alt="" />

alt="" />

Relocating to Canada from the U.S.? Before you pack your bags, take a hard look at your financial structure, especially if you’re married. One key area many couples overlook is how their income-producing assets are titled and taxed. Here’s why gifting and income-splitting strategies should be on your radar before making the move.

Canada Doesn’t Do “Married Filing Jointly”

Unlike the U.S., where couples can file a joint return and potentially benefit from a lower overall tax burden, Canada treats each spouse as a separate taxpayer. That means every adult in Canada files their own return, there are no joint returns allowed.

This might sound straightforward, but it can lead to a much higher combined household tax bill if income is unevenly distributed between spouses.

Why Income Splitting Matters

alt="" />

alt="" />

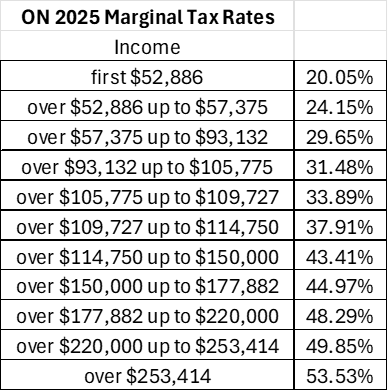

Let’s say one spouse earns significantly more than the other and holds most of the investments. In that case, the higher-income spouse is taxed at a steeper marginal rate, potentially over 50% depending on the province, while the other pays little to no tax.

For example, if Peter has $300,000 USD in earned income and holds all the investments in his name, the investment income will be taxed at 53.53%. If instead, Peter gifts the investment assets to his wife, Lois while they live in the U.S. and before they become Canadian tax residents, then none of the investment income would be taxed at the top combined marginal tax bracket when they move to Canada.

The solution is to equalize the taxable income between spouses wherever possible. That means shifting ownership of investment accounts, rental properties, and other taxable assets into the hands of the lower-income spouse. When income is distributed more evenly, both spouses can benefit from the lower tiers of Canada’s progressive tax system, reducing your overall household tax burden.

Gifting Assets: The Strategy Behind the Shift

Transferring ownership of assets is a powerful tool, but it must be done carefully and strategically, especially before you become a Canadian tax resident.

Here are a few important considerations:

1. Coordinate With Estate Planning

Changing ownership of assets can affect your estate plan. Who owns what matters not only for tax purposes, but also for inheritance planning. If you’re restructuring accounts, real estate, or business ownership, you may need to update your will, trust documents, or beneficiary designations.

In some cases, a postnuptial agreement may be required to formally acknowledge new ownership arrangements between spouses, particularly if the transferred assets are significant.

2. Be Careful If Your Spouse Is Not a U.S. Citizen

If your spouse is not a U.S. citizen, gifting can trigger U.S. gift tax rules. While U.S. citizens can gift an unlimited amount to a U.S. citizen spouse, there are annual limits on tax-free gifts to non-citizen spouses. The 2025 limit is $190,000 USD and is indexed. Exceeding the annual limit could result in reporting requirements and a potential gift tax.

alt="" />

alt="" />3. Plan for Capital Gains

Before you transfer any taxable assets, be aware that you may have to sell investments and create a taxable event, potentially triggering capital gains tax. This will create tax drag, which is when you have less assets invested than you would have if you had not sold, so the difference in projected tax rate between spouses needs to be large enough to justify the tax drag.

Additionally, if you’re planning to do Roth conversions or take distributions from Canadian Registered accounts, it’s wise to coordinate the timing and tax impact with any gifting strategies. The goal is to minimize your total tax burden across both countries while you have the chance before your tax residency shifts to Canada.

Income splitting and gifting before your move to Canada can be a smart financial strategy, but it’s not a DIY project. It requires coordination between:

- Tax planning

- Estate planning

- Cross-border financial planning

- Legal considerations

That’s where we come in.

At 49th Parallel Wealth Management, we help individuals and couples navigate the complex tax, estate, and financial planning decisions that come with moving between the U.S. and Canada. Our strategies are personalized, proactive, and designed to reduce long-term tax exposure on both sides of the border.

Moving to Canada? Let’s Get Your Financial House in Order.

You don’t have to figure it out alone. From Roth conversions and real estate to taxable accounts and trusts, we help ensure your move is smooth, strategic, and free of surprises. From the desert to the tundra, we are your cross-border retirement experts!