US vs Canada Citizenship Law: The Exclusive Citizenship Act vs Bill C-3

By :Lucas Wennersten, CFP® (US & Canada), CFA · 8 minute read · Refreshed May 13, 2026

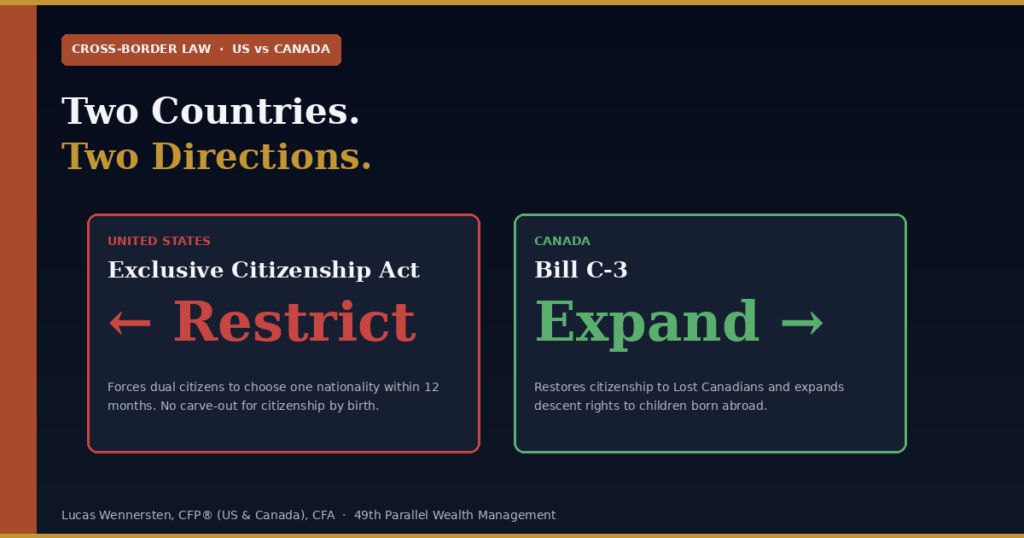

Two countries that share the world’s longest undefended border are moving in opposite directions on the question of citizenship. The United States has introduced the Exclusive Citizenship Act of 2025, which would force American dual citizens to choose one nationality. Canada has introduced Bill C-3, which expands citizenship rights and restores citizenship to people who lost it under earlier rules.

For cross-border families — and there are millions of them between Canada and the US — these two laws would land at the same time and pull in opposite directions. This article walks through both, side by side, with a focus on what it actually means for families who live and work between the two countries.

For the tax mechanics behind the US Act — FEIE, FTC, FATCA, the exit tax, and why renunciation has expensive consequences — see the deep tax analysis of the Exclusive Citizenship Act.

The United States: The Exclusive Citizenship Act of 2025

The Exclusive Citizenship Act of 2025 is a proposed bill introduced in the US Senate that would eliminate dual citizenship for Americans. Under the Act as drafted, every US citizen who also holds another country’s citizenship would be required to choose one within twelve months of the bill becoming law. Anyone who failed to choose would automatically lose their US citizenship one year after enactment.

The Act applies regardless of how the second citizenship was acquired. A US citizen who became Canadian by marriage, a US citizen born in Canada, a US citizen who acquired Canadian citizenship through descent from a Canadian parent — all would be required to make the choice. There is no carve-out for accidental dual citizens, no grandfather provision for citizenship acquired at birth, and no protection for minors.

The mechanism is significant because of what already attaches to renunciation under existing US law. IRC §§877 and 877A govern the tax treatment of US citizens who renounce. A renouncing citizen who is a ‘covered expatriate’ — meaning their net worth exceeds $2 million, their average annual US tax exceeded approximately $206,000 over the prior five years, or they fail to certify five years of US tax compliance — faces a mark-to-market exit tax on worldwide assets.

Under the Exclusive Citizenship Act, anyone who chooses their foreign citizenship would trigger this regime simultaneously with millions of others. The administrative load alone would be staggering. The tax revenue impact, perhaps surprisingly, would likely be negative for the US Treasury — most US citizens abroad pay no US tax under existing exclusions and credits, but a large number of high-net-worth dual citizens forced to renounce would pull US-situs assets out of the system to avoid the post-renunciation estate tax exposure that drops from a $15 million citizen exemption to a $60,000 non-citizen exemption.

Canada: Bill C-3 Expands Citizenship Rights

Canada’s Bill C-3 moves in the opposite direction. The bill responds to a 2023 Ontario Superior Court decision that found the existing first-generation limit on citizenship by descent to be unconstitutional. Under prior law, a Canadian citizen who was born outside Canada could not automatically pass citizenship to a child born outside Canada — a rule that produced a class of people known as ‘Lost Canadians.’

Bill C-3 does three things. First, it removes the first-generation limit, allowing Canadian citizens born abroad to pass citizenship to their children regardless of where the children are born. Second, it restores citizenship to people who lost it under prior rules. Third, it sets a ‘substantial connection’ test for citizenship by descent beyond the first generation, requiring that the Canadian-citizen parent demonstrate at least 1,095 days (three years) of physical presence in Canada before the child’s birth.

The contrast with the US Act is stark. Where the Exclusive Citizenship Act would strip citizenship from people based on a procedural failure to choose, Bill C-3 restores citizenship to people who never should have lost it. Where the US Act forces a permanent decision on minors who cannot meaningfully consent, Bill C-3 preserves citizenship pathways for Canadian children born globally. Where the US Act centralizes sovereignty as exclusivity, Bill C-3 treats global mobility as a normal feature of modern citizenship rather than a problem to be solved.

Side-by-Side: Exclusive Citizenship Act vs Bill C-3

Issue | United States — Exclusive Citizenship Act | Canada — Bill C-3 |

Direction | Restricts citizenship — forces choice between US and any other | Expands citizenship — restores it and broadens descent rights |

Effect on dual citizens | Forces them to renounce one citizenship within 12 months | Allows them to keep both; restores citizenship to those wrongly stripped |

Effect on children | Children with dual citizenship at birth must choose at majority — no grandfather | Children born abroad to Canadian citizens can inherit citizenship under expanded rules |

Tax consequences for non-compliance | Automatic loss of US citizenship → exit tax under IRC §877A if ‘covered expatriate’ | No tax consequence — citizenship is a status, not a tax trigger |

Treatment of accidental dual citizens | No carve-out — applies regardless of how the second citizenship was acquired | Substantial connection test (1,095 days physical presence) for descent beyond first generation |

Cross-border family impact | Forces choice that can split families across the border permanently | Preserves family citizenship continuity across borders |

Underlying philosophy | Citizenship is exclusive — incompatible with allegiance elsewhere | Citizenship is inclusive — recognizes modern global mobility |

Status | Proposed legislation, not enacted as of May 2026 | Tabled in Parliament, moving through committee as of May 2026 |

What This Means for Cross-Border Families

Cross-border families don’t experience these laws in isolation. They face both regimes simultaneously, and the practical implications cascade through everyday life — where children attend school, where retirement accounts are held, where property is owned. Three scenarios illustrate how the combined effect lands.

Scenario 1:

A US-citizen family in Arizona has a child born in Toronto during a work assignment. The child is a US citizen by birth to US parents and a Canadian citizen by birth in Canada. Under existing law, both citizenships are stable. Under the Exclusive Citizenship Act, the child would be required to choose at the age of majority. Under Bill C-3, the child could later pass Canadian citizenship to their own children born abroad, provided the 1,095-day substantial connection test is met. The net effect: a child who could grow up with two clear pathways is forced into a single one — by the US — while Canada extends the second pathway across generations.

This scenario isn’t hypothetical for me. My son was born in Toronto in 2019; we live in Arizona. Under current law, his dual citizenship is settled. Under the proposed Act, he would face a choice he’s far too young to understand — and one that, given our domicile, would functionally strip him of the Canadian citizenship he holds by birthright.

Scenario 2:

A Canadian-born US permanent resident, now a US citizen, owns a Canadian cottage. She retains Canadian citizenship through birth. Under the Exclusive Citizenship Act, she would have to choose. If she renounces US citizenship, she becomes a non-resident alien for US tax purposes — and any US-situs property she owns, including any US securities held outside retirement accounts, loses the $15 million US estate tax exemption and gets only the $60,000 non-citizen exemption. The cottage in Canada is fine. The US assets become a tax problem. If she renounces Canadian citizenship to stay American, she may face Canadian departure tax rules if she ever becomes a Canadian tax resident again, and the cottage continues to face cross-border treatment under Canadian rules.

Scenario 3:

A Lost Canadian — someone who lost Canadian citizenship under earlier rules — would have it restored under Bill C-3. But if that same person is also a US citizen, the Exclusive Citizenship Act would simultaneously require them to choose. The two laws would arrive at their doorstep in the same year — one offering back a citizenship that was wrongly taken, the other demanding they give up the citizenship they already have. The cross-pressure is the cruelest illustration of how poorly aligned the two systems would be.

What Cross-Border Families Can Do Right Now

Neither bill is law yet. The Exclusive Citizenship Act faces significant constitutional questions — the Fourteenth Amendment protects citizenship from being stripped without due process — and Bill C-3 is moving through committee in the Canadian Parliament. But cross-border families should not wait to understand their exposure. Three practical steps are worth considering now:

- Document everything. Pull together birth records, naturalization records, prior Canadian citizenship documentation, and US passport history. If Bill C-3 passes, restoring Canadian citizenship requires documentation. If the Exclusive Citizenship Act passes, contesting an automatic loss of US citizenship will require the same.

- Model the tax cost of renunciation now, before the rush. If renunciation becomes mandatory under the US Act, millions of high-net-worth dual citizens will all need expatriation tax modeling at the same time. Anyone in this category benefits from doing the analysis early.

- Review the structure of US-situs assets. If the Exclusive Citizenship Act passes and you renounce US citizenship, the $60,000 non-citizen estate tax exemption on US-situs assets becomes the new ceiling. Real estate, brokerage accounts outside retirement plans, and direct holdings of US stocks all become more expensive to hold post-renunciation.

The Bottom Line

Two countries on the same border are moving in opposite directions on citizenship at the same time. The United States is moving toward exclusivity. Canada is moving toward inclusion. For families who live between the two countries, the practical consequences are very different — Canada’s approach preserves family continuity across generations and borders, while the US approach forces choices that have multi-generational tax and estate planning consequences.

The Exclusive Citizenship Act is not yet law and faces serious constitutional headwinds. Bill C-3 is more procedurally straightforward — Canada’s Supreme Court has effectively required the changes Bill C-3 implements. Cross-border families who track both bills now will be far better positioned to act when either, or both, reach final passage.

Frequently Asked Questions

Q: What is the Exclusive Citizenship Act of 2025?

A: The Exclusive Citizenship Act of 2025 is a proposed US Senate bill that would require American dual citizens to choose between US citizenship and any other citizenship they hold within twelve months of the bill becoming law. Anyone who failed to choose would automatically lose their US citizenship one year after enactment.

Q: What is Bill C-3 in Canada?

A: Bill C-3 is Canadian legislation responding to a 2023 court ruling that found Canada’s first-generation limit on citizenship by descent unconstitutional. Bill C-3 removes that limit, restores citizenship to people who lost it under earlier rules (Lost Canadians), and sets a 1,095-day substantial connection test for descent beyond the first generation.

Q: Does the Exclusive Citizenship Act apply to children?

A: As drafted, yes. The Act does not contain carve-outs for minors or for citizenship acquired at birth. A child born to one US parent and one Canadian parent — and therefore a citizen of both countries at birth — would be required to choose one citizenship at the age of majority.

Q: If the US Act passes, can I keep my US citizenship by renouncing my Canadian citizenship?

A: Under the Act as drafted, yes. The choice goes either direction. The US Act would require you to renounce all foreign citizenships within twelve months. The practical consequences of either choice — keeping US and losing Canadian, or losing US and keeping Canadian — depend on where you live, where your assets are held, and your family circumstances.

Q: What is a Lost Canadian?

A: A Lost Canadian is a person who lost or was denied Canadian citizenship under prior legislation, particularly the first-generation limit on citizenship by descent. Bill C-3 is designed to restore citizenship to this group. Estimates of the affected population range from tens of thousands to over a hundred thousand people.

Q: How does this affect my cross-border financial planning?

A: If the US Exclusive Citizenship Act passes, anyone forced to renounce US citizenship faces a chain of cross-border financial consequences: the US exit tax under IRC §877A if they are a covered expatriate, a drop from the $15 million US estate tax exemption to a $60,000 non-citizen exemption on US-situs assets, and special tax treatment of any future gifts or bequests to US persons.

Q: Will the Exclusive Citizenship Act survive a constitutional challenge?

A: Many constitutional scholars are skeptical. The Fourteenth Amendment to the US Constitution provides that all persons born or naturalized in the United States are citizens. Supreme Court precedent, particularly Afroyim v. Rusk (1967), establishes that US citizenship cannot be stripped without the citizen’s consent. The Act would face immediate court challenges and may not survive them.

Q: Will Bill C-3 pass?

A: Bill C-3 has stronger procedural momentum than the US Act because the underlying court ruling that found the prior law unconstitutional has set a deadline for Parliament to act. Whether the final version retains every provision of the current draft is uncertain, but the broad direction of restoring lost citizenship and removing the first-generation limit is widely expected to become law.

Q: If my child has both US and Canadian citizenship, do I need to do anything now?

A: Not under current law. Both citizenships are stable as long as both countries continue to recognize dual citizenship. But families in this position should keep complete documentation of how each citizenship was acquired — birth certificates, US passports, Canadian citizenship documentation — so they can respond quickly if either law passes.

Q: Where can I get advice that covers both the US and Canadian sides of this?

A: Cross-border family planning requires advice that genuinely spans both regulatory systems, not just expertise on one side. For a complimentary consultation with a CFP® licensed in both the US and Canada, see the contact link below.

Get Cross-Border Family Planning Clarity

Cross-border families face complexity that single-jurisdiction advisors cannot fully address. If you hold US and Canadian citizenship in your family — yourself, your spouse, or your children — book a complimentary consultation with 49th Parallel Wealth Management. Lucas Wennersten is dual-licensed CFP® (US & Canada) and a CFA, and our practice is built specifically around the families who span both countries.

This article is for general educational purposes and is not legal, tax, or immigration advice. The Exclusive Citizenship Act of 2025 and Canada’s Bill C-3 are both proposed legislation that has not been enacted as of the publication date. Specific provisions and effective dates may change as each bill moves through legislative process. Consult a qualified cross-border advisor before taking action.

LW

Lucas Wennersten

Cross-Border Financial Advisor · 49th Parallel Wealth Management

CFA

CFP® US & Canada

Founder

Author

Columnist

Lucas Wennersten is the founder of 49th Parallel Wealth Management and a dual-certified financial planner (CFP® US & Canada) and Chartered Financial Analyst (CFA). With a career spanning both Arizona and Toronto, Lucas brings firsthand experience navigating cross-border finances to every client relationship. He writes and speaks on wealth management, cross-border tax strategy, and retirement planning for Canadians and Americans living between two countries.

📚

Book by Lucas Wennersten

Crossing the 49th Parallel: A Retirement Planning Guide for Moving Across the Canada–U.S. Border

crossingthe49thparallel.com

49th Parallel Wealth Management

From the Desert to the Tundra™

0 thoughts on “The Exclusive Citizenship Act of 2025 vs Bill C-3”

Pingback: The Beauty of Diversity: Choosing Love, Curiosity, and Patience in a Divided World - Crossing the 49th Parallel