class="attachment-full size-full wp-image-9267" alt="U.S Exit Tax Renunciation" srcset="https://49thparallelwealthmanagement.com/wp-content/uploads/2026/06/us-exit-tax-renunciation-linkedin-1.png 1200w, https://49thparallelwealthmanagement.com/wp-content/uploads/2026/06/us-exit-tax-renunciation-linkedin-1-300x300.png 300w, https://49thparallelwealthmanagement.com/wp-content/uploads/2026/06/us-exit-tax-renunciation-linkedin-1-1024x1024.png 1024w, https://49thparallelwealthmanagement.com/wp-content/uploads/2026/06/us-exit-tax-renunciation-linkedin-1-150x150.png 150w, https://49thparallelwealthmanagement.com/wp-content/uploads/2026/06/us-exit-tax-renunciation-linkedin-1-768x768.png 768w, https://49thparallelwealthmanagement.com/wp-content/uploads/2026/06/us-exit-tax-renunciation-linkedin-1-600x600.png 600w, https://49thparallelwealthmanagement.com/wp-content/uploads/2026/06/us-exit-tax-renunciation-linkedin-1-100x100.png 100w" sizes="(max-width: 1200px) 100vw, 1200px" />

class="attachment-full size-full wp-image-9267" alt="U.S Exit Tax Renunciation" srcset="https://49thparallelwealthmanagement.com/wp-content/uploads/2026/06/us-exit-tax-renunciation-linkedin-1.png 1200w, https://49thparallelwealthmanagement.com/wp-content/uploads/2026/06/us-exit-tax-renunciation-linkedin-1-300x300.png 300w, https://49thparallelwealthmanagement.com/wp-content/uploads/2026/06/us-exit-tax-renunciation-linkedin-1-1024x1024.png 1024w, https://49thparallelwealthmanagement.com/wp-content/uploads/2026/06/us-exit-tax-renunciation-linkedin-1-150x150.png 150w, https://49thparallelwealthmanagement.com/wp-content/uploads/2026/06/us-exit-tax-renunciation-linkedin-1-768x768.png 768w, https://49thparallelwealthmanagement.com/wp-content/uploads/2026/06/us-exit-tax-renunciation-linkedin-1-600x600.png 600w, https://49thparallelwealthmanagement.com/wp-content/uploads/2026/06/us-exit-tax-renunciation-linkedin-1-100x100.png 100w" sizes="(max-width: 1200px) 100vw, 1200px" />The Seven Figures, Two Countries Series — Post 3 of 4

The US Exit Tax When You Renounce: The Real Math at $5M+

By Lucas Wennersten, CFP® (US & Canada), CFA · 9-minute read

Part of Seven Figures, Two Countries — cross-border wealth decisions for $5M+ Canada-US families.

Home › Blog › Seven Figures, Two Countries › The US Exit Tax When You Renounce

This article is general education, not personalized tax, legal, or financial advice. Exit-tax rules are intricate, fact-specific, and change with annual inflation adjustments. Before acting on renunciation, speak with a cross-border advisor and a US tax attorney.

Most people who reach the point of seriously considering renunciation of US citizenship have already worked through the personal questions — family, identity, future plans. What surprises them is the tax math. The US exit tax under Section 877A is widely misunderstood, occasionally exaggerated, and almost always larger and stranger than the back-of-envelope number people arrive with. For families at $5 million and above, it is rarely a footnote in the decision — it often is the decision. This piece is the cost-side companion to the broader cross-border tax planning conversation: the actual math, the levers that move it, and the moves worth making before the date you give up your passport.

This is the tax-math piece. For the background on who counts as a covered expatriate and the procedural side, see our companion article on covered expatriate status. Here, we focus on what it actually costs.

First, the gateway: three tests, anyone triggers it

Renouncing US citizenship does not, by itself, trigger the exit tax. It is triggered only if you are a “covered expatriate” — the technical category the rules apply to. You become one if you meet any of three tests on your expatriation date:

- Net worth of $2,000,000 or more on the date of expatriation. This figure is statutory and not adjusted for inflation. At $5M+, you trip this one automatically.

- Average annual US net income tax of $211,000 or more for the five tax years before expatriation (2026 figure; this threshold is inflation-adjusted each year).

- Failure to certify five years of tax compliance on IRS Form 8854. Even if you pass the first two tests, getting this wrong makes you a covered expatriate by default.

There is a narrow exception for certain dual citizens from birth who have remained tax-resident in the other country, and for some who expatriate before reaching age 18½. These exceptions are highly fact-specific. For most $5M+ Americans considering renunciation, they do not apply.

How the exit tax actually works: the mark-to-market regime

The mechanism is the part that catches people off guard. On the day before you expatriate, the IRS treats you as having sold all your worldwide property at fair market value — a deemed sale of everything you own, all at once. You then pay capital gains tax on the net gain above an exclusion. The IRS lays this out on its Expatriation Tax page.

For 2026, that exclusion is $910,000 (up from $890,000 in 2025; it is indexed for inflation each year). It applies to your total net gain across all mark-to-market assets, not to each asset individually. Losses offset gains in the calculation. Whatever net gain remains above $910,000 is taxed at long-term capital gains rates — typically 20% federal plus the 3.8% net investment income tax for high-income filers, totalling 23.8%, before any state tax.

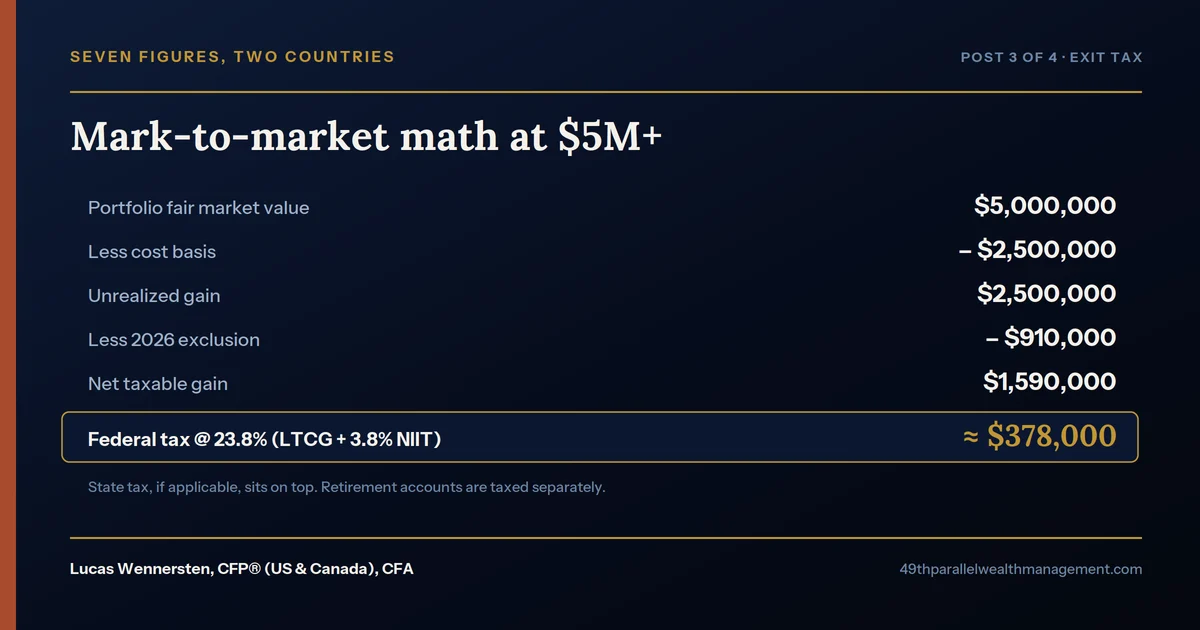

The math at $5M+: a worked example

Numbers make this concrete. Imagine a US citizen with a $5,000,000 portfolio, mostly equity built up over a long career, with an aggregate cost basis of $2,500,000. The unrealized gain is $2,500,000. The exit tax on those assets, on the day before renunciation, runs roughly as follows:

Portfolio fair market value: $5,000,000. Cost basis: $2,500,000. Unrealized gain: $2,500,000. Less the 2026 exclusion of $910,000. Net taxable gain: $1,590,000. Federal tax at 23.8% (long-term capital gains plus net investment income tax): roughly $378,000. State tax, if applicable, sits on top.

That is the number most people are not expecting — and it is just the mark-to-market portion. Retirement accounts and deferred compensation are taxed separately and, often, less forgivingly.

Retirement accounts and deferred compensation are treated differently

This is where the cost can balloon. “Specified tax-deferred accounts” — IRAs, Roth IRAs, 401(k)s (when held outside an employer’s eligible plan), HSAs, 529 plans, Coverdell ESAs — are not part of the mark-to-market regime. Instead, you are treated as having received the entire account balance as a distribution on the day before expatriation. The full balance is taxed as ordinary income that year, with no $910,000 exclusion against it.

For a $5M+ family, that can mean a seven-figure IRA pushed into the top ordinary-income bracket in a single year, on top of the mark-to-market tax on the rest of the portfolio. It is one of the largest, least-flexible parts of the entire exit-tax exposure.

Eligible deferred compensation (for example, a qualifying employer pension or 401(k) the plan agrees to handle correctly) is treated differently again: you generally are not taxed at exit, but a 30% withholding tax applies to each future payment, and you waive the protections of any tax treaty on those payments. Ineligible deferred compensation — including many foreign pensions and unvested or unexercised stock awards — is taxed at exit on the present value of what you are entitled to receive. Nongrantor trust interests follow their own rules and are some of the most complex pieces of the regime.

Section 2801: the tax that follows your family

This is the part people learn about late. After you renounce as a covered expatriate, gifts and bequests you later make to US persons (US citizens and residents) trigger a 40% tax — paid by the recipient — under Section 2801. This is a separate regime from the exit tax and continues for the rest of your life. There is no time limit.

Practically, this means that if your post-renunciation plan includes leaving a meaningful inheritance to US children or grandchildren, the cost of getting wealth across that gap is real, recurring, and built into the rest of the decision. It is the single most common reason a renunciation analysis comes out negative for a family with US-resident heirs.

The treaty does not save you

Some clients assume the Canada-United States Tax Convention must provide relief from the exit tax — it does not. The treaty’s saving clause preserves each country’s right to tax its own citizens (and former citizens, in the case of the exit-tax regime) under its own rules. Canada’s foreign tax credit system may eventually relieve double taxation when you later sell the same asset and Canada taxes the post-immigration gain, but it does not reach back to undo the exit tax itself.

Levers worth pulling before the renunciation date

Almost every meaningful reduction in exit-tax exposure is structural and time-sensitive. By the date of expatriation it is generally too late to move the numbers. The most useful planning moves before that date include:

Time the renunciation deliberately. Avoid renouncing in a year of unusually high income or large realized gains; the exit tax sits on top of everything else. Realize losses pre-exit where possible to offset the deemed gain.

Use the appreciated-securities lever. Donating appreciated securities pre-renunciation removes high-gain positions from the mark-to-market base and delivers a charitable deduction in the same year — frequently the single most efficient pre-exit move.

Coordinate with a concentrated stock position plan. If you are also moving to Canada, the Canadian arrival cost-base reset and the US exit-tax math interact, and the order of events matters: residency change, then renunciation, then sales is a very different sequence from the reverse.

Consider the deferral election. For mark-to-market gains, an election allows you to defer the exit-tax payment on specific assets until they are actually sold, with adequate security (typically a bond or letter of credit) and a waiver of treaty benefits on those assets. It can ease cash-flow pain on illiquid holdings but does not reduce the ultimate tax.

Plan your cross-border wealth management around the whole picture. The Section 2801 issue, especially, often only resolves through how the post-renunciation estate plan is structured — with the heirs’ tax residence as one of the central variables.

A pre-renunciation checklist

Before you set an expatriation date, work through:

- Confirm whether you are likely to be a covered expatriate (most $5M+ households are, by net worth alone).

- Inventory worldwide assets at current fair market value — the exit tax is calculated on that figure.

- Identify retirement accounts and deferred compensation separately; they are not part of the mark-to-market exclusion.

- Model the math in a year of low ordinary income to avoid stacking effects.

- Realize losses pre-exit where possible; consider charitable gifts of high-gain positions.

- Decide whether to make the deferral election for illiquid mark-to-market assets.

- Address the Section 2801 path — especially if you have US-resident children or grandchildren.

- Coordinate the exit date with any move to a new country of residence; sequence matters.

The bottom line

Renouncing US citizenship at $5M+ is the rare planning decision where the cost can be calculated with reasonable precision — and where the calculation often shifts the decision. The exit tax itself is large; the retirement-account piece is larger and less flexible than people expect; and the Section 2801 regime, paid by your US heirs after you renounce, is the long tail almost everyone underestimates. None of it is unmanageable with lead time. All of it is hard to fix in the last quarter before your expatriation date.

Frequently asked questions

What is the US exit tax?

It is the tax imposed under Section 877A on a covered expatriate’s worldwide assets, treated as sold at fair market value the day before expatriation. It captures unrealized gains the US would otherwise lose the right to tax once you are no longer a citizen or long-term resident.

Who is a covered expatriate?

Anyone who renounces US citizenship (or terminates long-term residency) and meets any one of three tests on the expatriation date: net worth of $2 million or more, an average annual US income tax of $211,000 or more for the prior five years (2026 figure), or failure to certify five years of tax compliance on Form 8854.

How is the exit tax calculated?

The IRS treats you as having sold all your worldwide property at fair market value on the day before expatriation. Net gain across all mark-to-market assets, less the annual exclusion, is taxed at long-term capital gains rates, plus the 3.8% net investment income tax for high-income filers. Retirement accounts and deferred compensation follow separate rules.

What is the 2026 exit-tax exclusion amount?

$910,000, up from $890,000 in 2025. The exclusion is inflation-adjusted annually by the IRS in its revenue procedure. The $2 million net-worth threshold for covered expatriate status, by contrast, is statutory and not indexed.

How are my IRA and 401(k) treated under the exit tax?

IRAs, Roth IRAs, HSAs, 529 plans, and similar specified tax-deferred accounts are treated as fully distributed to you on the day before expatriation, taxed as ordinary income in that year, with no $910,000 exclusion against them. Eligible employer deferred compensation has its own 30% withholding regime on future payments.

What is the actual exit-tax cost on a $5 million portfolio?

It depends on cost basis, but a $5M portfolio with a $2.5M basis (a $2.5M unrealized gain) yields roughly $378,000 in federal tax (long-term capital gains plus the net investment income tax) after the 2026 exclusion. State tax and retirement-account treatment can add significantly more.

Does the Canada-US tax treaty reduce or eliminate the exit tax?

No. The treaty’s saving clause preserves the US right to tax its citizens and former citizens under the exit-tax regime. Foreign tax credit relief may help with later double taxation when Canada eventually taxes the same asset’s post-immigration gain, but does not reduce the exit tax itself.

Can I defer paying the exit tax?

Yes, an election allows deferral of the mark-to-market tax on specific assets until they are actually sold, provided you post adequate security and waive treaty benefits on those assets. It is a cash-flow tool, not a tax-reduction tool.

What is Section 2801, and does it affect my heirs?

Section 2801 imposes a separate 40% tax on gifts and bequests from covered expatriates to US persons, paid by the US recipient. It applies indefinitely after expatriation and is often the largest long-term cost for families with US-resident heirs.

More from Seven Figures, Two Countries

Cross-Border Charitable Giving: A Guide for Wealthy Canada-US Families — Article XXI, in-kind gifts, and the cross-border philanthropy levers that work in both countries.

Concentrated Stock When You Move to Canada: The $5M Diversification Problem — The ITA 128.1 cost-base reset and the US-Canada basis mismatch.

T1135 Foreign Reporting: The Form That Can Cost More Than the Tax — The CRA’s foreign-property inventory that calculates no tax but punishes silence.