Seven Figures, Two Countries: A Cross-Border Wealth Series for $5M+ Canada-US Families

By Lucas Wennersten, CFP® (US & Canada), CFA · 7-minute read

Series introduction — read first, then dive into the four pieces.

Home › Blog › Seven Figures, Two Countries

This series is general education, not personalized tax, legal, or financial advice. Each piece is illustrative; cross-border rules are intricate, fact-specific, and change over time. Before acting, speak with a cross-border advisor about your situation.

When a wealthy family’s life spans both sides of the 49th parallel, the planning gets harder rather than easier — not because either system is necessarily worse, but because each country’s rules were designed without the other in mind. A decision that is beautifully tax-efficient on one side can be silently expensive on the other. Sequencing matters. Timing matters. Sometimes citizenship matters more than residency. And the planning conversation that works for a domestic-only household quietly breaks once the border is in the picture, which is why integrated cross-border wealth management looks different from the sum of its parts.

Seven Figures, Two Countries is a series for $5M+ households navigating that complexity. Each piece takes a single cross-border decision that genuinely bites at this level of wealth and works through what actually happens — the planning levers, the trap that catches almost everyone, and the math in real numbers. These are not introductory articles. They assume you are past “what is a TFSA” and facing real-money decisions: a move, a sale, a gift, a renunciation, an annual reporting obligation that quietly compounds.

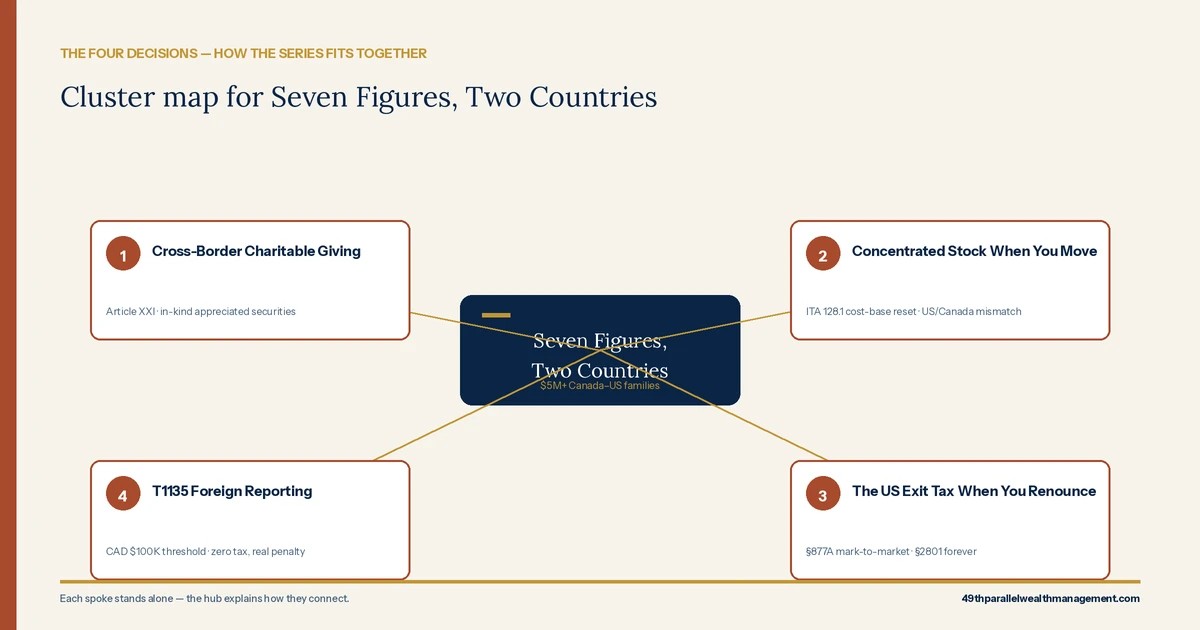

The four decisions

The series covers four areas where the cross-border interaction is most consequential at the seven-figure level. Each is genuinely under-served in the cross-border literature, each is high-stakes, and each connects to the others in ways that matter once you see them together.

1. Cross-Border Charitable Giving

By default, each country only rewards gifts to its own charities. The Canada-United States Tax Convention provides a limited bridge under Article XXI — but with a string attached that surprises almost every donor: the gift must align with income sourced in the charity’s country. And the single biggest lever almost no one uses correctly is donating appreciated securities in-kind instead of cash, which can eliminate the Canadian capital gain entirely while delivering a full-value receipt. For families giving meaningfully, structure (donor-advised funds vs private foundations, holding-company gifts) becomes the real conversation.

Read the full guide: Cross-Border Charitable Giving: A Guide for Wealthy Canada-US Families

2. Concentrated Stock and the Move to Canada

A founder, long-tenured executive, or tech employee with $5M+ in a single stock faces an investment problem disguised as a tax problem. Becoming a Canadian resident delivers a powerful gift — a fresh cost base on arrival, deemed acquired at fair market value, so Canada does not tax the pre-immigration gain. CRA’s guidance for newcomers to Canada explains the rule, but for US citizens, the IRS does not reset basis at all. The resulting mismatch — sometimes millions of dollars wide — is the heart of the planning. So is the diversification toolkit (sell-down with loss harvesting, donations, exchange funds, collars), each of which travels across the border differently and rarely the way generic US advice suggests.

Read the full guide: Concentrated Stock When You Move to Canada: The $5M Diversification Problem

3. The US Exit Tax When You Renounce

By the time most people seriously consider renunciation, the personal questions are settled — what catches them off guard is the math. The IRS expatriation tax regime, under Section 877A, is widely misunderstood and almost always larger and stranger than the back-of-envelope estimate. At $5M+, the gateway is automatic via the $2 million net-worth test. The mark-to-market regime taxes worldwide assets as if sold the day before expatriation; retirement accounts are treated worse than people expect; and Section 2801’s 40% transfer tax follows the renouncer indefinitely — paid by US-resident heirs on every later gift and bequest. The procedural side runs through the US Department of State, but the cost side is where the decision often shifts.

Read the full guide: The US Exit Tax When You Renounce: The Real Math at $5M+

4. T1135 Foreign Reporting

The form that calculates no tax but punishes silence. Form T1135 — the CRA’s annual inventory of your foreign property — is triggered automatically once total cost of specified foreign property crosses CAD $100,000, a threshold that has not moved in two decades. At $5M+, you are permanently in the detailed-reporting tier. Penalties start at $25 per day, escalate to $12,000 or more for gross negligence, and can extend the period during which the CRA reopens your return. It is also a separate regime from the US side, where US citizens living in Canada may also have to file the FBAR (FinCEN Form 114) and Form 8938 — the cross-border family files all of them, with different definitions on each side of the border.

Read the full guide: T1135 Foreign Reporting: The Form That Can Cost More Than the Tax

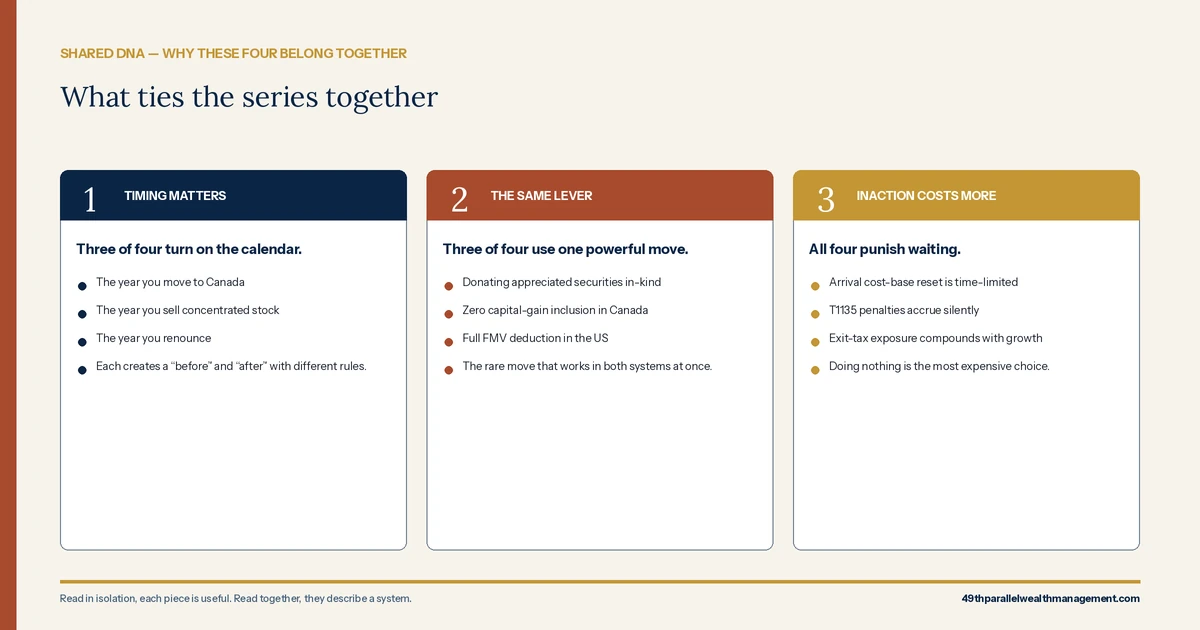

How these four decisions connect

These are not four standalone topics — they share the same DNA, which is what makes them a series rather than a list.

Three of the four turn on timing. The year you move to Canada, the year you sell concentrated stock, the year you renounce — each creates a “before” and “after” with different rules, and the sequence in which you cross those events can change the answer by seven figures. T1135 is the inventory layer the other three operate against: what you hold, where, and what its cost base is.

Three of the four involve the same lever — donating appreciated securities. Whether you are giving philanthropically, diversifying a concentrated position, or trimming a portfolio before renunciation, the in-kind charitable gift is the rare move that helps in both countries simultaneously. It is the one strategy that recurs across the series for good reason.

All four are areas where doing nothing is the most expensive choice. The Canadian arrival cost-base reset is time-limited. T1135 penalties accrue silently. Exit-tax exposure compounds with portfolio growth. Charitable giving without planning leaves five and six figures on the table. None of these decisions reward waiting.

Read in isolation, each piece is useful. Read together, they describe an integrated approach to high-net-worth cross-border planning that takes the calendar as seriously as the strategy.

How to use this series

Each guide stands alone, so start with the one closest to your situation. If you are contemplating a move, begin with concentrated stock. If philanthropy is part of your plan, start with the giving guide. If renunciation is on the table, the exit-tax piece is the math you need before going further. T1135 applies to anyone in Canadian residency with foreign assets — which, in this series’ audience, is essentially everyone.

If you want a second opinion specific to your situation, book a complimentary consultation with our team. We work with families in exactly this seam, and the planning value is usually in the interaction between these decisions, not in any one of them alone.

A note on what this series is — and isn’t

This is general education, not advice. The math examples are illustrative. The thresholds in tax law change with annual inflation adjustments. The cross-border interaction depends heavily on specific facts — your citizenship, your residency dates, the nature of your holdings, the order of your moves. What this series can do is help you ask sharper questions and recognize where the cross-border dimension changes the answer you would otherwise be given by a domestic-only advisor.

Frequently asked questions

Who is Seven Figures, Two Countries written for?

Wealthy Canada-US families navigating the cross-border dimension of their wealth: dual residents, snowbirds with substantial holdings, US persons living in Canada, Canadians with significant US assets, and anyone considering moving across the 49th parallel with seven-figure investable wealth.

Why these four topics specifically?

Because each is genuinely under-served in cross-border content, each becomes material at $5M+, and they connect to one another in ways that change the answer. Each was selected by mining what competitors rank for, what the planning literature ignores, and where we see clients arrive with the most expensive misunderstandings.

What counts as $5M+ in this context?

Total household financial wealth — investable assets plus business interests — of roughly $5 million and above. The exact figure matters less than the planning posture: at this level, the cross-border friction points described in the series stop being theoretical and start being seven-figure decisions.

Do I need to read the series in order?

No. Each guide stands alone. The hub explains how they connect; the spokes go deep on individual decisions. Most readers arrive at one piece via their specific situation and pull in the others as the connections become relevant.

Is this series US tax advice or Canadian tax advice?

Both — every piece treats the two systems together, because separating them is the most common mistake at this level of wealth. The series is written for cross-border families, not for tax filers in either single jurisdiction.

Does this series replace working with a cross-border advisor?

No, and it is not designed to. Cross-border planning depends heavily on specific facts: citizenship, residency dates, asset locations, family situations. The series is designed to help you ask sharper questions, recognize where the border changes the answer, and arrive at the planning conversation already knowing what to look for.

Will additional pieces be added to the series?

Yes, when a new $5M+ cross-border decision shows up as both meaningfully under-served and consequential. The four current pieces were chosen because each met that bar; future additions will follow the same rule.

What is the single biggest cross-border planning mistake the series addresses?

Treating each country’s rules in isolation. Most of the expensive mistakes we see at $5M+ come from advice that is correct domestically and disastrous internationally — a US strategy applied to a Canadian resident, or vice versa, with no one watching the interaction between them.

How are these four topics connected to each other?

Three of them turn on timing — the year you move, the year you sell, the year you renounce — and the fourth (T1135) is the inventory layer those decisions operate against. Three of them share a single planning lever (donating appreciated securities). And all four punish inaction harder than they punish bad action, which is why they belong together.

Navigating a cross-border decision that touches more than one of these areas? Book a complimentary consultation with our team and we will model the interaction — not just the individual pieces.