Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

The Anti-CBDC Act: What a U.S. Digital Dollar Ban Means for Cross-Border Investors

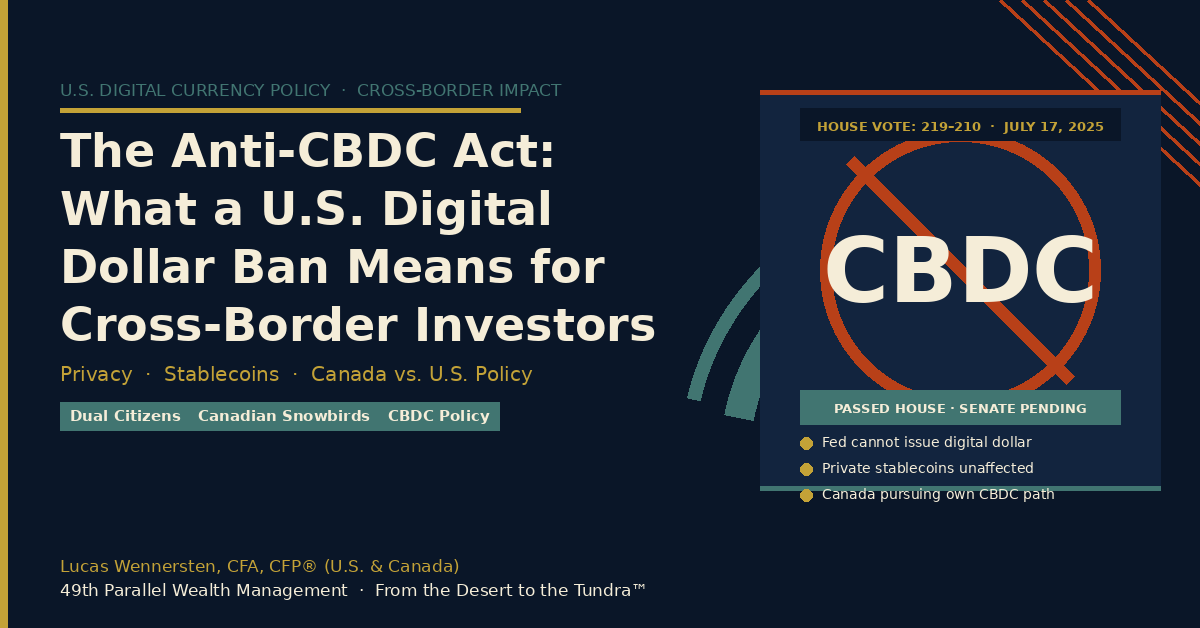

In July 2025, the U.S. House of Representatives passed the Anti-CBDC Surveillance State Act — a bill that would permanently prohibit the Federal Reserve from issuing a central bank digital currency, either directly to consumers or through financial intermediaries. The bill now awaits Senate action, but its passage marks a decisive political statement about the direction of U.S. digital finance.

For most Americans, this is a debate about privacy and government overreach. For Canadians with U.S. accounts, dual citizens managing digital assets in both countries, and cross-border families navigating two different financial systems, the implications run deeper. While the U.S. moves to block a federal digital dollar, Canada is pursuing its own CBDC research independently — creating a growing divergence in digital currency policy that cross-border investors need to understand.

At 49th Parallel Wealth Management, we work with clients on both sides of the border who are asking what this means for their financial plans. Here is what we know and what to watch.

Anti-CBDC Surveillance State Act

The Anti CBDC Surveillance State Act (H.R. 1919), introduced on March 6, 2025 by Rep. Tom Emmer (R MN), prohibits the Federal Reserve from issuing a central bank digital currency (CBDC), either directly or through intermediaries. It also bars the Fed from using any CBDC for monetary policy, and from conducting related tests or pilots, unless Congress explicitly authorizes it.

Where It Stands in the Legislative Process

• Introduced: March 6, 2025, and reported (amended) by the Financial Services Committee on May 6.

• Passed the House: July 17, 2025, by a vote of 219–210.

• Next Step: Awaiting action in the Senate before heading to the President for signature.

The Act was strategically attached to the must-pass National Defense Authorization Act to ensure momentum.

Cross-Border Context:

Unlike the GENIUS Act, which was signed into law on July 18, 2025, the Anti-CBDC Surveillance State Act has not yet been enacted. Its passage through the House is significant, but the Senate path remains uncertain. Cross-border clients should monitor developments closely — the outcome will have meaningful implications for the digital currency landscape on the U.S. side of any cross-border financial plan.

Key Provisions

1. Ban on Direct CBDC Issuance

o Fed cannot offer digital currency, accounts, or wallets directly to individuals.

2. Ban on Indirect CBDC Issuance

o Prohibits the Fed from issuing CBDC via intermediaries or financial institutions.

3. Prohibition on Fed CBDC Testing or Use

o Forbids testing, developing, or implementing a CBDC for monetary policy.

4. Congressional Authorization Required

o Any future Fed CBDC initiative requires explicit congressional approval.

5. Privacy Protections

o Clarifies the ban does not apply to private, permissionless digital cash that retains physical cash privacy.

Note for Cross-Border Clients: The bill explicitly clarifies that its ban does not apply to private, permissionless digital assets that retain the privacy characteristics of physical cash. This means stablecoins and existing crypto assets held by cross-border investors are not affected by this legislation — the target is exclusively a Fed-issued retail CBDC.

Proponents: Privacy, Sovereignty & Institutional Support

• Whip Emmer argues the Act preserves financial privacy, prevents surveillance, and guards against control by unelected bureaucrats.

• Rep. Byron Donalds, echoing Trump’s stance, described CBDC as a threat to liberty and “globalist tyranny,” stressing support for private-sector innovation.

• Credit unions, the American Bankers Association, and other financial groups endorse the bill, citing the need to protect member data, preserve community banking, and prevent the Fed from displacing traditional financial services.

The Canada Divergence:

While the U.S. moves toward blocking a government-issued digital dollar, the Bank of Canada has been conducting active CBDC research through its own Digital Canadian Dollar project. This creates a meaningful policy divergence: cross-border families may eventually operate across two digital currency environments with different privacy standards, interoperability considerations, and regulatory frameworks. Whether Canada ultimately launches a CBDC will significantly affect how cross-border digital payments function for dual citizens and snowbirds.

Critics: Falling Behind Global Trends & Policy Risks

• Financial Privacy Advocates & Economists worry the U.S. might lose ground as over 70 countries explore CBDCs—potentially weakening dollar dominance.

• Christopher Smart (FT) calls the ban “shameful,” arguing thoughtful CBDC design could safeguard privacy while enhancing international payments.

• Rep. Maxine Waters cautions that CBDCs could bolster financial stability and reduce costs, and claims the bill could hinder innovation and constrain the Fed.

Implications Across Sectors

Banking

• Preserves current model: Banks and credit unions maintain deposit relationships and customer data control.

• Hinders innovation: Without Fed-issued digital accounts, banks may need to partner with private fintechs for digital currency services.

Investment

• Stable funding: Prevents sudden deposit drains to Fed wallets.

• Potential opportunity cost: Markets may miss out on efficiency gains from a well-architected digital dollar.

For Cross-Border Investors:

A U.S. CBDC ban strengthens the position of private stablecoins — now regulated under the GENIUS Act — as the primary vehicle for digital dollar transactions. For cross-border clients using stablecoins to manage USD-CAD transfers, this reinforces the importance of understanding the GENIUS Act compliance framework, T1135 reporting obligations for Canadian residents, and FBAR requirements for U.S. persons holding digital assets on foreign platforms.

Crypto & Digital Assets

• Private sector stays central: Stablecoins and permissionless digital assets continue under existing regulatory frameworks.

• Limits government competition: Crypto firms avoid facing state-issued competition in retail digital currency.

What’s Next?

The Anti-CBDC Surveillance State Act is still moving through the legislative process, but its direction is clear: the U.S. is choosing private-sector innovation over government-issued digital currency. For cross-border investors, the more immediate planning question is not whether a U.S. CBDC will exist — it likely will not — but how the growing divergence between U.S. and Canadian digital currency policy will affect cross-border payments, reporting obligations, and portfolio structure in the years ahead. If you hold digital assets across both countries, now is the right time to ensure your cross-border financial plan accounts for this evolving landscape.

For more, check out our articles on the GENIUS Act, and the CLARITY Act, on our blog at 49thparallelwealthmanagement.com.

Frequently Asked Questions

What is the Anti-CBDC Surveillance State Act?

The Anti-CBDC Surveillance State Act (H.R. 1919) is a U.S. bill introduced by Rep. Tom Emmer in March 2025 that would prohibit the Federal Reserve from issuing a central bank digital currency — either directly to consumers or through financial intermediaries. It would also ban the Fed from testing or developing a CBDC for monetary policy purposes without explicit congressional approval. The bill passed the U.S. House of Representatives on July 17, 2025 by a vote of 219–210 and is currently awaiting Senate action.

Has the Anti-CBDC Act been signed into law?

No — not yet. As of mid-2025, the bill has passed the U.S. House but has not been voted on by the Senate or signed by the President. Its legislative path remains uncertain. This is an important distinction from the GENIUS Act, which was signed into law on July 18, 2025. Cross-border investors should monitor Senate developments, as the outcome will affect the long-term digital currency landscape on the U.S. side of any cross-border financial plan.

Does the Anti-CBDC Act affect stablecoins or existing crypto assets?

No. The bill explicitly targets only a Federal Reserve-issued retail central bank digital currency. It does not affect private stablecoins, permissionless digital assets, or existing cryptocurrency holdings. Stablecoins are separately governed by the GENIUS Act, which was signed into law in July 2025 and establishes a federal framework for payment stablecoins. Cross-border investors holding stablecoins or other digital assets are not directly affected by the Anti-CBDC Act.

Is Canada planning to launch a CBDC?

Canada has been conducting active research into a Digital Canadian Dollar through the Bank of Canada, though no formal launch decision has been made. Unlike the U.S., Canada has not passed legislation blocking a government-issued digital currency. This creates a growing policy divergence: cross-border families may eventually operate across two digital currency environments with different privacy standards, interoperability considerations, and regulatory frameworks. Whether Canada ultimately launches a CBDC will significantly affect how cross-border digital payments function for dual citizens and Canadian snowbirds with U.S. accounts.

What does a U.S. CBDC ban mean for cross-border payments between Canada and the U.S.?

If the Anti-CBDC Act becomes law, it reinforces the role of private stablecoins — now regulated under the GENIUS Act — as the primary vehicle for digital dollar transactions in the U.S. For cross-border clients using stablecoins to manage USD-CAD transfers, this means the GENIUS Act compliance framework becomes the relevant regulatory reference point. Canadian residents holding U.S.-based stablecoins must still consider T1135 reporting obligations, and U.S. persons holding digital assets on foreign platforms must continue to assess their FBAR requirements regardless of the CBDC debate.

How does the Anti-CBDC Act fit with the GENIUS Act and CLARITY Act?

The three bills form a coordinated framework for U.S. digital finance. The CLARITY Act establishes the taxonomy for how digital assets are classified and regulated between the SEC and CFTC. The GENIUS Act overlays a specific regulatory framework for private payment stablecoins. The Anti-CBDC Act completes the picture by ensuring the Federal Reserve cannot enter the market as a competitor through a government-issued digital dollar — leaving innovation and competition to the private sector. Together, these three bills define the architecture of U.S. digital finance for the foreseeable future.