T1135 Foreign Reporting: The Form That Can Cost More Than the Tax

By Lucas Wennersten, CFP® (US & Canada), CFA · 8-minute read

Part of Seven Figures, Two Countries — cross-border wealth decisions for $5M+ Canada-US families.

Home › Blog › T1135 Foreign Reporting

This article is general education, not personalized tax, legal, or financial advice. Foreign-reporting rules are intricate and fact-specific, and penalties are severe. Before relying on any position, speak with a cross-border advisor.

It is the most deceptively dangerous form in the cross-border tax system: an information return that calculates no tax, yet carries penalties that can run into the tens of thousands of dollars. Form T1135, the Foreign Income Verification Statement, asks Canadian residents to give the CRA an annual inventory of their foreign property. For a wealthy family that has moved to Canada — or a Canadian who has built a portfolio of US and offshore assets — it is not optional, it is not difficult to trigger, and getting it wrong is one of the few mistakes in cross-border tax planning where the punishment has nothing to do with how much tax you actually owe.

Here is what T1135 actually requires at this level of wealth, what counts and what doesn’t, the arrival-year rule that surprises new residents, and why the penalties deserve real attention.

Who has to file — and why $5M+ families almost always do

You must file T1135 if, at any point in the year, the total cost of your “specified foreign property” exceeds CAD $100,000. Three features of that sentence trip people up.

First, it is based on cost, not market value — the historical cost of what you bought, converted to Canadian dollars at the exchange rate on the purchase date. Second, it is an “at any time” test: cross $100,000 for a single day and you must file for the whole year, even if you held nothing foreign on December 31. Third, the $100,000 threshold has not moved in decades, so as portfolios and exchange rates have grown, far more people cross it than the number suggests. At $5 million and above, you are essentially always over it — and almost always into the detailed-reporting tier described below.

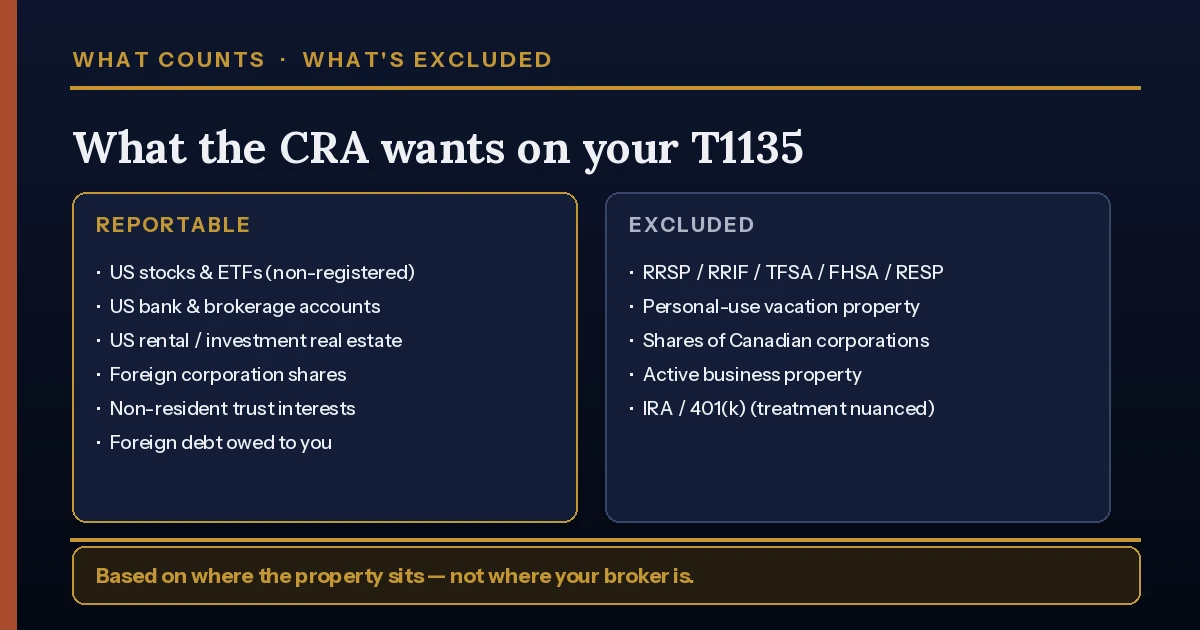

What counts as specified foreign property — and what doesn’t

This is where most errors happen, because the line is not where people expect it. The defining question is not where your broker is — it is where the property is situated.

Reportable, even when held through a Canadian brokerage: US and other foreign stocks and ETFs in a non-registered account, foreign bank accounts, US rental or investment real estate, debt owed by non-residents, and interests in non-resident trusts (many popular US-listed ETFs are technically trusts). A US-dollar account at a Canadian bank holding Apple shares is foreign property; the Canadian broker does not change that.

Excluded, even above $100,000: property inside Canadian registered plans (RRSP, RRIF, TFSA, RESP, FHSA) even when they hold foreign investments, personal-use property such as a vacation home you never rent out, shares of a Canadian corporation even if it owns foreign assets, and property used mainly in an active business. The treatment of US retirement accounts such as IRAs and 401(k)s is genuinely nuanced and fact-specific — do not assume, confirm.

Simplified vs detailed reporting — and why you’re likely in the detailed tier

There are two reporting methods, and the threshold between them matters at this level of wealth. If your total cost of specified foreign property stays between $100,000 and $250,000 throughout the year, you can use the simplified method — reporting by category and country band rather than asset by asset. Once the total cost hits $250,000 at any time in the year, you move to detailed reporting: each property, its country, maximum cost during the year, year-end cost, income generated, and gains or losses on disposition.

For a $5M+ household, detailed reporting is effectively permanent. The practical burden is record-keeping: tracking the Canadian-dollar cost of every foreign holding, including the exchange rate on each purchase, across potentially many accounts. The families who struggle with T1135 are rarely the ones who refuse to comply — they are the ones whose foreign holdings are scattered across institutions and never consolidated. This is where it belongs inside your broader cross-border wealth management process, not a once-a-year scramble in April.

The arrival-year rule new residents miss

Here is the nuance that ties directly to any recent move: in the year you first become a Canadian tax resident, you are exempt from filing T1135. Your first obligation is the following year. This dovetails with the arrival cost-base reset we cover in the concentrated stock guide — the year you land is unusual on several fronts, and it pays to know which obligations start immediately and which start a year later.

The flip side: the exemption is only for your very first year, and only if it is genuinely your first year of Canadian residency. From year two onward, the full requirement applies, and the CRA increasingly receives the underlying data anyway through international information-sharing — so a quietly unfiled T1135 is far easier to detect than it once was.

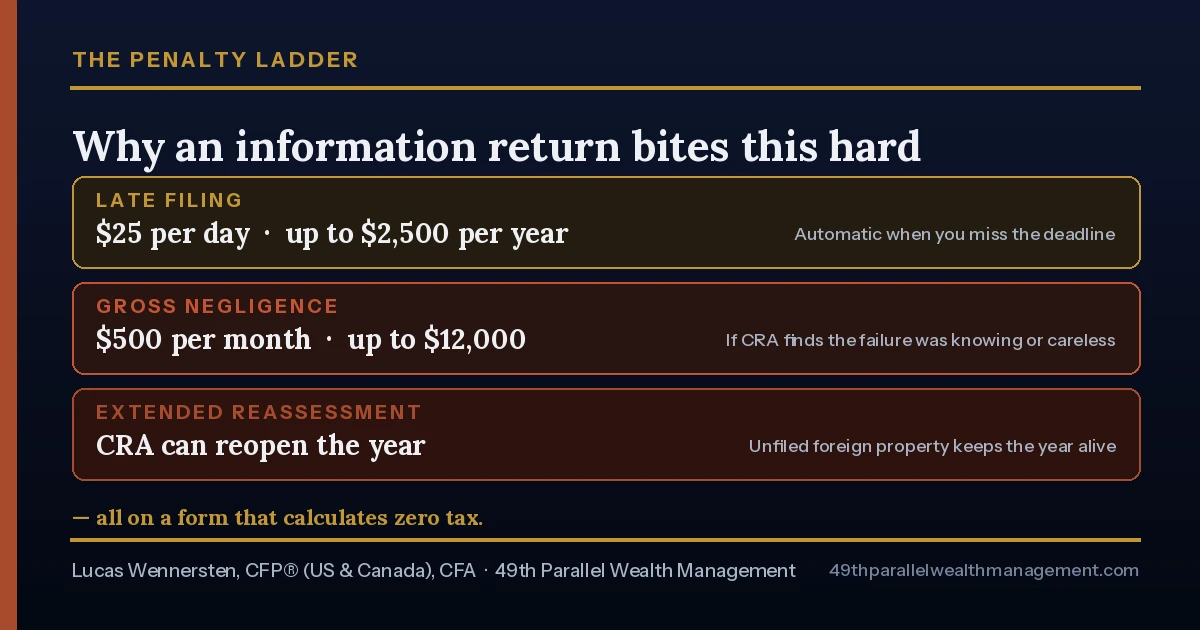

The penalties: why an information return bites this hard

Because no tax is calculated on T1135, people underrate it — until they see the penalty schedule. The basic late-filing penalty is $25 per day, with a minimum of $100 and a maximum of $2,500 per year, per missed form. Where the CRA finds the failure was made knowingly or through gross negligence, the penalty rises to $500 per month, up to $12,000. Continued failure after a formal demand, and additional penalties tied to unreported foreign income, can push exposure higher still — and a failure to file can extend the period during which the CRA may reassess the year.

The asymmetry is the whole point: a family can owe zero additional Canadian tax on its foreign holdings and still face five-figure penalties purely for failing to file the inventory on time. It is one of the highest penalty-to-tax ratios in the system, which is exactly why it deserves a place in the annual process rather than a footnote.

T1135 is not the US forms — a US person in Canada files all of them

A frequent and expensive confusion: T1135 is a Canadian form, entirely separate from the US foreign-reporting regime. A US citizen living in Canada may also have to file the FBAR (FinCEN Form 114) for foreign financial accounts and IRS Form 8938 under FATCA — and, confusingly, “foreign” means the opposite thing on each side of the border. From Canada’s perspective US assets are foreign; from the US perspective Canadian assets are. Dual filers report their cross-border holdings to both tax authorities, on different forms, with different thresholds and definitions. Residency status under the Canada-United States Tax Convention determines who is a Canadian resident for this purpose in the first place.

A T1135 checklist for cross-border families

To keep T1135 from becoming a problem:

- Total the Canadian-dollar cost of all non-registered foreign property — if it ever exceeds $100,000 in the year, you file.

- Track cost in Canadian dollars at the exchange rate on each purchase date, not current value.

- Confirm whether you are in the simplified or detailed tier (over $250,000 cost means detailed).

- Consolidate scattered foreign accounts so the annual reporting is manageable and accurate.

- If you became a Canadian resident this year, confirm the first-year exemption applies — then plan for filing next year.

- If you are a US person, coordinate T1135 with your FBAR and Form 8938 filings; the definitions differ.

- Refer to the official CRA materials for the current form and instructions, including Form T1135 and the CRA guidance for newcomers to Canada.

The bottom line

T1135 is the rare obligation where the cost of carelessness is fixed, large, and entirely avoidable. It calculates no tax, but it punishes silence — and for wealthy cross-border families with US accounts, US real estate, and scattered foreign holdings, the threshold is crossed automatically and the detailed-reporting burden is permanent. Built into an annual process, it is routine. Left to memory, it is one of the easiest ways to turn a zero-tax year into a five-figure penalty.

Frequently asked questions

Who has to file Form T1135?

Any Canadian resident — individual, corporation, or certain trusts and partnerships — whose total cost of specified foreign property exceeds CAD $100,000 at any point in the year. It applies to factual residents, deemed residents, and certain others, including US citizens living in Canada.

What counts as specified foreign property?

Foreign stocks and ETFs in non-registered accounts, foreign bank accounts, foreign rental or investment real estate, debt owed by non-residents, and interests in non-resident trusts, among others. It is based on where the property is situated, not where your broker is located.

Are my US stocks held through a Canadian broker reportable?

Yes. US and other foreign securities held in a non-registered account are specified foreign property even when the brokerage is Canadian. The location of the underlying property, not the institution, is what matters.

Is my US vacation home reportable on T1135?

Generally no, if it is genuinely personal-use property that you do not rent out. If you rent it, it becomes reportable. A capital gain on sale is still taxable in Canada regardless of the T1135 treatment.

Are the foreign holdings in my RRSP or TFSA reportable?

No. Property held inside Canadian registered plans — RRSP, RRIF, TFSA, RESP, FHSA — is excluded from T1135 even if those plans hold foreign investments.

What is the difference between simplified and detailed reporting?

If your total cost of specified foreign property stays between $100,000 and $250,000 throughout the year, you can report by category using the simplified method. Once it reaches $250,000 at any time, you must report each property in detail — country, maximum and year-end cost, income, and gains or losses.

Do I have to file T1135 in my first year as a Canadian resident?

No. New residents are exempt from filing T1135 for the year they first become a Canadian tax resident. The obligation begins the following year, and only the first year qualifies for the exemption.

What are the penalties for not filing T1135?

The basic late-filing penalty is $25 per day, minimum $100 and maximum $2,500 per year. Where the failure is knowing or grossly negligent, it rises to $500 per month up to $12,000, with further penalties and an extended reassessment period possible — all on a form that calculates no tax.

Is T1135 the same as the US FBAR or Form 8938?

No. T1135 is a Canadian form. FBAR (FinCEN Form 114) and Form 8938 are US forms. A US citizen living in Canada may have to file all of them, on different forms, with different thresholds and definitions — and “foreign” means opposite things on each side of the border.

Not sure your foreign holdings are being reported correctly — or whether you crossed the threshold this year? Book a complimentary consultation and we will review your cross-border reporting before the CRA does.

This article is general education, not personalized tax, legal, or financial advice. Rules and thresholds change over time. Speak with a cross-border advisor before acting. — 49th Parallel Wealth Management.

From the Desert to the Tundra™