Home Sale Tax: How the US 2-of-5 Rule Compares to Canada — and the Four Bills Trying to Change It

By Lucas Wennersten, CFP® (US & Canada), CFA · 9 minute read · Updated May 14, 2026

The conversation about how the US taxes home sales is no longer hypothetical. Between July 2025 and January 2026, at least four bills were introduced in Congress proposing to either eliminate or substantially raise the capital gains exclusion on primary home sales. President Trump has publicly supported the idea. None of the bills has been enacted as of May 2026, but the topic is one of the most active in current US tax debate.

What makes this interesting from a cross-border perspective: the US is debating whether to move closer to a system Canada has already had for decades. Canada doesn’t tax capital gains on a principal residence at all (with some technical nuances). The US currently taxes everything above $250,000 ($500,000 married) — a cap unchanged since 1997.

For cross-border families, the answer to ‘how is my home sale taxed?’ depends on which country you’re tax-resident in, when you became a resident there, and what the property’s history looks like. A bill that changes US law could shift the equation considerably. This article walks through current US law, the Canadian model, the four pending bills, and the cross-border mechanics that matter most for dual citizens and families with property on both sides of the border.

Current US Law: The 2-of-5 Rule (Section 121)

Under IRS Publication 523 (Selling Your Home) and Internal Revenue Code Section 121, US homeowners can exclude up to $250,000 in capital gains from taxation if filing single, or $500,000 if married filing jointly. The exclusion applies when:

- You owned the home for at least 2 of the past 5 years (the ownership test)

- You used the home as your primary residence for at least 2 of the past 5 years (the use test)

- You haven’t claimed the home sale exclusion on another property in the past 2 years

Two practical points often missed: the 2-year periods don’t need to be continuous (you can leave and return, as long as the total adds up). And the cap has not been indexed for inflation since 1997. The National Association of Realtors estimates that approximately 34% of US homeowners now exceed the $250,000 threshold and 10% exceed $500,000 — far more than when the rule was written.

Special suspension for armed forces, foreign service, and intelligence personnel: Section 121(d)(9) allows up to 10 years of suspension on the 2-of-5 rule for qualified extended duty. This is the only formal break the existing rule gives to Americans living abroad.

The Canadian Principal Residence Exemption

Canada’s principal residence exemption works differently. There is no cap. The full capital gain on a principal residence can be exempt from Canadian tax, provided the property qualifies for each year of ownership. For properties not used exclusively as a principal residence, the exemption is prorated by a formula:

Tax-Free Portion = (# of years designated as principal residence + 1) ÷ (# of years owned)

Three rules that often surprise people:

- A family unit (you, your spouse/common-law partner, and minor children together) can only designate ONE property as principal residence per tax year. This rule has been in place since 1981.

- Since 2016, the sale of any principal residence must be reported on Schedule 3 and Form T2091, even when fully tax-exempt. Failure to report triggers penalties and loss of the exemption.

- Vacant land and recreational properties can qualify as principal residence, but the ‘ordinarily inhabited’ test must be met. Even a few days a year of use can qualify a cottage.

Four Bills Currently Trying to Change US Law

As of May 2026, four bills targeting the home sale exclusion are pending in the House Ways and Means Committee. None has advanced to a floor vote. Here’s the lineup:

| Bill | Sponsor | What It Does | Status |

| No Tax on Home Sales Act (H.R. 4327) | Marjorie Taylor Greene (R-GA), July 2025 | Eliminates the cap entirely; full gain on principal residence tax-free if 2-of-5 met | In committee |

| More Homes on the Market Act | Jimmy Panetta (D-CA) + Mike Kelly (R-PA), 2025 — bipartisan with 100+ cosponsors | Raises exclusion to $500K single / $1M MFJ AND indexes for inflation going forward | In committee |

| Don’t Tax the American Dream Act | Craig Goldman (R-TX), January 13 2026 | Eliminates cap if homeowner lived in property at least 2 years (similar to Greene) | In committee |

| Middle Class Home Tax Elimination Act | Scott Fitzgerald (R-WI), January 2026 | Eliminates federal capital gains tax on primary home sales for middle-income filers | In committee |

Trump publicly supported eliminating capital gains on home sales in July 2025. The Joint Committee on Taxation has not produced a formal scoring of these specific bills, but JCT scoring of similar proposals suggests the federal revenue loss could run into the tens of billions annually. Bipartisan support for the More Homes Act gives it the most realistic path to enactment, but all four bills remain in committee with no scheduled markup as of May 2026.

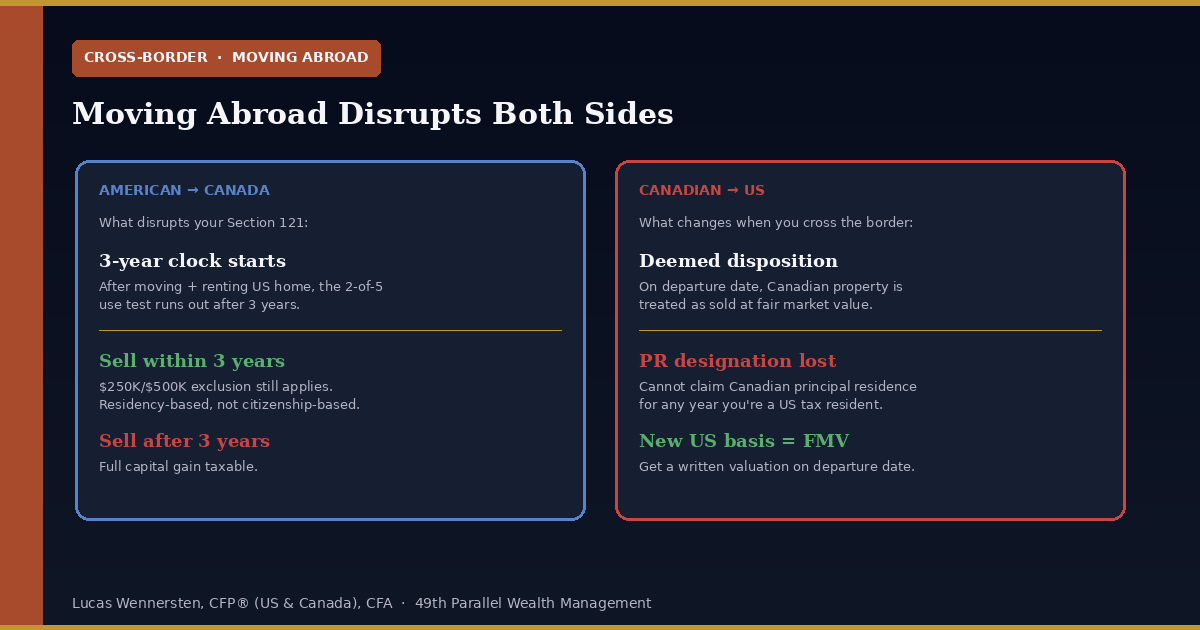

What Happens When You Move Abroad?

This is where the cross-border family pain begins. The home sale exclusion in BOTH countries depends on residency facts that get disrupted when you move across the border. Three scenarios cover most cases:

American moving to Canada with a US home

If you keep the US home and rent it out after moving, the 2-of-5 test starts ticking. After 3 years of non-use, you lose Section 121 eligibility entirely. If you sell within those 3 years, the full $250K/$500K exclusion applies even though you’re living in Canada (the test is residency-based, not citizenship-based). Plan the timing carefully: a sale 2 years 11 months after moving generally qualifies; a sale 3 years 1 month later does not.

On the Canadian side: you don’t become eligible to claim Canadian principal residence on the US home unless you actually move into it during residency in Canada — usually impossible if you’re now living in Toronto. If the property is rented while you’re a Canadian resident, you’ll report the rental income on your T1 and pay Canadian tax on the eventual capital gain (50% inclusion, or 66.67% for gains above $250,000 in a year after June 2024).

Canadian moving to the US with a Canadian home

Canada applies a deemed disposition on the date you become a non-resident — your worldwide property is treated as if sold at fair market value. For property qualifying as principal residence up to that date, the deemed disposition rules generally don’t trigger Canadian tax (the principal residence exemption covers it). But the new cost basis for US tax purposes is the FMV on your departure date, NOT what you originally paid. This is a critical point: you ‘step up’ your basis to FMV when crossing the border for US tax purposes.

If you later sell the Canadian property as a US tax resident, you may qualify for the US Section 121 exclusion IF you meet the 2-of-5 test. The current proposals (Greene, Goldman, Fitzgerald) would relax or eliminate this requirement, potentially saving cross-border movers significant US tax on their pre-departure home appreciation.

Canadian selling a US vacation or rental property

This is the FIRPTA case — and the home sale exclusion debate is largely irrelevant here. Section 121 only applies to a primary residence, not vacation or rental property. Canadians selling US property pay 15% FIRPTA withholding at closing, file Form 1040-NR, and report the gain on the Canadian return as well. See our cross-border real estate guide for the full FIRPTA mechanics. Even if Greene’s bill passes, FIRPTA continues to apply to non-resident sellers regardless of whether the property was once a primary residence.

Cross-Border Planning Considerations

Three planning considerations matter most for families with property exposure on both sides of the border:

Timing your move around a sale

Whether to sell BEFORE or AFTER becoming non-resident in the home country is one of the largest tax decisions in any cross-border move. Selling before crossing usually means the home-country exclusion (Section 121 in the US, principal residence exemption in Canada) applies cleanly. Selling after crossing introduces the destination country’s tax regime and the home country’s non-resident rules — typically much more complex and often more expensive.

Departure tax planning for Canadians becoming US residents

Canada’s deemed disposition can include real estate, but principal residence designation can shelter the home portion. Crystallizing the FMV at departure is important — it sets your new US cost basis. Documentation matters: get a written valuation as of your departure date, preferably from a licensed appraiser. CRA Form T1243 captures the deemed disposition; the US side uses the FMV as your basis on any future Form 1040 sale reporting.

Watch what Congress actually does — but don’t plan around it

Tax bills move slowly. The current $250K/$500K caps have been unchanged for 28 years. Canada-US tax strategy should be built around current law, with awareness of pending legislation. If a bill passes, planning can adjust. If you make decisions today assuming a bill will pass — and it doesn’t — you may face unexpected tax bills.

The Bigger Question: Should the US Adopt Canada’s Approach?

Four design options dominate the US debate:

- Eliminate the cap entirely (Greene, Goldman, Fitzgerald approaches) — full alignment with Canadian model

- Raise the cap and index for inflation (More Homes Act) — moderate reform that mostly addresses the 1997 cap erosion

- Adopt a Canadian-style formula prorating exemption by years of principal use — more administratively complex but more equitable for those who rent out their homes

- Leave Section 121 alone — keep the existing 2-of-5 rule and $250K/$500K cap; rely on inflation to keep adjusting the underlying tax burden

Critics of full elimination argue it disproportionately benefits the wealthy (Yale Budget Lab analysis from July 2025 found the wealthiest 5% of homeowners would capture most of the benefit). Critics of the status quo point out that decades-old caps no longer match housing reality — a $300,000 home in 1997 has often appreciated past the exclusion threshold even for middle-class sellers. The bipartisan More Homes Act splits the difference: doubles the cap, indexes for inflation, doesn’t go to full elimination. It has the most cosponsors of any of the four bills.

The Bottom Line

The US is having a real policy conversation about whether to move toward Canada’s approach to home sale taxes. Four active bills + presidential support + a bipartisan companion = real legislative momentum. But none has passed, and tax bills tend to move slowly.

For cross-border families, the more pressing reality is the mechanics that already apply: Section 121’s 2-of-5 rule, Canada’s deemed disposition on departure, FIRPTA on non-resident sales, and the principal residence designation rules. These create real planning opportunities — and real traps — regardless of whether Congress acts in 2026 or 2027.

If you’re contemplating a move across the border, or own property on both sides, the home sale tax question is rarely independent of the broader cross-border tax picture. Book a complimentary consultation with 49th Parallel Wealth Management to coordinate the timing of any home sale with your broader cross-border financial plan.

Frequently Asked Questions

Q: What is the No Tax on Home Sales Act?

A: H.R. 4327, introduced by Representative Marjorie Taylor Greene (R-GA) in July 2025, would eliminate the federal capital gains tax on the sale of a primary residence by removing the current $250,000 single / $500,000 married caps. The 2-of-5 ownership and use rules would remain. The bill is still in the House Ways and Means Committee as of May 2026 with no scheduled markup.

Q: What are the four bills in Congress trying to change US home sale tax?

A: Four bills are currently pending: the No Tax on Home Sales Act (Greene, full elimination), the More Homes on the Market Act (Panetta/Kelly bipartisan, raises to $500K/$1M with inflation indexing), the Don’t Tax the American Dream Act (Goldman, eliminates cap if 2-year residence met), and the Middle Class Home Tax Elimination Act (Fitzgerald, middle-income focused elimination). All are in the House Ways and Means Committee.

Q: How is a home sale taxed in Canada vs the US?

A: Canada exempts capital gains on a designated principal residence entirely, with no dollar cap, using a formula proration if the property was not principal residence for all years owned. The US allows an exclusion of $250,000 single or $500,000 married filing jointly, but only if you owned and used the home as your primary residence for at least 2 of the past 5 years. The US cap has not been indexed for inflation since 1997.

Q: What is the US 2-of-5 rule?

A: Under Section 121 of the Internal Revenue Code, you must have owned the home for at least 2 of the past 5 years (ownership test) AND used it as your primary residence for at least 2 of the past 5 years (use test) to claim the home sale exclusion. The 2-year periods do not need to be continuous. You also cannot have claimed the exclusion on another property within the past 2 years.

Q: What happens to my US home sale exclusion if I move to Canada?

A: If you keep the US home and rent it out after moving to Canada, the 2-of-5 use test starts ticking. After 3 years of non-use, you lose Section 121 eligibility on that property. If you sell within 3 years of moving, the full $250K/$500K exclusion still applies (it’s residency-based, not citizenship-based). After 3 years, you’re fully taxable on the gain. Time the sale carefully if you anticipate a move.

Q: How does Canada’s principal residence exemption work?

A: Canada applies a formula: tax-free portion = (years designated as principal residence + 1) ÷ years owned. A family unit can designate only ONE property per year as principal residence. Since 2016, every principal residence sale must be reported on Schedule 3 and Form T2091, even when fully tax-exempt. Failure to report triggers penalties and loss of the exemption.

Q: Does the home sale exclusion apply to Canadians selling US vacation property?

A: No. Section 121 only applies to a primary residence. Vacation homes and rental properties don’t qualify for the exclusion. Canadians selling US vacation property pay 15% FIRPTA withholding at closing, file Form 1040-NR to compute actual capital gains tax, and report the gain on their Canadian tax return as well (with a foreign tax credit for US tax paid). Even if Greene’s bill passes, FIRPTA continues to apply to non-resident sellers.

Q: Are there exceptions to the 2-of-5 rule for Americans living abroad?

A: Yes. Section 121(d)(9) allows up to 10 years of suspension on the 2-of-5 use test for armed forces, foreign service, and intelligence officials on qualified extended duty. There is no general ‘expat suspension’ for Americans living abroad for other reasons — the standard 2-of-5 rule applies. The foreign earned income exclusion (Section 911) doesn’t help with home sale gain.

Q: Should I sell my US home before or after moving to Canada?

A: Generally, selling BEFORE you become a Canadian tax resident gives the cleanest tax outcome — the full Section 121 exclusion applies to the US side, and Canada has no claim on the gain because you’re not a Canadian resident yet. Selling AFTER becoming a Canadian resident may still qualify for Section 121 (if 2-of-5 met) but the gain above the exclusion will be reported on both your US return and your Canadian T1, with foreign tax credits coordinating. Specific timing depends on home appreciation, mortgage situation, and the residency status start date — worth modeling before the move.

This article is for general educational purposes and is not tax, legal, or investment advice. Tax rules, pending legislation, and treaty positions change. The four bills referenced were active in Congress as of May 2026; their status may change. Confirm current US Section 121 rules, Canadian principal residence rules, and bill status with a qualified cross-border tax advisor before any home sale decision.