How Inflation Affects the Stock Market: What Investors Need to Know

By Lucas Wennersten, CFP® (US & Canada), CFA · 49th Parallel Wealth Management

Reading time: ~6 minutes · Published: July 11, 2025 · Updated: April 26, 2026

DISCLAIMER This article is for informational and educational purposes only. It does not constitute financial, investment, tax, or legal advice. The information presented reflects general principles and may not apply to your specific situation. Past performance is not indicative of future results. Consult a qualified cross-border financial advisor before making any investment or portfolio decisions. 49th Parallel Wealth Management is registered as an investment adviser in the United States. |

Inflation is one of the most closely watched economic indicators — and for good reason. It shapes everything from your grocery bill to your retirement portfolio. While a modest amount of inflation is normal in a healthy economy, high or rising inflation has historically created headwinds for equity markets.

The relationship is not as simple as “prices go up, therefore stocks go up.” The reality is more nuanced: companies charging more for their products does not automatically translate into stronger earnings or higher stock prices. For investors navigating this environment — especially those with assets and expenses in two different countries — understanding how inflation actually moves through corporate earnings and market valuations is essential.

This article breaks down the key transmission channels: how inflation affects corporate revenues and margins, how central banks respond and what that means for valuations, and why cross-border investors face an additional layer of complexity that single-country investors do not.

|

The Revenue Illusion: More Isn’t Always Better

When prices rise, companies can charge more per unit. At face value, this looks like a revenue windfall — and sometimes it is. But in a sustained inflationary environment, something else happens: consumer behaviour shifts.

- Spending becomes more selective. People turn to cheaper alternatives, cut back on non-essentials, and delay major purchases.

- Brand loyalty erodes. When price becomes the primary consideration, premium brands lose their pricing advantage.

- Unit volumes fall. Even if each transaction is worth more, the number of transactions can decrease enough to flatten or reduce total revenue.

Companies sometimes respond by reducing the size or quantity of a product without changing the sticker price — a phenomenon widely known as shrinkflation. While this preserves short-term sales volumes, it typically damages brand equity over time as consumers notice the change.

The result is that higher prices do not reliably produce higher profits. Revenue growth during inflation is often illusory when adjusted for the full picture of volume, cost, and consumer behaviour.

The Margin Squeeze: Rising Input Costs, Uncertain Pricing Power

Inflation does not just affect what companies charge — it also affects what they pay. Input costs for raw materials, energy, labour, and transportation typically rise during inflationary periods, and often unpredictably.

This creates a compounding challenge for businesses:

- Production costs become harder to forecast. Companies cannot price strategically when they cannot reliably project what future inputs will cost.

- Buyers rush to lock in lower prices. Anticipating further increases, purchasing managers accelerate orders, which can strain supply chains, deplete inventory, and push prices higher still.

- The pass-through dilemma. Businesses face a difficult choice: pass rising costs to customers and risk losing volume, or absorb the costs and watch profit margins compress.

For investors, this margin pressure translates directly into earnings risk. Weaker margins typically produce earnings disappointments, which reprice equities downward. Sectors with limited pricing power — those selling commoditised goods or services where customers can easily switch — are most vulnerable.

How Central Banks Respond: Interest Rates and Stock Valuations

Beyond the direct impact on corporate earnings, inflation shapes equity markets through a second, structural channel: central bank policy.

When inflation runs above target, central banks raise interest rates to reduce liquidity and slow economic activity. The Federal Open Market Committee targets an inflation rate of approximately 2% — above that level, the policy response is typically rate increases.

Higher rates affect stock valuations in two concrete ways:

- Borrowing costs rise for companies and consumers alike. Capital becomes more expensive, investment slows, and consumer demand moderates.

- Future earnings are discounted more aggressively. Discounted cash flow models assign lower present values to future earnings when the discount rate rises. This is why growth-oriented companies and technology stocks tend to underperform most during inflationary periods — their valuations rest heavily on earnings years in the future, and those distant earnings are worth meaningfully less at higher discount rates.

The combined effect — margin compression from rising costs plus multiple compression from rising rates — is why equity markets tend to struggle when inflation runs persistently high.

|

Inflation and the Cross-Border Portfolio

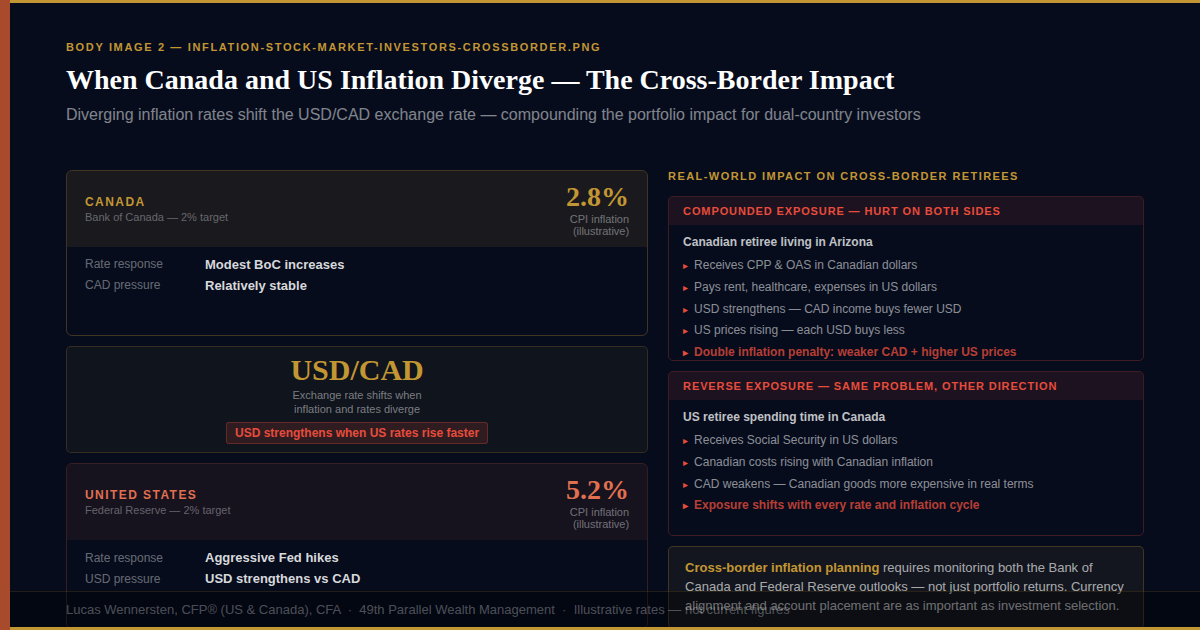

For investors with assets and expenses in both Canada and the United States, inflation introduces a layer of complexity that single-country investors simply do not face: the interaction between two different inflation environments and the exchange rate that connects them.

Canadian and US inflation rates can diverge materially. When they do, the Bank of Canada and the Federal Reserve often respond with different rate adjustments at different times. Those diverging rate paths shift the USD/CAD exchange rate — and that movement directly affects the real purchasing power of cross-border income and savings.

Consider a Canadian retiree living in Arizona. Their Canada Pension Plan and Old Age Security income arrives in Canadian dollars. Their rent, healthcare, and day-to-day expenses are in US dollars. If US inflation runs hotter than Canadian inflation and the USD strengthens as a result, their Canadian income buys fewer US dollars. They face an inflation penalty on both sides: rising US prices, and a less favourable exchange rate.

The reverse is equally true. A US retiree spending time in Canada faces the same structural exposure in the opposite direction. The underlying portfolio return is only one part of the equation — currency movement can add or subtract meaningfully from the real value of cross-border income streams.

Managing this requires more than a standard inflation hedge. Thoughtful cross-border investors consider:

- Currency alignment — ensuring that income and expenses are reasonably matched by currency, where possible

- Account placement — holding USD-denominated investments in US accounts and CAD-denominated investments in Canadian accounts where tax rules permit

- Inflation differential monitoring — tracking both the Bank of Canada and Federal Reserve inflation outlooks as part of any currency exposure review

This is one reason why cross-border financial planning differs fundamentally from planning within a single jurisdiction. Inflation does not affect both sides of the border equally, and the gap matters.

Disinflation and Deflation: Not the Same Thing

Disinflation: A Market-Friendly Trend

Disinflation refers to a slowdown in the rate of inflation — prices are still rising, but more slowly. This environment is generally constructive for equity markets. Input cost pressures ease, companies can plan more effectively, profit margins tend to recover, and consumer confidence improves. Investors typically reward disinflation with higher valuations, particularly in cyclical and growth sectors that were hit hardest during the inflationary period.

Deflation: A More Serious Problem

Deflation — an outright decline in the general price level — is typically worse than inflation for equity markets, even though falling prices may seem appealing on the surface. Deflation signals a contraction in demand, and it creates a self-reinforcing cycle that is difficult to break:

- Consumers delay purchases, anticipating further price declines.

- Businesses respond by cutting costs and reducing staff.

- Lower employment reduces consumer demand further.

- Companies face pressure to reduce prices to generate cash flow, which pushes prices lower still.

In deflationary environments, stock markets typically perform poorly, particularly in sectors tied to consumer spending, real estate, and discretionary goods. Corporate revenues fall in nominal terms even before margin pressure is considered.

Key Takeaways

Scenario | Description | Stock Market Impact |

Rising Inflation | Prices increasing quickly; input costs and uncertainty rising | Negative — lower margins, higher rates, multiple compression |

Disinflation | Inflation slowing down but still positive | Positive — margin recovery, stable costs, confidence returns |

Deflation | Prices falling broadly across the economy | Negative — signals demand weakness, self-reinforcing contraction |

Cross-Border | Canadian & US inflation diverge; USD/CAD shifts | Compounded — affects both real returns and exchange rate purchasing power |

Conclusion

Inflation is not a single event — it is a cycle with distinct phases, each of which creates a different environment for investors. Rising inflation compresses margins, raises the cost of capital, and reduces the present value of future earnings. Disinflation relieves those pressures and tends to be constructive for equities. Deflation signals something more serious: a contraction in demand that stock markets typically price quickly and harshly.

For cross-border investors, the picture is more complex still. Two inflation environments, two rate-setting institutions, and one exchange rate connecting them creates an additional variable that requires active monitoring — not just as part of your investment strategy, but as part of your cash flow and currency planning.

Whether through diversification, sector rotation, inflation-resistant assets, or currency positioning, staying ahead of inflation requires understanding how it actually moves through markets. If you would like to discuss how inflation affects your specific cross-border situation, book a complimentary consultation with our team.

Frequently Asked Questions

Why is high inflation bad for the stock market?

High inflation hurts stocks through three main channels. Input costs rise faster than companies can raise prices, compressing profit margins. Central banks respond by raising interest rates, which increases borrowing costs and reduces the present value of future earnings. Consumer spending also shifts as goods become more expensive, reducing sales volumes even when prices are nominally higher.

Do higher prices mean higher company revenues during inflation?

Not necessarily. While companies can charge more per unit, consumer behaviour shifts in inflationary environments. Spending becomes more selective, brand loyalty erodes as consumers prioritise price, and unit volumes can fall even if prices rise. Total revenue may flatten or decline even when prices are up.

What is shrinkflation?

Shrinkflation is when companies reduce the size or quantity of a product without lowering its price, rather than raising the sticker price directly. It preserves short-term sales volumes by avoiding visible price increases, but typically damages long-term brand equity as consumers notice the reduction.

How do interest rates connect to inflation and stock valuations?

When inflation rises, central banks typically raise short-term interest rates to slow economic activity and reduce the money supply. Higher rates increase borrowing costs for businesses and consumers. They also reduce the present value of future corporate earnings in discounted cash flow models, which is why growth stocks tend to underperform most during high inflation — their value depends heavily on future earnings, which are worth less when discount rates rise.

What is the Federal Reserve’s inflation target?

The Federal Open Market Committee targets an inflation rate of approximately 2%. This level is considered consistent with stable prices and healthy long-term economic growth. When inflation rises above this target, the Fed typically raises short-term interest rates to reduce liquidity, slow borrowing, and cool economic activity.

What is disinflation and why is it generally good for stocks?

Disinflation is a slowdown in the rate of inflation — prices are still rising, but more slowly. As cost pressures ease, companies can plan more effectively and profit margins tend to recover. Consumer confidence typically improves as well. Investors usually reward this environment with higher valuations, particularly in cyclical and growth sectors.

What is deflation and why is it considered worse than inflation?

Deflation is a general decrease in prices across the economy. While falling prices may sound appealing, deflation signals weak economic demand and typically triggers a self-reinforcing cycle: consumers delay purchases, businesses cut costs and staff, demand falls further, and prices drop further still. Stock markets generally perform poorly during deflationary periods, especially in sectors tied to consumer spending and real estate.

How does inflation affect cross-border investors with assets in both Canada and the US?

Cross-border investors face compounded inflation exposure. Canadian and US inflation rates can diverge meaningfully, and the resulting shifts in the USD/CAD exchange rate directly affect the real purchasing power of income or assets held in one currency while spending occurs in another. A retiree with Canadian-dollar pension income and US-dollar living expenses can be doubly impacted when inflation rates diverge between the two countries.

How do USD/CAD exchange rate movements relate to inflation?

Exchange rates are influenced by relative inflation and interest rate differentials between countries. When US inflation is higher than Canadian inflation, the Bank of Canada and the Federal Reserve often diverge in their rate responses, which can shift the USD/CAD rate materially. For cross-border retirees drawing income in one currency and spending in another, these movements directly affect purchasing power independent of portfolio returns.

What portfolio strategies help during inflationary periods?

Common inflation-resistant strategies include maintaining diversified equity exposure rather than moving entirely to cash or fixed income, allocating to real assets such as REITs or commodities, holding shorter-duration bonds that are less sensitive to rising rates, and for cross-border investors, reviewing currency exposure to ensure income and expense currencies are reasonably aligned.