Medicaid’s 80-Hour Work Rule: What Cross-Border Families Need to Know

DISCLAIMER: This article is |

When Canadians move to the United States, they bring one assumption that can cost them dearly: that healthcare will be sorted out the way it always was — automatically, universally, just by being there. Canada’s provincial health systems have that effect. After a lifetime of OHIP, MSP, or RAMQ, the idea that you could move countries and end up uninsured does not feel real.

It is real. And a major US policy change makes the planning even more urgent.

Under the 2025 federal budget reconciliation law — the One Big Beautiful Bill — many adult Medicaid enrollees will be required to prove at least 80 hours per month of community engagement, including paid work, to keep their coverage. For cross-border families navigating the move from Canada to the US, this change is one piece of a larger picture that deserves careful planning before the move — not after.

The Healthcare Assumption Canadians Make When Moving to the US

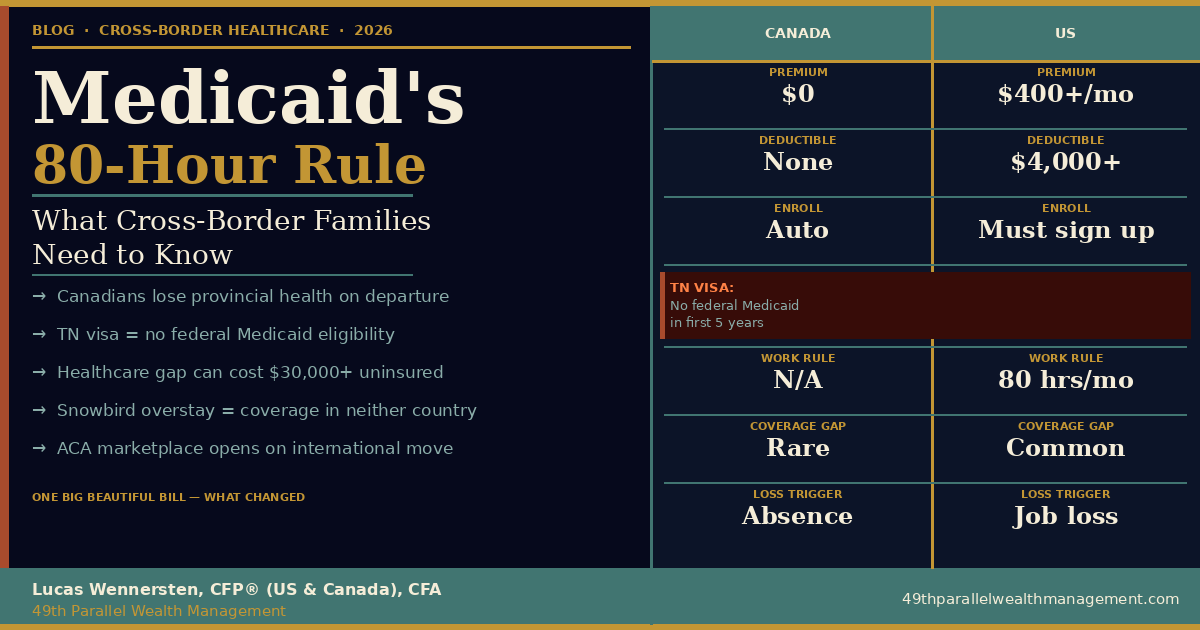

In Canada, healthcare coverage follows you. As long as you are a provincial resident, you are covered. The system is funded by taxes, not by employment status. You do not need to find a plan, pay a premium, or choose a deductible tier.

The US system works entirely differently. Coverage is tied to employment, income level, age, or individual purchase. If you move to the US and your employer does not offer health benefits — or if you are self-employed, on a work visa in a lower-wage role, or transitioning between jobs — you can find yourself completely without coverage.

The gap: Most provinces end your health coverage after a defined period of absence — typically 6 to 7 months. Ontario (OHIP), for example, covers you for up to 212 days outside Ontario per year. British Columbia (MSP) has a 7-month rule. If you permanently relocate to the US, your provincial coverage ends. The US side of that gap is not filled automatically. You must find and enroll in coverage — or face the full cost of US healthcare without insurance. |

What the Medicaid 80-Hour Work Requirement Actually Is

Medicaid is the US federal-state program that provides health coverage for low-income individuals and families. In states that expanded Medicaid under the ACA marketplace coverage, adults earning up to 138% of the federal poverty level ($20,783 for a single adult in 2025) are eligible.

The new rule, as detailed in the CMS community engagement guidance, requires adult enrollees ages 19–64 in the ACA expansion group to demonstrate at least 80 hours per month of qualifying activity to maintain coverage. That activity can include:

- Paid employment of at least 80 hours

- Community service totalling at least 80 hours

- Qualifying work program participation

- Half-time enrollment in an educational or career/technical program

- Earning income equivalent to the federal minimum wage multiplied by 80 hours ($580/month at $7.25/hour)

States must implement by January 1, 2027, though they may start earlier. The requirement cannot be waived under Section 1115.

Why This Matters for Canadians Moving to the US

Most Canadians who move to the US do not end up on Medicaid. Their income is too high, their employment too stable, or their immigration status excludes them. But the cross-border healthcare planning issue is much broader than Medicaid eligibility alone. The new rule is a useful frame for understanding the full picture.

Who This Directly Affects

Canadians who fall into the Medicaid eligibility window in an expansion state:

- Early-career professionals on TN or H-1B visas earning lower wages in their first US role

- Canadians who move to the US for a spouse’s employment and are not yet working themselves

- Self-employed Canadians in the US who have not yet built consistent income

- Canadians who retire early, relocate to the US, and have limited income before Social Security or pension income begins

Immigration note: TN visa holders and most non-immigrant visa holders are generally ineligible for federally funded Medicaid during the first five years of US residency under the 1996 federal welfare law. Some states use state funds to cover certain non-immigrants. If you are on a TN or H-1B visa, do not assume Medicaid is an option — plan for private coverage from day one. |

Who This Indirectly Affects — The Coverage Gap Problem

The deeper cross-border healthcare issue is not Medicaid specifically — it is the gap between leaving Canadian provincial coverage and establishing solid US coverage. That gap catches people off guard far more often than Medicaid’s work requirement will.

A single US hospital visit without insurance can cost $15,000 to $50,000 or more. A cross-border family going through a relocation year — selling a Canadian home, landing in the US, getting the children settled, finding employers — is often in a transition state where nobody has confirmed healthcare coverage. That is a significant financial exposure that belongs in your cross-border financial planning from the outset.

Canada vs US Healthcare: What Changes When You Move

Feature | Canada (Provincial) | US (Employer / ACA / Medicaid) |

Coverage trigger | Provincial residency | Employment, income, age, or purchase |

Premium cost | $0 in most provinces | $200–$600+/month individual (ACA) |

Deductible | None | $1,500–$8,000+ per year |

Doctor visit | Covered | Copay + deductible applies |

Loss of coverage | When you leave province | When you lose job or stop paying |

Uninsured risk | Not applicable | Full cost of care — can be catastrophic |

Transition period | 6–7 months depending on province | Immediate — coverage ends with status |

The Snowbird Healthcare Trap

Snowbirds face a compounding risk. Spending too long in the US — enough to trigger the IRS substantial presence test — can make you a US tax resident. That same extended presence often violates your province’s residency requirements, ending your provincial health coverage.

The result: you may lose both your Canadian provincial coverage and face US tax obligations — without qualifying for the US healthcare benefits that come with US residency, particularly Medicare, which requires 40 quarters of US work history.

This is exactly the kind of interlocking planning problem that a complete Canada-US tax strategy and healthcare review is designed to identify before it becomes a crisis. Many snowbirds discover it only after the fact.

What Cross-Border Families Should Do

- Confirm your provincial coverage end date before you leave. Contact your provincial health authority and get a written confirmation of when your coverage lapses based on your departure date. Do not guess.

- Enroll in US coverage before your Canadian coverage ends. If your employer offers health benefits, enroll on day one. If not, shop the ACA marketplace at healthcare.gov. A qualifying life event — relocating from another country — opens a special enrollment period outside the standard November-January open enrollment window.

- Budget for deductibles and copays. Even with good US coverage, out-of-pocket costs are a real expense. A family plan with a $4,000 deductible means the first $4,000 of medical expenses each year comes out of pocket. This does not exist in the Canadian system and frequently surprises new arrivals.

- Understand Medicaid eligibility if income is low. If your income in the first year in the US is below 138% of the federal poverty level and you are in a Medicaid expansion state, you may qualify. Understand the work requirement timeline and documentation process so you are not caught by the 2027 implementation.

- Build healthcare cost projections into your cross-border plan. Healthcare is consistently the largest unplanned expense for Canadians who relocate to the US. A real cross-border financial planning engagement accounts for coverage timelines, premium budgets, long-term care exposure, and the path to Medicare eligibility.

- Review your situation if you are already in the US. If you moved to the US in the last few years and have not explicitly reviewed your healthcare coverage and its interaction with your tax residency and Canadian pension benefits, now is the right time. Our common cross-border questions page is a useful starting point.

Frequently Asked Questions

Do Canadians moving to the US qualify for Medicaid?

Canadians who become US tax residents may qualify for Medicaid if their income falls below 138% of the federal poverty level and they are in an ACA expansion state. Eligibility depends on immigration status — TN and H-1B visa holders are generally excluded from federally funded Medicaid for the first five years.

What is the new Medicaid 80-hour work requirement?

Starting by January 1, 2027, many adult Medicaid enrollees ages 19–64 in the ACA expansion group must demonstrate at least 80 hours per month of community engagement — paid work, community service, qualifying education, or a combination — to maintain coverage.

When does Canada stop covering you when you move to the US?

This varies by province. Most provinces end coverage after 6 to 7 months of absence. OHIP covers you for up to 212 days outside Ontario per year. British Columbia’s MSP has a 7-month rule. Permanently relocating to the US ends provincial coverage after the applicable transition period.

What healthcare options exist for Canadians in the US without employer insurance?

Canadians moving to the US can purchase coverage through the ACA marketplace at healthcare.gov. Relocating from another country qualifies as a special enrollment event. Depending on income, premium tax credits may apply. Those 65+ with 40 quarters of US work history may qualify for Medicare.

Does the Medicaid 80-hour rule apply to TN visa holders?

Most TN visa holders are not eligible for federally funded Medicaid during the first five years of US residency. Some states cover certain non-immigrants using state funds. TN visa holders should obtain private or employer-sponsored coverage and not rely on Medicaid as a safety net.

What is the healthcare gap risk for Canadians moving to the US?

The healthcare gap is the period between losing provincial coverage in Canada and obtaining qualifying US coverage. A single uninsured hospital visit in the US can cost $15,000 to $50,000 or more. Planning coverage transition in advance of the move is essential.

Can snowbirds lose provincial health coverage?

Yes. Snowbirds who exceed their province’s maximum out-of-province days risk losing provincial coverage. If they also meet the IRS substantial presence test, they may become US tax residents — creating obligations in both countries while potentially qualifying for coverage in neither.

What should cross-border families do to plan for US healthcare costs?

Confirm provincial coverage end dates before departing, enroll in US coverage immediately upon arrival, budget for deductibles and copays that do not exist in the Canadian system, and include healthcare cost projections in your cross-border financial plan.

Does losing Medicaid affect cross-border tax filing?

Losing Medicaid itself does not create a direct tax liability, but healthcare costs that become out-of-pocket may affect the medical expense deduction on both US and Canadian returns depending on residency status. Gaps in US insurance coverage interact with ACA reporting requirements on Form 1040.

Is US healthcare planning part of cross-border financial planning?

Yes — and it is one of the most overlooked components. Healthcare is often the largest unplanned expense for Canadians who relocate to the US. A complete cross-border plan accounts for coverage transition, premium costs, deductible exposure, long-term care, and the path to Medicare eligibility.

At 49th Parallel Wealth Management

Healthcare is where the Canada-to-US move most often goes wrong financially. Coming from a universal system, Canadians consistently underestimate the cost, complexity, and planning lead time required to establish solid US coverage. It is not a detail to sort out after you arrive — it is a core part of retiring across the border or making any permanent move work.

At 49th Parallel Wealth Management, we hold dual licensing in both Canada and the US and work exclusively with cross-border families who need both sides of the picture. We build healthcare cost projections, coverage timelines, and long-term care exposure into every cross-border financial planning engagement.

From the Desert to the Tundra™ — book a complimentary consultation and let’s make sure the healthcare gap is not part of your story.

From the Desert to the Tundra™