Moody’s US Downgrade: What It Means for Cross-Border Investors

Lucas Wennersten, CFP® (US & Canada), CFA · 49th Parallel Wealth Management · ~11 min read |

IMPORTANT DISCLAIMER This article is for educational purposes only and does not constitute tax, legal, or investment advice. Cross-border financial situations are highly fact-specific. Always consult a qualified cross-border financial advisor and tax professional before making decisions based on market events. |

On May 16, 2025, Moody’s Investors Service lowered the United States’ long-term credit rating from Aaa to Aa1 — making it the first time all three major agencies (Moody’s, S&P, and Fitch) have rated US sovereign debt below the highest investment grade. The move cited persistent fiscal deficits, rising interest servicing costs that now exceed defense spending, and the absence of meaningful bipartisan fiscal reform.

Most commentary on the downgrade has focused on US domestic investors: what happens to Treasuries, whether yields rise, whether the stock market reacts. That coverage is useful but incomplete for anyone with financial accounts, property, pension assets, or family on both sides of the Canada-US border. The cross-border picture is materially different — and in some ways more nuanced than either country’s domestic narrative.

What Moody’s Actually Said — and What It Didn’t

The downgrade reflects three structural concerns Moody’s has flagged over many years, not a sudden crisis event. The US national debt now exceeds $36 trillion, and annual interest payments have surpassed defense spending for the first time. Moody’s specifically noted the lack of political consensus around fiscal consolidation — neither party has produced a credible medium-term plan to stabilise the debt-to-GDP ratio.

What the downgrade does not mean: that the US is at risk of default, that Treasuries are unsafe, or that a recession is imminent. The April 2025 federal budget showed a $258 billion monthly surplus driven by strong tax receipts — a useful reminder that a single data point rarely tells the full story. The year-to-date deficit still exceeded $1 trillion at the time of the downgrade. Both facts are true simultaneously, and both matter.

HISTORICAL CONTEXT: THE 2011 S&P DOWNGRADE S&P downgraded the US from AAA to AA+ in August 2011 — the last comparable event. Markets initially sold off, then recovered. Over the 12 months following the downgrade: • The S&P 500 returned approximately +15% • 10-year Treasury yields fell, not rose, as investors sought safety • The USD weakened modestly against the CAD before recovering The Moody’s downgrade is not necessarily a market inflection point. It is a fiscal accountability signal — and one that has specific implications for cross-border families. |

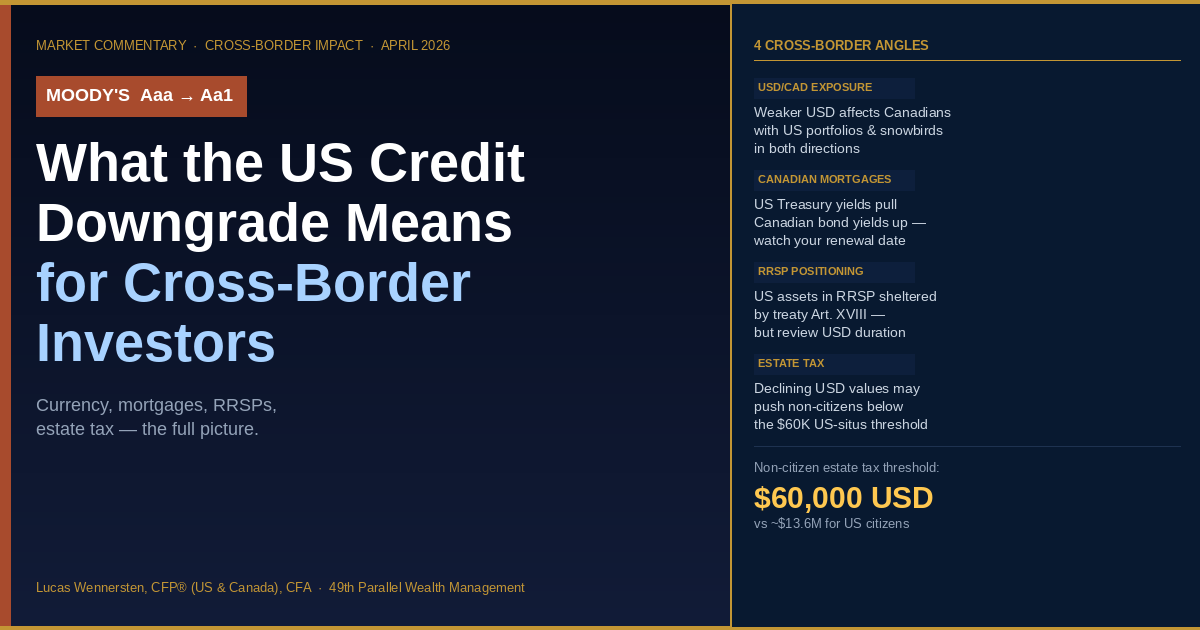

USD/CAD: The Currency Angle Every Cross-Border Family Feels Directly

For cross-border families, a US sovereign credit event is first and foremost a currency story. When confidence in US fiscal management weakens, the USD tends to soften against major currencies including the CAD. The CAD is a commodity currency that often strengthens when USD confidence dips and global commodity prices hold firm.

This creates a set of divergent outcomes depending on which direction you are facing across the border:

Your situation | If USD weakens vs CAD | If USD strengthens vs CAD |

Canadian in the US, USD income | US income buys less CAD for Canadian family/expenses/property | US income converts to more CAD — buying power for Canadian obligations improves |

Canadian with USD investment portfolio | Portfolio value in CAD terms declines even if USD returns are flat | CAD-equivalent portfolio value rises — a tailwind on top of investment returns |

Snowbird spending winters in the US on Canadian dollars | US spending becomes cheaper in CAD terms — Arizona, Florida, Hawaii cost less | US spending costs more CAD — budget planning for the US winter matters more |

American in Canada, planning Canada retirement | USD-denominated savings buy less CAD retirement purchasing power | USD savings stretch further for Canadian retirement expenses |

The Bank of Canada publishes daily exchange rates at bankofcanada.ca/rates/exchange. For cross-border families with significant currency exposure in either direction, the Moody’s downgrade is a reasonable prompt to review whether your currency positioning — where you hold cash, near-cash, and fixed income — still matches your actual spending obligations. This is a core part of cross-border financial planning that domestic advisors on either side rarely address.

US Treasury Yields and Canadian Mortgage Rates: A Linked Market

One of the less-discussed cross-border implications of the Moody’s downgrade is its potential effect on Canadian fixed income and mortgage rates. Canadian and US bond markets are tightly correlated — not identical, but meaningfully linked. When US Treasury yields rise in response to fiscal concerns or reduced demand for US sovereign debt, Canadian Government Bond (CGB) yields often follow, with some lag and divergence based on Bank of Canada policy.

Canadian fixed-rate mortgage rates are priced off CGB yields. If a sustained rise in US yields pulls Canadian yields higher, Canadians renewing fixed-rate mortgages face higher rates than they might have expected — a direct pocket-book consequence of US fiscal credibility concerns. For cross-border clients who still own Canadian property while living in the US (or vice versa), this linkage matters at renewal time.

WHAT TO WATCH If you have a Canadian mortgage renewing in the next 12–24 months, track the 5-year CGB yield alongside the US 10-year Treasury. A sustained rise in US yields that pulls Canadian yields up meaningfully may argue for locking in a fixed rate earlier rather than waiting at renewal. This is not investment advice — it is a planning variable worth discussing with your mortgage broker and cross-border advisor together. |

RRSP Exposure to US Assets: What the Downgrade Means for Registered Accounts

Many cross-border Canadians — particularly those who have worked in both countries — hold US equities and US bonds inside their RRSPs. The RRSP’s foreign content rules were removed in 2005, so there is no restriction on holding US assets in a registered account. However, the cross-border tax treatment of US-source income inside an RRSP is governed by the Canada-US Tax Treaty, specifically Article XVIII.

Under Article XVIII, the US generally exempts RRSP income from US withholding tax for Canadian residents — meaning US dividends and interest inside an RRSP are typically sheltered from the 15% or 30% US non-resident withholding tax that would otherwise apply. This treaty benefit is worth preserving. It means holding US equities inside an RRSP (rather than in a taxable Canadian account) is often the most efficient structure for cross-border clients with RRSP room.

As US fiscal concerns put pressure on USD-denominated bonds, RRSP holders with heavy US fixed income exposure may want to review their duration and currency positioning. This is not a call to reduce US equities — long-term equity returns are not driven by credit rating events. But US fixed income inside an RRSP warrants a conversation about whether the yield is adequate compensation for the currency and duration risk. The Canada-US Tax Treaty text is available at canada.ca/us-tax-treaty, and our team covers this as part of cross-border retirement planning reviews.

The Estate Tax Silver Lining: Declining USD Values and the $60,000 Threshold

This is the counterintuitive cross-border angle that almost nobody covers. Non-US citizens who hold US-situs assets — US equities, US real estate, US-listed ETFs in a US brokerage account — face US estate tax on those assets above a threshold of just $60,000 USD. The threshold for US citizens is roughly $13.6 million. The gap is enormous, and it catches many cross-border clients off guard.

Here is the silver lining: the $60,000 threshold is a fixed USD amount. If the USD weakens against the CAD — as it has tended to do during periods of US fiscal stress — the CAD-equivalent value of a cross-border client’s US-situs holdings may fall below the threshold that would otherwise trigger US estate tax exposure. A Canadian resident whose US brokerage account was worth $80,000 USD at year-end 2024 might find it worth only $68,000 USD after a USD correction, reducing or eliminating the estate tax exposure.

IMPORTANT CAVEAT ON ESTATE TAX PLANNING Relying on USD weakness to manage estate tax exposure is not a strategy — it is a coincidence. The right approach is deliberate account structuring: holding Canadian-listed equivalents of US assets in Canadian brokerage accounts eliminates the US-situs concern entirely, regardless of exchange rates. Our cross-border estate planning work addresses this directly. |

Cross-Border Portfolio Positioning: What to Actually Review

The Moody’s downgrade does not require a portfolio overhaul. Reacting to rating events by selling equities or shifting to cash has historically been one of the more reliably poor investment decisions. What it does warrant is a structured review of whether your cross-border portfolio is positioned correctly for the environment it is already in — regardless of the downgrade. Here are the four areas worth checking:

- Currency reserves and cash positioning: If you have near-term obligations in both currencies — a Canadian mortgage renewal, a US tax installment, a cross-border property purchase — holding adequate reserves in the right currency reduces your exposure to adverse exchange rate moves at the worst time.

- US fixed income duration: Long-duration US bonds are most sensitive to yield increases. If your RRSP or taxable account holds US bond ETFs with long duration, a sustained rise in US yields could produce meaningful capital losses even before currency effects. Shorter duration reduces this sensitivity.

- RRSP and 401(k) asset location: The treaty treatment of US-source income differs between account types. US equities belong in the RRSP (treaty shelters US withholding). Canadian equities belong in taxable accounts where the dividend tax credit applies. Getting asset location right is more impactful than reacting to rating events.

- US-situs exposure review: If your total US-situs assets (US brokerage account, US real estate, US-listed ETFs) are close to or above $60,000 USD, a dedicated estate planning review is overdue regardless of the downgrade.

None of these reviews require a market view on what the downgrade means for the S&P 500. They are structural planning questions that the downgrade simply makes timely. Our cross-border wealth management and cross-border investment management work covers each of these areas in a structured way.

Frequently Asked Questions

1. Will Moody’s downgrade cause US Treasuries to lose value?

Not necessarily, and history suggests the opposite is more common. After the S&P downgrade in 2011, US Treasury yields actually fell as investors sought safety — counterintuitively, the downgrade drove money into Treasuries rather than out of them. The Moody’s downgrade is primarily a fiscal credibility signal. Whether it causes yields to rise depends on many factors including Federal Reserve policy, global risk appetite, and whether the downgrade triggers forced selling by institutional investors whose mandates require Aaa/AAA holdings — which is a relatively narrow group for the Aa1 rating.

2. As a Canadian resident, should I reduce my US equity exposure after the downgrade?

The downgrade does not provide a reliable signal for reducing US equity exposure. Long-term equity returns are driven by corporate earnings, economic growth, and valuation — not sovereign credit ratings. The more relevant question for a Canadian resident is whether your US equity exposure is held in the right account type (RRSP for treaty benefits) and whether your currency hedging or unhedged position matches your actual spending obligations. Those are planning decisions, not market timing decisions.

3. How does the Moody’s downgrade affect the Canadian dollar?

In the short term, a US sovereign credit concern can weaken the USD against the CAD, since the CAD is generally viewed as a fiscally stronger currency relative to the US on a debt-to-GDP basis. However, the CAD is also a commodity currency that is heavily influenced by oil prices, global risk sentiment, and the Bank of Canada’s rate decisions. Over any multi-week or multi-month horizon, those factors typically dominate any single credit rating event. Currency moves are difficult to predict, which is exactly why cross-border financial planning focuses on structural positioning rather than currency forecasts.

4. Does the downgrade affect my RRSP if it holds US assets?

Not directly. The RRSP is a Canadian registered account, and its tax treatment in Canada is unaffected by US credit ratings. The Canada-US Tax Treaty protections for US-source income inside an RRSP (Article XVIII) also remain in force. What may be affected indirectly is the value of USD-denominated holdings inside your RRSP if the USD weakens — which would reduce the CAD-equivalent value of US assets in your account. This is a normal currency exposure that exists regardless of the downgrade.

5. Should Canadians with US mortgages or property be concerned?

Canadians with US property financed by a US mortgage are exposed to two effects from a downgrade event: potential USD weakness (which reduces the CAD cost of their US mortgage obligation — a benefit) and potential US yield rises (which could increase refinancing costs if their mortgage is variable or coming up for renewal). On balance, a moderately weaker USD is generally a mild tailwind for Canadians holding US-denominated liabilities while earning CAD. The concern is more acute if rising yields push US mortgage rates higher at renewal.

6. I am a snowbird. How does the downgrade affect my US spending budget?

If the USD weakens relative to the CAD following the downgrade, your Canadian dollars buy more USD — your Arizona, Florida, or Hawaii spending budget goes further. This has been one of the recurring pleasant surprises for snowbirds during USD softness periods. The reverse is also true: a stronger USD makes US spending more expensive in CAD terms. For snowbirds with multi-year spending plans, building in a currency buffer (holding some USD cash reserves from Canadian-dollar conversions when the rate is favourable) is a simple planning tool.

7. Does the downgrade affect the Canada-US Tax Treaty?

No. Credit rating events have no bearing on bilateral tax treaties. The Canada-US Tax Treaty of 1980 (and its subsequent protocols) remains fully in force and is not affected by Moody’s rating actions. Treaty provisions governing RRSP treatment, withholding tax rates on dividends and interest, capital gains allocation, and the mutual agreement procedure are all unaffected.

8. As a US person in Canada, should I move money out of USD assets?

This depends on your financial plan, not on the downgrade. If you have long-term financial goals denominated in CAD — retiring in Canada, funding Canadian education costs, maintaining a Canadian primary residence — then holding significant USD-denominated assets creates a structural currency mismatch that exists regardless of the downgrade. A credit event may accelerate the conversation, but the underlying planning question is whether your asset currencies match your liability currencies over your planning horizon.

9. Could the downgrade affect CPP, OAS, or Social Security payments?

No. Canadian pension payments (CPP and OAS) are funded through Canadian government revenues and the CPP Investment Board — entirely separate from US fiscal matters. US Social Security is funded through the US payroll tax system (FICA). Neither program’s payment reliability is affected by a Moody’s rating action. For cross-border clients receiving both CPP/OAS and Social Security, the relevant planning consideration is currency — which currency you receive each payment in, and how that maps to your spending obligations.

10. What should I actually do right now?

For most cross-border investors, the right action after a credit rating event is to do nothing with your portfolio and do something with your plan. Specifically: review whether your currency reserves match near-term obligations in both currencies, confirm your RRSP and taxable account asset location is optimal under the treaty, check whether any US-situs assets are above the $60,000 estate tax threshold, and verify your mortgage renewal timeline on any Canadian property. If you have not had a structured cross-border financial review recently, this is a reasonable prompt to schedule one.

IS YOUR CROSS-BORDER PORTFOLIO POSITIONED FOR THIS ENVIRONMENT? Market events create planning moments. The Moody’s downgrade raises real questions about currency exposure, Canadian mortgage linkages, RRSP positioning, and estate tax thresholds that domestic advisors on either side of the border rarely address together. Lucas Wennersten holds dual CFP® designations in both Canada and the US, plus the CFA credential. 49th Parallel Wealth Management works exclusively with cross-border clients. Book a complimentary consultation — or explore our cross-border financial planning and cross-border retirement planning services. |