Private Equity in Your 401(k): What the New Rules Mean for Investors

DISCLAIMER This article is for informational and educational purposes only. It does not constitute financial, investment, tax, or legal advice. Return estimates cited are from third-party sources and are not guarantees of future performance. Private equity involves significant risk including illiquidity and potential loss of principal. Consult a qualified fiduciary advisor before making any investment decisions. 49th Parallel Wealth Management is registered as an investment adviser in the United States. |

By Lucas Wennersten, CFP® (US & Canada), CFA · 49th Parallel Wealth Management

Reading time: ~7 minutes · Updated: April 26, 2026

For decades, 401(k) plans have followed a predictable script: a short list of mutual funds, often dominated by target-date funds or a single fund family. While simple, this model has limited investors’ ability to diversify across asset classes — particularly when it comes to alternatives like private equity, private debt, market-neutral strategies, or real assets.

That is now changing. A 2025 executive order directed the Department of Labor to expand the permissible investment options in employer-sponsored retirement plans to include private equity and other alternative investments. The rollout is still in early stages and adoption will vary by plan sponsor, but the regulatory door has been opened in a meaningful way.

This article breaks down what private equity actually is, how it has historically performed relative to public equities, the real risks and fees investors need to understand, and — critically — what this means for cross-border investors who hold both US and Canadian retirement accounts.

Why This Matters: The Limitations of Today’s 401(k)

Most 401(k) participants have access to a narrow menu of investment options. The current reality for many plans includes:

- Limited diversification — most plans restrict access to a handful of mutual funds or ETFs within a few asset classes

- One-size-fits-all portfolios — target-date funds often fail to reflect personal risk tolerance, tax situation, or financial goals

- Missed opportunities — investors are unable to access alternative assets that institutional investors and endowments have used for decades to manage risk and enhance returns

Expanding the investment menu addresses all three. More choice does not mean every option is right for every investor — but it allows advisors and informed participants to construct retirement strategies tailored to individual circumstances rather than lowest-common-denominator defaults.

The Private Equity Landscape

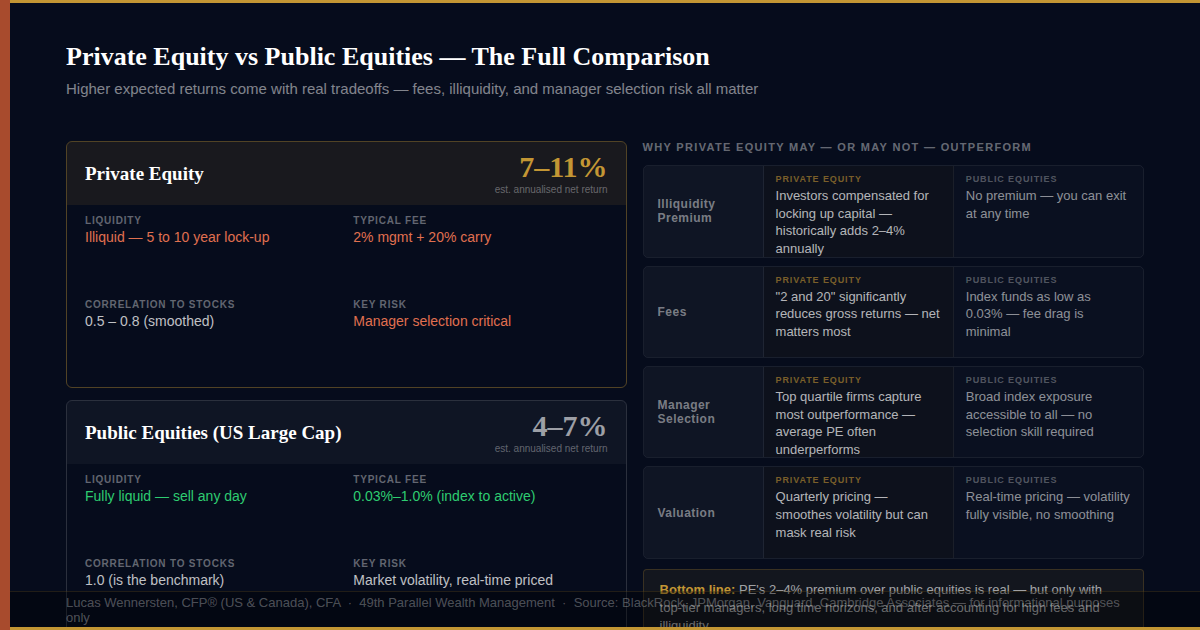

Private equity involves investing in companies that are not listed on public stock exchanges. Unlike publicly traded stocks, private equity investments are illiquid — you cannot sell your position when you choose. Private equity firms typically acquire, improve, and eventually sell companies over a 5 to 10 year investment cycle.

A few statistics that contextualise the opportunity:

- As of recent estimates, only approximately 13% of US companies with over $100 million in annual revenue are publicly traded. The remaining 87% are privately held.

- The number of public companies in the US has declined by nearly 50% over the past 25 years.

- Private companies are staying private longer, often reaching high valuations before considering an IPO.

- Venture capital and private equity firms are extracting more value during the private phase, leaving less upside for public market investors.

In other words, a growing share of corporate value creation is happening in private markets. The 401(k) expansion attempts to give everyday investors access to that growth.

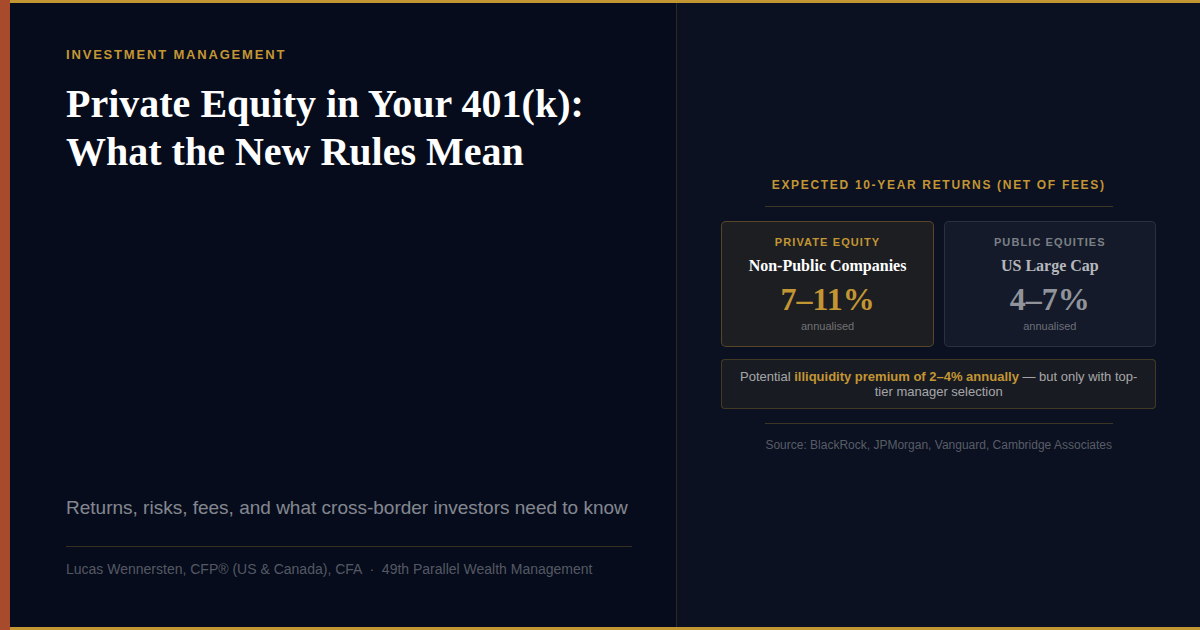

Expected Returns: Private Equity vs Public Equities

Asset Class | Expected 10-Year Return (Net) | Source |

Private Equity | 7% – 11% annualised | BlackRock, JPMorgan, Vanguard, Cambridge Associates |

Public Equities — US Large Cap | 4% – 7% annualised | Morningstar, Vanguard, Research Affiliates |

The potential premium of 2% to 4% annually is meaningful over a 10 to 20 year retirement horizon. But these figures represent top-tier manager performance. The distribution of returns in private equity is far wider than in public markets — average or lower-quartile funds have historically underperformed public equities after fees. Manager selection is not a secondary consideration; it is the primary determinant of whether PE adds value.

Why Private Equity May Outperform

- Illiquidity Premium — Investors are compensated for locking up capital for longer periods, historically generating excess return above public markets.

- Operational Value Creation — PE firms often improve profitability through hands-on management, cost restructuring, and strategic repositioning.

- Leverage — Strategic use of debt can enhance equity returns, though it also amplifies risk in downturns.

- Access to Growth — Private firms can scale dramatically before going public, capturing value that never reaches public market investors.

The Risks: What Investors Must Understand

- Selection bias — Top-quartile PE firms deliver most of the outperformance. Average or lower-tier funds often underperform public equities after fees.

- Fees — PE carries high costs, commonly structured as “2 and 20”: a 2% annual management fee on committed capital plus 20% carried interest on profits above a hurdle rate. These fees significantly reduce net investor returns relative to gross performance.

- Illiquidity risk — You cannot redeem private equity on short notice. Capital is typically locked up for 5 to 10 years. This is incompatible with short time horizons or investors who may need to access funds before traditional retirement age.

- Valuation smoothing — PE returns are reported quarterly rather than daily. This makes performance appear less volatile than it truly is and can understate the real correlation with public market downturns.

CORRELATION NOTE Private equity has a correlation of approximately 0.5 to 0.8 with public equities, depending on strategy and measurement period: • Buyout funds: higher correlation — typically 0.6 to 0.8 • Venture capital and growth equity: lower correlation — typically 0.3 to 0.6 The apparent smoothness of PE returns is partly an artifact of quarterly pricing. True economic exposure is often more correlated with public markets than the reported data suggests. |

|

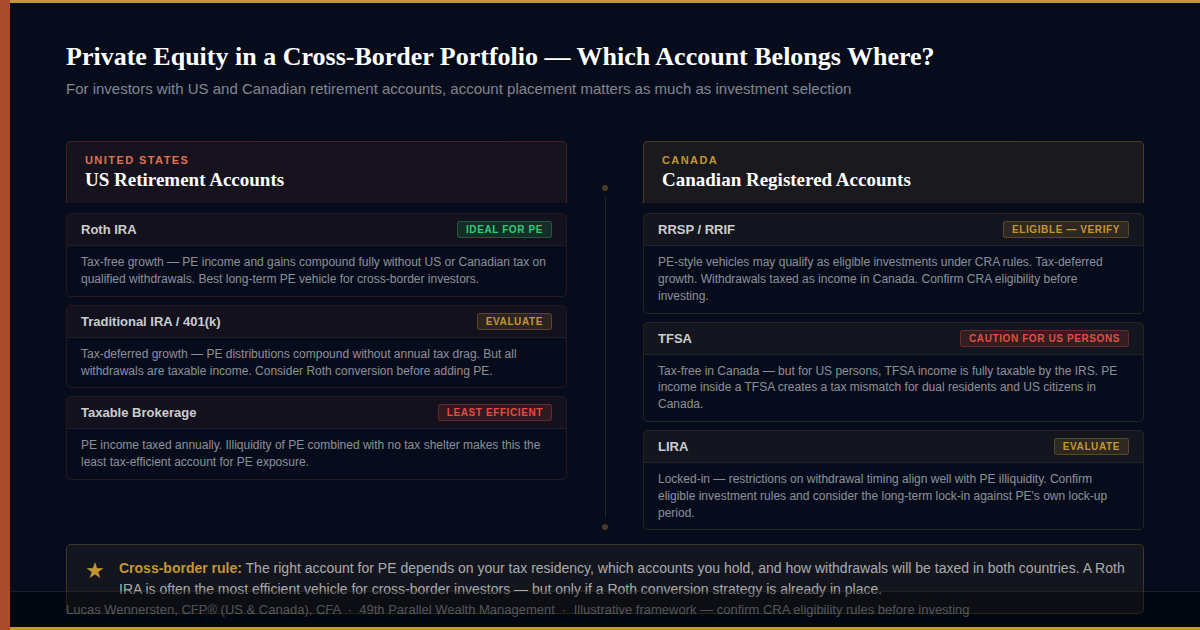

What Cross-Border Investors Need to Know

Canadian investors do not have 401(k) accounts, but the private equity conversation is still relevant — just different.

In Canada, private equity-style exposure is available through alternative mutual funds and limited partnership structures that qualify as eligible investments under CRA rules for RRSPs, TFSAs, and LIRAs. Availability varies by account type and custodian, and not all PE-style vehicles qualify for registered account inclusion. Confirming eligibility before investing is essential — an ineligible investment inside a registered account can trigger significant tax consequences.

For cross-border investors holding both US and Canadian retirement accounts, the allocation question becomes more complex. The account type matters as much as the investment itself. Private equity distributions that generate ordinary income behave differently inside a Roth IRA versus a TFSA — the Roth protects that income from US tax, while the TFSA protects it from Canadian tax but not from US tax for US persons. Putting the right investment in the right account across both systems can meaningfully affect after-tax returns over a decade-long PE holding period.

If you hold retirement accounts in both countries, PE allocation decisions should not be made in isolation. The cross-border account placement question deserves the same attention as the investment selection itself. See our cross-border financial planning and investment management pages for more detail on how we approach this.

|

Don’t Go It Alone

With greater investment choice comes greater responsibility. Alternative investments carry different risks and liquidity constraints than traditional stocks and bonds. That is why it is essential to work with a fiduciary advisor who can help you determine what — if any — role these investments should play in your overall retirement plan.

At 49th Parallel Wealth Management, we offer hourly consulting to help you make informed decisions about your 401(k), whether or not we manage the rest of your portfolio. We also work with Pontera, which enables us to professionally manage your employer-sponsored retirement account on your behalf, even if it remains within your current provider.

Conclusion

If the evolution of the 401(k) system leads to broader access to alternative investments like private equity, it marks a meaningful shift in how Americans prepare for retirement. It will not be right for everyone — the illiquidity, fees, and manager selection risk are real constraints that rule out PE for many participants.

But for investors with long time horizons, appropriate liquidity buffers, and access to quality managers through an advisor, private equity inside a tax-advantaged account could provide the kind of differentiated return source that diversified portfolios have lacked at the retail level.

For cross-border investors specifically, the question is not just whether to invest in PE — it is which account to put it in. Getting that placement decision right across two tax systems is where the real planning value lies.

If you have questions about how private equity fits into your retirement or cross-border plan, book a complimentary consultation with our team.

|

Frequently Asked Questions

Can private equity now be included in a 401(k) plan?

Yes. A 2025 executive order directed the Department of Labor to expand permissible investment options in employer-sponsored retirement plans to include private equity and other alternative investments. The rollout is ongoing and plan adoption varies by employer, but the regulatory framework has been put in place.

What is private equity and how does it differ from public equities?

Private equity involves investing in companies not listed on public stock exchanges. Unlike publicly traded stocks, private equity investments are illiquid — you cannot sell when you choose. Private equity firms typically acquire, improve, and eventually sell companies over a 5 to 10 year period. In exchange for the illiquidity and added complexity, investors have historically received an illiquidity premium above what public markets offer.

What returns can private equity deliver compared to public equities?

Estimates from major asset managers suggest private equity may deliver annualised net returns of 7% to 11% over a 10-year horizon, compared to 4% to 7% for US large-cap public equities. These figures represent top-tier manager performance. Average or lower-quartile private equity funds have historically underperformed public markets after fees, making manager selection critical.

What are the main risks of private equity in a 401(k)?

The primary risks include illiquidity — capital is locked up for 5 to 10 years; high fees — typically a 2% management fee plus 20% carried interest; valuation smoothing — quarterly pricing that can make returns appear less volatile than they are; and selection risk — most outperformance is concentrated in top-quartile managers.

What does “2 and 20” mean in private equity?

“2 and 20” refers to the typical fee structure: a 2% annual management fee on committed capital, plus 20% carried interest on profits above a specified return threshold called the hurdle rate. These fees are substantially higher than traditional mutual funds or index funds and significantly reduce net returns to investors.

How correlated is private equity with public stock markets?

Private equity has a correlation of approximately 0.5 to 0.8 with public equities depending on strategy and measurement period. Buyout funds tend toward 0.6 to 0.8; venture capital and growth equity strategies often show 0.3 to 0.6. The apparent smoothness of PE returns is partly an artifact of quarterly valuation rather than real-time pricing, which understates true economic correlation with public markets.

Can Canadian investors access private equity in their retirement accounts?

Canadian investors do not have 401(k) accounts but can access PE-style exposure through eligible alternative fund structures inside RRSPs, TFSAs, and LIRAs, subject to CRA qualified investment rules. For US persons, TFSA income remains taxable to the IRS, creating a tax mismatch. The Roth IRA is generally the preferred vehicle for cross-border investors seeking PE exposure in a tax-advantaged account.

Should I add private equity to my 401(k)?

Private equity is not appropriate for everyone. Key considerations include your investment time horizon — PE works best with 10 or more years; your liquidity needs — illiquid alternatives are incompatible with early access requirements; your ability to identify top-tier managers through an advisor; and your fee sensitivity relative to low-cost index alternatives. Working with a fiduciary advisor is essential before making any allocation.