Toronto Vacant Home Tax 2025: Rates, Exemptions & Snowbird Rules

Reading time: ~9 minutes · Updated: April 26, 2026

DISCLAIMER This article is for informational and educational purposes only. It does not constitute financial, investment, tax, or legal advice. Toronto Vacant Home Tax rules, rates, deadlines, and exemptions are set by the City of Toronto and subject to change annually. Always confirm current requirements at toronto.ca or with a qualified tax professional before filing. 49th Parallel Wealth Management is registered as an investment adviser in the United States. |

If you own residential property in Toronto and leave it unoccupied for more than six months in a calendar year, the City of Toronto will bill you a Vacant Home Tax (VHT). At the current rate of 3% of assessed value, that bill can reach $24,000 on an $800,000 property, $30,000 on a $1,000,000 property, or $45,000 on a $1,500,000 property. This is not a filing technicality — it is a material financial obligation.

For most Toronto homeowners, the VHT is straightforward: file the annual declaration on time, confirm your property is your principal residence, and move on. But for Canadians who split time between Toronto and the United States — snowbirds, dual residents, and cross-border retirees — the VHT creates a genuine planning conflict. Spending too much time in the US risks triggering the tax. Spending too little can create unintended US tax exposure. Getting this balance right requires understanding both sides of the border simultaneously.

This guide covers the current rate, how the tax is calculated, all available exemptions, declaration deadlines, penalties, and — most importantly — the critical overlap between the VHT’s six-month occupancy rule and the US Substantial Presence Test for cross-border Canadians.

|

What Is the Toronto Vacant Home Tax?

The Toronto Vacant Home Tax is a municipal levy introduced in 2022 under Part XII.1 of the City of Toronto Act. It requires all residential property owners in Toronto to declare their property’s occupancy status annually. Properties deemed or declared vacant for more than six months in the calendar year are subject to the tax.

The official program page is at toronto.ca/vacanthometax. The purpose of the tax is to increase Toronto’s housing supply by incentivising owners to occupy, rent, or sell properties rather than leaving them empty. Revenue collected is directed to the City’s HousingTO affordable housing initiatives.

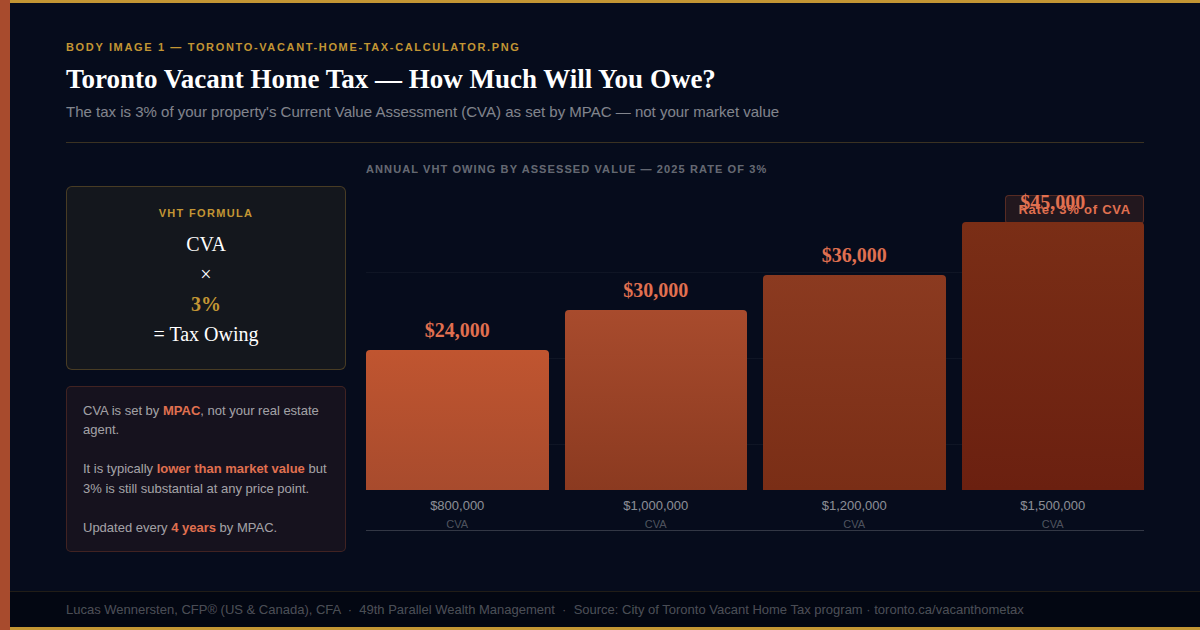

The 2025 Rate and How the Tax Is Calculated

The VHT is calculated as a percentage of the property’s Current Value Assessment (CVA) as determined by the Municipal Property Assessment Corporation (MPAC). The CVA is typically updated every four years and is shown on your annual property tax bill. It is generally lower than current market value.

Assessed Value (CVA) | 2025 VHT Rate | Tax Owing |

$800,000 | 3% | $24,000 |

$1,000,000 | 3% | $30,000 |

$1,200,000 | 3% | $36,000 |

$1,500,000 | 3% | $45,000 |

The rate has been 3% since the 2024 taxation year, up from 1% at the tax’s launch in 2022. City Council confirms the rate annually. There is no sliding scale — the full 3% applies if the property is deemed vacant, regardless of how many months beyond six it was empty.

RATE HISTORY • 2022 and 2023 taxation years: 1% of CVA • 2024 taxation year onward: 3% of CVA — tripled from launch rate |

Declaration Deadline and Process

Every residential property owner in Toronto must file an annual declaration, regardless of occupancy status. Missing the deadline — even if your home was fully occupied — results in the property being automatically deemed vacant and billed the full tax.

Key Date | Detail |

Declaration opens | November 1, 2025 |

Declaration deadline | April 30, 2026 (for 2025 taxation year) |

VHT notices issued | May 2026 (if tax is owed) |

Payment — instalment 1 | September 15, 2026 |

Payment — instalment 2 | October 15, 2026 |

Payment — instalment 3 | November 16, 2026 |

Declarations can be filed online at toronto.ca/vacanthometax using your 21-digit assessment roll number and customer number from your property tax bill. Phone (311 within Toronto, 416-392-2489 outside) and in-person options are also available.

PENALTY SUMMARY • Late filing fee: $21.24 if you miss the deadline but still file • Deemed vacant: property automatically treated as vacant if no declaration filed by deadline — full tax billed regardless of actual occupancy • False declaration: fines up to $10,000 in addition to the tax owed • Overdue tax: interest at 1.25% per month (15% annually) until paid |

Exemptions — Who Qualifies and What Documentation Is Required

A property can be vacant and still exempt from the tax if one of the following criteria is met. You must declare and provide supporting documentation — selecting an exemption without evidence creates audit risk.

Exemption | Qualification | Documentation Required |

Principal Residence | Owner or tenant occupies as principal residence for 6+ months cumulatively | Declaration of occupancy; bills, mail, or driver’s licence at address |

Rental Tenancy | Tenant occupies under 30+ day agreement for 6+ months total | Copy of signed tenancy agreement |

Death of Owner | Owner died during or before the reference year | Death certificate; estate documentation |

Major Renovation | Property undergoing significant renovation preventing occupancy | Building permit; contractor records |

Legal Title Transfer | Property sold with full legal title transfer during the year | Land Transfer Deed |

Employment-Required Absence | Owner/spouse works full-time in Toronto; principal residence is outside GTA | Employer letter confirming full-time employment in Toronto |

Court-Ordered Vacancy | Court order prohibiting occupancy for 6+ months | Copy of court order |

Medical Secondary Residence (2024+) | Owner/spouse/dependent requires secondary residence for medical reasons; principal residence outside GTA | Medical certificate from licensed physician |

New Developer Inventory | Newly constructed unit not yet sold (up to 2 years) | Sales listing or proof of new construction |

|

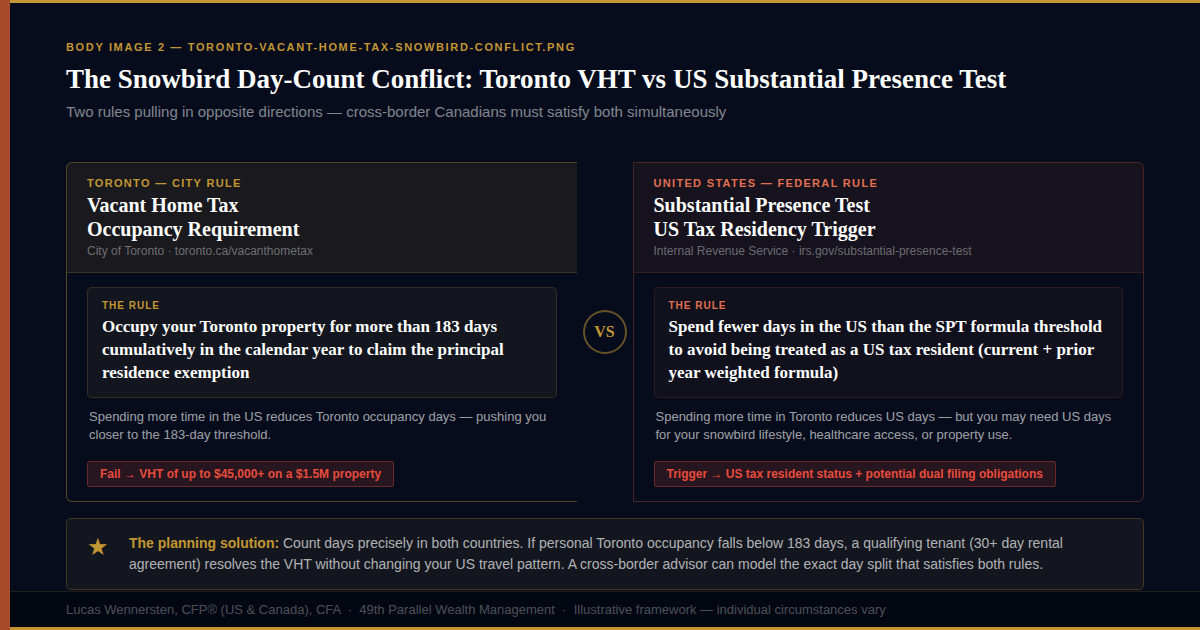

The Snowbird Conflict: VHT Meets the US Substantial Presence Test

This is the section most guides skip — and the most important one for 49th Parallel clients.

Canadian snowbirds who winter in the United States and maintain a Toronto property are caught between two competing day-count rules that pull in opposite directions:

Toronto Vacant Home Tax Rule | US Substantial Presence Test Rule |

Occupy your Toronto property for more than 6 months (183+ days) cumulatively in the calendar year to claim the principal residence exemption and avoid the VHT | Spend fewer than 183 days in the US in the current year (combined with prior-year days under the SPT formula) to avoid being treated as a US tax resident |

The conflict is direct: if you spend more time in Toronto to satisfy the VHT, you reduce your US days. If you spend more time in the US to enjoy your winter property, you risk failing the Toronto occupancy test and triggering the VHT.

There is no single formula that resolves this for every situation — it depends on the specific split of days, whether you own property in both countries, your provincial health coverage requirements, and your full income picture. But the planning principles are consistent:

- Count your days carefully — maintain a day-count log for both countries. The Toronto 183-day test and the US Substantial Presence Test both turn on precise day counts, and informal estimates are not sufficient for either.

- The principal residence rule is cumulative, not consecutive — you do not need to spend six unbroken months in Toronto. Six months accumulated across the year qualifies.

- Provincial health coverage has its own rules — Ontario’s OHIP requires you to be physically present in Ontario for at least 153 days in any 12-month period to maintain coverage. This adds a third layer to the day-count picture.

- Renting is a clean exit — if you cannot satisfy the 183-day personal occupancy requirement, putting a qualifying tenant in your Toronto property under a 30+ day agreement resolves the VHT without requiring you to change your US travel pattern.

For a detailed breakdown of how the US 182-day rule interacts with Canadian residency and provincial health rules, see our cross-border financial planning page. For retirement-specific day-count planning, see our cross-border retirement planning overview.

Action Steps for Toronto Property Owners

- File your declaration by April 30, 2026 — even if your home is fully occupied. Non-declaration is treated as a declaration of vacancy.

- Count your occupancy days — maintain a written log with dates and supporting documents such as bills, mail, and bank statements showing the Toronto address.

- If you are a snowbird — model the day split across both countries. If personal occupancy falls below 183 days in Toronto, evaluate whether qualifying tenancy is a better structure.

- Confirm your CVA — your assessed value is on your property tax bill or MPAC notice. If you believe it is inaccurate, file a Request for Reconsideration with MPAC.

- Gather exemption documentation now — do not wait until filing season. If you are claiming any exemption, locate the supporting documents before the declaration window closes.

- Consult a cross-border advisor if your situation involves both countries — the VHT, US Substantial Presence Test, and provincial health rules interact in ways that a single-country tax professional may not catch.

Conclusion

The Toronto Vacant Home Tax is no longer a niche concern for a handful of property investors. At 3% of assessed value, it is a material financial exposure for any Toronto property owner who does not occupy their home for at least six months per year — whether by choice or circumstance.

For snowbirds and cross-border Canadians, the stakes are higher still. The VHT’s six-month rule sits directly in tension with the US residency day-count rules, and navigating that tension requires coordinated planning across both tax systems simultaneously. A declaration filed without understanding the full cross-border picture can satisfy Toronto’s rules while creating unintended US tax exposure — or vice versa.

The best time to review your day-count structure is before the declaration window closes, not after the bill arrives. If you have questions about how the VHT fits into your broader cross-border picture, book a complimentary consultation with 49th Parallel Wealth Management. From the Desert to the Tundra™, we work across both systems so you do not have to choose between them.

Frequently Asked Questions

What is the Toronto Vacant Home Tax rate in 2025?

The Toronto Vacant Home Tax rate for the 2025 taxation year is 3% of the property’s Current Value Assessment (CVA) as determined by MPAC. This is up from 1% when the tax launched in 2022. For a property assessed at $1,000,000, the tax is $30,000. The rate is set annually by City Council.

What is the declaration deadline for the Toronto Vacant Home Tax?

For the 2025 taxation year, the declaration deadline is April 30, 2026. The declaration period opened November 1, 2025. If you miss the deadline, your property is automatically deemed vacant and you will be billed the tax regardless of actual occupancy, plus a late filing fee of $21.24.

How long does a property need to be vacant to trigger the tax?

A property is considered vacant if it is unoccupied for more than six months (more than 183 days) in the calendar year. The six months do not need to be consecutive — they are counted cumulatively across the year.

What happens if I miss the Toronto Vacant Home Tax declaration deadline?

If you fail to file a declaration by the deadline, the City of Toronto will automatically deem your property vacant and bill you the full Vacant Home Tax for the year, even if your home was occupied. A late filing fee of $21.24 also applies. Making a false declaration can result in fines of up to $10,000 in addition to the tax owed.

Is the Toronto Vacant Home Tax a problem for snowbirds?

Yes — the VHT creates a direct conflict for Canadian snowbirds. The tax requires you to occupy your Toronto property for more than six months per year to claim the principal residence exemption. However, spending too many days in the United States can trigger US tax residency under the Substantial Presence Test. Snowbirds must carefully count their days in both countries and structure their time to satisfy both rules simultaneously.

What exemptions are available for the Toronto Vacant Home Tax?

The City of Toronto recognises several exemptions: principal residence of the owner or a tenant; death of the owner; major renovation; transfer of legal title; employment-required occupancy outside the GTA; court order prohibiting occupancy; medical secondary residence (added 2024); and new developer inventory for up to two years. Each exemption requires supporting documentation filed by the deadline.

How is the Toronto Vacant Home Tax calculated?

The tax equals 3% of the property’s Current Value Assessment (CVA) as set by MPAC. Examples: $800,000 CVA = $24,000 owing; $1,000,000 CVA = $30,000 owing; $1,500,000 CVA = $45,000 owing. The CVA is typically updated every four years by MPAC.

Can I rent out my Toronto property to avoid the Vacant Home Tax?

Yes. If a tenant occupies the property as their principal residence for more than six months in the calendar year under a rental agreement of 30 days or longer, the property qualifies for the principal residence exemption and is not subject to the tax. You must retain the tenancy agreement as documentation.

Does the Toronto Vacant Home Tax apply to all residential properties?

The VHT applies to all residential properties within Toronto’s municipal boundaries. Every homeowner must file an annual declaration regardless of occupancy status. Failure to declare is treated as a declaration of vacancy. Properties outside the City of Toronto’s boundaries are not subject to the VHT, though other Ontario municipalities may have their own programs.

When is the Toronto Vacant Home Tax payable?

For the 2025 taxation year, the tax is payable in three equal instalments: September 15, October 15, and November 16, 2026. Overdue amounts accrue interest at 1.25% per month (15% annually). Outstanding amounts are added to the property tax roll for collection.