What Happens to Your 401k When You Move to Canada

Part of the US Retirement Accounts in Canada series — keep your US retirement savings working across

the border.

If you’re moving to Canada with a 401(k, te most important thing to know is what you don’t have to do: you don’t have to cash it out, and in almost every case you shouldn’t. Your 401k is probably one of the largest assets you own, and the instinct to “clean things up” before a cross-border move is exactly how people hand a quarter of it to the IRS for no reason. The calmer reality is that the Canada-US tax treaty lets the account keep doing its job after you become a Canadian resident. This post is the detailed walk-through; for how the 401k fits with your IRA and Roth, see the full guide to US retirement accounts in Canada.

First: what’s the Canadian equivalent of a 401k?

People searching “401k equivalent in Canada” are usually trying to map a familiar account onto an unfamiliar system. The closest match is the RRSP (Registered Retirement Savings Plan) — a tax-deferred account you contribute to with pre-tax dollars and withdraw from as taxable income in retirement. If your Canadian employer offers a Group RRSP or a defined-contribution pension plan, that’s the nearest analogue to an employer 401k with matching.

The accounts rhyme, but they aren’t identical — contribution limits, employer matching, and withdrawal timing all differ, and importantly, you cannot simply “convert” a 401k into an RRSP without tax consequences (more on that below). For the full side-by-side, see 401k vs RRSP . The key point for now: your existing 401k stays a US account governed by US rules, and Canada’s job is to decide how to tax it for a resident — which the treaty handles cleanly.

The treaty does the work

Under Article XVIII of the Canada-US tax treaty, a 401k is treated as a pension. That single fact drives everything: Canada does not tax the growth accruing inside the account year to year. The tax deferral you built up while living in the US continues uninterrupted after you become a Canadian resident. Canada only taxes the money when it comes out — and even then, with a mechanism to prevent double taxation.

Unlike the Roth IRA, the 401k requires no special election to preserve this treatment — the pension characterization is automatic. (The Roth is the account that needs the one-time filing; if you also hold one, read your Roth IRA after moving to Canada before your first Canadian tax deadline.)

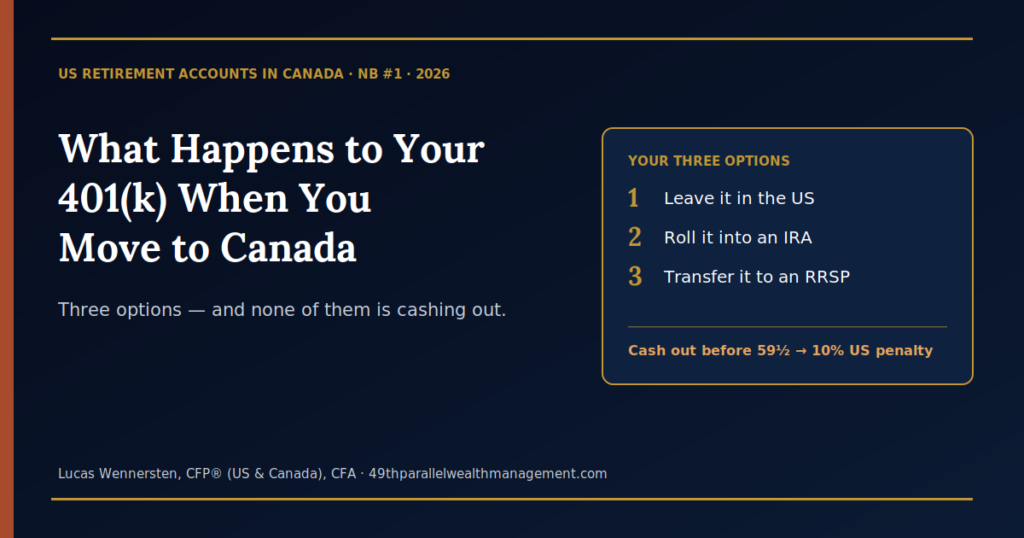

Your three options when you move

You have three real choices for a 401k, and none of them involves cashing out.

Diagram: three paths for a 401k when you move to Canada — leave it in the US, roll it into an IRA, or transfer it into an RRSP — none of which requires cashing out.

Leave it in the US. The simplest path. The account keeps deferring under the treaty, and there’s nothing to file. The main thing to check is your custodian: many US brokerages restrict or freeze accounts once you have a Canadian address, so confirm yours will keep servicing a Canadian-resident account before you move.

Roll it into an IRA. A 401k-to-IRA rollover is not a taxable event in either country, and an IRA usually offers more investment flexibility than an employer plan menu. The treaty deferral carries over unchanged. This is a common housekeeping step done at or before the move — again, with a cross-border-capable custodian.

Transfer it into an RRSP. This is possible, using a special rule (paragraph 60(j) of the Income Tax Act), but it is usually a trap for anyone under 59½: the transfer requires a US withdrawal, which triggers US tax and a 10% early-withdrawal penalty that the Canadian foreign tax credit cannot fully offset. There are narrow situations where it makes sense. The full analysis — including when it’s actually worth doing — is in transferring a 401k or IRA to an RRSP .

How 401k withdrawals are taxed once you’re in Canada

When you eventually draw on the 401k as a Canadian resident, two tax systems touch the same dollars, then reconcile:

- The US taxes first, through withholding. Under the treaty, periodic pension payments are subject to 15% US withholding when you’ve filed a Form W-8BEN claiming treaty benefits. A lump-sum or non-periodic distribution that doesn’t qualify as periodic can face the default 30%

- Canada taxes the withdrawal as income, then credits the US tax. You report the distribution on your Canadian return and claim a foreign tax credit (Form T2209) for the US tax paid. The credit prevents the same dollars from being taxed twice; in practice you pay the higher of the two countries’ effective rates, not the sum.

The net result for most retirees: the 401k is taxed roughly as if it were ordinary Canadian retirement income, with the US taking its share first via withholding.

The trap: don’t withdraw before 59½

The single most expensive 401k mistake on a northbound move is an early withdrawal. If you take money out before age 59½, the US adds a 10% early-withdrawal penalty on top of regular income tax. That penalty is not creditable in Canada — there’s no corresponding Canadian tax to offset it against — so it’s a pure, unrecoverable cost. This is why “cash it out and start fresh in Canada” is the advice to run from: between US tax, the penalty, and lost deferral, it can cost a third of the account or more.

Required minimum distributions still apply

Moving to Canada does not switch off the US rules. A 401k (and a traditional IRA) is subject to required minimum distributions beginning at age 73. The US still expects those withdrawals to start on schedule, regardless of where you live, and they’ll flow through the same withholding-and-foreign-tax-credit treatment described above. If you also have Canadian registered accounts, note that an RRSP must convert to a RRIF by age 71 — so cross-border retirees often manage two separate withdrawal clocks.

Contributing to a 401k while living in Canada

If you’ve moved to Canada but still work for a US employer (or commute across the border), you may be able to keep contributing to a US employer plan and even deduct those contributions on your Canadian return, within limits the treaty sets out for cross-border workers. The rules are specific and situation-dependent — we cover them in deducting 401k contributions while working for a US employer.

403(b), 457, and Roth 401k accounts

If your US retirement savings sit in a 403(b) (non-profit and education employers) or a governmental 457(b) (state and municipal employers) rather than a 401k, the cross-border treatment is broadly the same: the treaty generally characterizes them as pensions, deferral continues in Canada, and withdrawals are taxed with the foreign tax credit. Non-governmental 457(f) plans are more complex and warrant individual advice.

A Roth 401k is different — it follows the Roth rules, not the traditional-401k rules, and a Roth 401k rolled into a Roth IRA can be protected by the same one-time treaty election that protects a Roth IRA. If you hold Roth-source money, read your Roth IRA after moving to Canada so you don’t miss the election deadline.

If you’re a US citizen or green-card holder

US citizens and green-card holders are taxed by the US on worldwide income wherever they live, so moving to Canada doesn’t end your US filing. Your 401k and any new Canadian accounts both feed your US information reporting (the FBAR, and often Form 8938). The 401k itself doesn’t create new headaches here — it’s a recognized US retirement account — but it’s part of the picture your cross-border accountant needs to see in full.

Your order of operations

- Before you leave the US: confirm your 401k custodian will keep servicing a Canadian-resident account or line up a cross-border-capable custodian for a rollover to an IRA. Take stock of all your US retirement accounts (including any Roth).

- At the move: decide leave-it vs roll-to-IRA. Don’t transfer to an RRSP or withdraw without modelling the US tax and penalty first.

- Ongoing: report any withdrawals on both returns, claim the foreign tax credit, file your W-8BEN with the custodian, and coordinate the RMD (73) and RRIF (71) clocks as you approach your 70s.

Frequently asked questions

What happens to my 401k when I move to Canada?

It can stay in the US and keep growing tax-deferred. Under Article XVIII of the treaty, Canada doesn’t tax the internal growth — only the withdrawals, with a foreign tax credit for any US tax paid. You don’t have to move or cash out the account.

What is the Canadian equivalent of a 401k?

The closest match is an RRSP, or an employer Group RRSP or defined-contribution pension plan if your Canadian employer offers one. All are tax-deferred, but contribution limits, matching, and withdrawal timing differ from a US 401k.

Do I have to move my 401k to Canada?

No. In most cases the best option is to leave it in the US (or roll it into an IRA for more flexibility), where it keeps deferring under the treaty. Transferring it into an RRSP is possible but usually costly before age 59½.

Will I be double-taxed on 401k withdrawals?

Not on the same dollars. The US withholds first (typically 15% on periodic pension payments with a W-8BEN on file), then Canada taxes the withdrawal and grants a foreign tax credit for the US tax. You effectively pay the higher of the two rates, not both.

Can I withdraw from my 401k early after moving to Canada?

You can, but it’s expensive. Before age 59½, the US applies a 10% early-withdrawal penalty on top of income tax, and that penalty is not recoverable through the Canadian foreign tax credit. Avoid early withdrawals unless there’s no alternative.

Do I still have to take RMDs if I live in Canada?

Generally yes. US required minimum distributions begin at age 73 on a 401k or IRA regardless of where you live. Separately, a Canadian RRSP must convert to a RRIF by age 71.

This article is general information for educational purposes, not personalized tax, legal, or investment advice. Cross-border rules are detail-sensitive and change over time; figures such as withholding rates and contribution limits can vary. Before acting, speak with a cross-border advisor qualified in both countries. 49th Parallel Wealth Management’s planning is led by a CFP® professional licensed in the US and Canada.

Moving north with a 401k? Book a cross-border review to map your options — leave it, roll it, or (rarely) transfer it — before you cross the border.