Roth IRA for Canadians: How to Keep Your Account Tax-Free After Moving North

DISCLAIMER: This article provides general educational information about US and Canadian retirement account rules and the Canada-US Tax Treaty. It is not legal, tax, accounting, or financial advice. The Article XVIII(7) treaty election is irrevocable; confirm details with the Canada Revenue Agency, the IRS, a cross-border tax accountant, and a qualified cross-border financial advisor before making decisions that depend on these rules.

By Lucas Wennersten, CFP® (US & Canada), CFA · Updated June 2026 · 12 minute read

A couple moved to Canada three years ago. They never filed one letter. It cost them their Roth

The following is an illustrative composite, not a specific client, but the mechanics and the outcome are real.

They were in their early sixties when they crossed the border from Seattle to Vancouver. Both had US-side careers behind them. They had built a combined $1.4 million across two Roth IRAs over twenty years of careful contributions and conversions. Tax-free retirement income on the US side, fully funded, paid up.

They told their Canadian accountant about the Roths in their first year. They asked the right questions. They did not get the right answer.

Three years later, they discovered their Canadian accountant had been quietly including the Roths’ annual internal growth — interest, dividends, capital gains — on their Canadian tax return every year. Tens of thousands of dollars of taxable income they had no idea they had reported. Worse: the omission of one specific letter to the Canada Revenue Agency, due by April 30 of their first Canadian tax year, has permanently changed the tax treatment of those accounts.

Here is the letter they needed to file, what happens if you miss it, and the full set of rules that govern a Roth IRA once you become a Canadian resident in 2026.

Can a Canadian have a Roth IRA?

The strict answer: no, not in the sense of opening a new account. A Roth IRA is a US tax-advantaged retirement account established under Internal Revenue Code §408A. Contributions require US-source earned income — wages, self-employment income, or similar compensation subject to US payroll taxes. A Canadian resident without US earned income cannot make a new contribution to a Roth IRA.

In practice, almost everyone we see holding a Roth IRA as a Canadian resident falls into one of three categories. They are former US residents — Americans, dual citizens, or green card holders — who moved north with an existing Roth. They are Canadians who worked in the US for some years, contributed to a Roth, returned to Canada, and now hold the account dormant. Or they are heirs who inherited a Roth from a US-resident parent or spouse and now hold the account as a Canadian-resident beneficiary.

If you fall into any of these categories, the question is not whether you can keep the Roth. You can. The question is what tax treatment applies to it on the Canadian side — and that depends almost entirely on one piece of paperwork most people never hear about until it is too late.

A note on the common confusion: a Canadian TFSA is not a Roth IRA equivalent in any meaningful regulatory sense, even though both work similarly from the holder’s perspective (after-tax contributions, tax-free growth, tax-free withdrawals in the home country). The two accounts have completely different cross-border treatment, which we cover in detail in our explainer on TFSAs for US persons.

What actually happens when you move to Canada with a Roth

By default, when you become a Canadian tax resident, the Canada Revenue Agency treats your Roth IRA as a foreign investment account. The interest, dividends, and capital gains accruing inside the account each year become taxable on your Canadian T1 return at your marginal rate. This applies regardless of whether you take any distributions. The CRA position is set out in Income Tax Folio S5-F3-C1, Taxation of a Roth IRA, which is the authoritative reference for everything in this article.

The default treatment defeats the entire point of the Roth. The account is tax-free in the US under §408A. Without action, it becomes annually taxable in Canada at top combined marginal rates of roughly 53.53% in Ontario, 54.00% in Nova Scotia, and about 53.50% in British Columbia. Two decades of careful tax planning get reversed overnight, simply because you crossed a border.

The fix is Article XVIII(7) of the Canada-US Tax Convention. The treaty allows a Canadian resident who owns a Roth IRA to make a one-time, irrevocable election treating the Roth as a pension for Canadian tax purposes. Once the election is filed, Canada respects the Roth’s tax-free growth, exactly as the US does, for the entire time the account is held.

The deadline is the filing-due date of your first Canadian T1 return — generally April 30 of the year following the year you became a Canadian resident. One election per Roth IRA account. The election is permanent: once filed, it is valid for the current year and every subsequent year you continue to be a Canadian resident, with no need to re-file.

Miss the deadline and the protection is not automatically lost. Contact the CRA Competent Authority Services Division and request a protective or late election. These have been accepted in many cases, particularly where the taxpayer can demonstrate the omission was an honest oversight and not a deliberate avoidance of Canadian tax. But you cannot count on this — every protective election adds delay, cost, professional fees, and the possibility of CRA refusing the late filing. The clean path is to file by the deadline.

The election letter: exactly what it must contain

This is where most retail articles get fuzzy. The election is not a CRA form. There is no Form RC267, no Form T1234, no checkbox on your T1 return. It is a letter — one letter per Roth IRA account — that you draft yourself, sign, and mail to a specific office at the CRA.

Per the CRA folio, the election letter must include:

- Your full name, address, Canadian Social Insurance Number (SIN), and US Social Security Number

- The name and address of the trustee or administrator of the Roth IRA (e.g., Fidelity, Vanguard, Schwab)

- The Roth IRA account number

- The date you became a Canadian resident

- The balance of the Roth IRA on the date you became a Canadian resident

- The amount and date of any Canadian Contribution made to the Roth, if any

- A signed statement: “I elect to defer taxation in Canada under paragraph 7 of Article XVIII of the Canada-US Tax Convention with respect to any income accrued in the Roth IRA for all tax years.”

The letter is sent to: Competent Authority Services Division, Canada Revenue Agency, 18th Floor, Canada Building, 344 Slater Street, Ottawa, ON K1A 0L5. (General enquiries only, no confidential information, can be emailed to CPMAPAPAG@cra-arc.gc.ca.) If you own more than one Roth IRA account — for example, a Roth IRA at one custodian and a Roth 401(k) rollover at another — you file a separate election letter for each account. Keep copies of every letter, along with all US tax documents (1099-R, Form 5498) and Roth transaction records. The CRA can request these years later to verify the taxable portion of the Roth, if any applies.

One operational note: many Americans moving north work with cross-border accountants who handle the election as part of the first-year T1 preparation. If you are working with a generic Canadian accountant who is unfamiliar with the Article XVIII(7) mechanics, the election is often missed. Make this a specific line item you ask about. We discuss broader first-year tax planning in our guide to Americans retiring in Canada

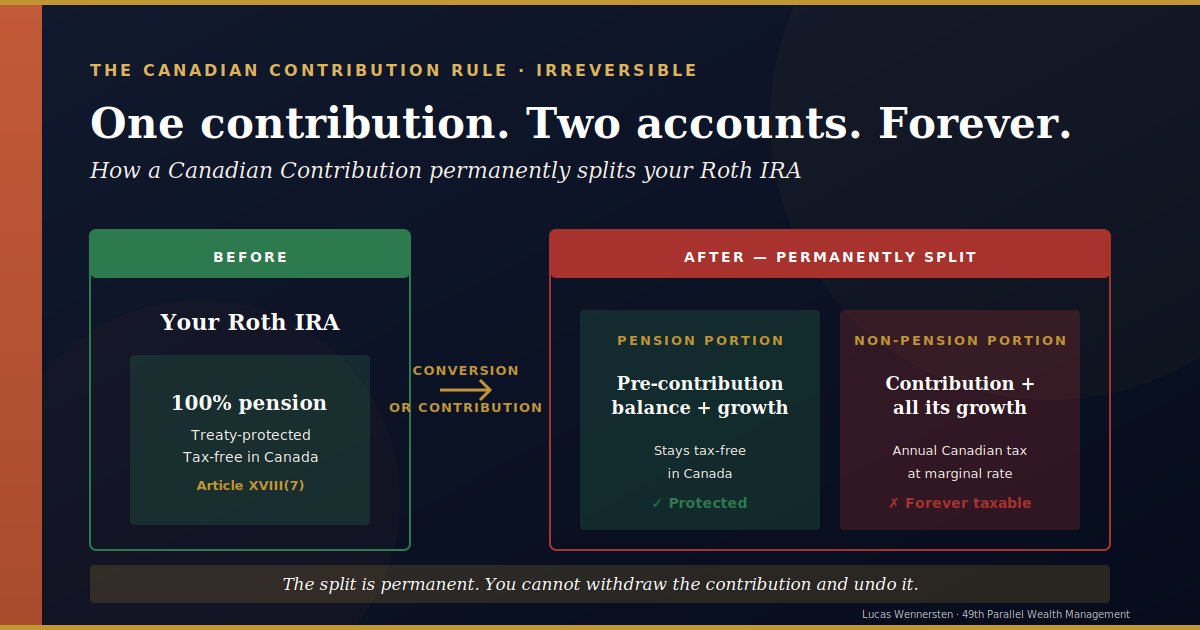

The Canadian Contribution trap

Once the election is filed, the Roth is protected. But there is one rule that, if violated, permanently and partially breaks the protection. The CRA calls this rule the “Canadian Contribution.”

Any contribution made to the Roth IRA while you are a Canadian resident contaminates the treaty election. The Roth does not lose its protection entirely — it gets split, permanently, into two accounting portions:

- The pension portion — the balance of the Roth IRA immediately before the Canadian Contribution, plus all treaty-protected growth accruing on that balance going forward. This portion continues to be tax-free in Canada under the original election.

- The non-pension portion — the Canadian Contribution itself, plus all growth accruing on that contributed amount going forward. This portion is annually taxable in Canada at your marginal rate, forever. The treaty does not protect it.

The split is permanent. Once the Roth is contaminated, you cannot undo it. You cannot withdraw the contribution and “unsplit” the account. Year over year, your custodian needs to track the two portions separately, and your Canadian tax preparer needs to include the non-pension portion’s accrual on your T1.

What counts as a Canadian Contribution? The CRA is explicit. It includes:

- Any new contribution to the Roth funded by US-source earned income while you are a Canadian resident (even if you are still legally allowed to contribute under US rules)

- A conversion from a Traditional IRA to a Roth IRA while you are a Canadian resident

- A rollover from a qualified retirement plan (like a 401(k)) to the Roth while you are a Canadian resident

What does NOT count as a Canadian Contribution:

- A rollover from one Roth IRA to another Roth IRA (custodian-to-custodian transfers)

- A rollover from a Roth 401(k) to a Roth IRA

- Any contribution made before 2009 (grandfathered under the Fifth Protocol)

The most common way otherwise-careful people contaminate their Roths is through Roth conversions executed while Canadian-resident. This is why the standard cross-border advice is to complete any planned Roth conversions BEFORE the move to Canada, not after. We cover this strategy in detail in Roth conversion strategy before crossing the border.

What you actually owe without the election

If the election is not made, the CRA’s default position is unambiguous. The internal growth of the Roth IRA — every dollar of interest, dividend income, and realized capital gain inside the account — is included in your Canadian taxable income on the year-by-year accrual basis. Not when you take a distribution. Not when you sell anything inside the account that the US side considers a non-taxable rebalancing. Every year, as income is generated inside the Roth, it is taxable in Canada.

The math compounds quickly. A $500,000 Roth invested in a diversified portfolio generating 6% returns produces $30,000 of taxable income in year one. At an Ontario top marginal rate of 53.53%, that is roughly $16,000 of Canadian tax owing — on income the US considers tax-free. Year after year, the bill grows in step with the account.

Worse, the holder typically has no withholding on this income, since the US side does not tax it and does not generate a 1099 for it. The Canadian tax liability sits silently on the return until either the holder discovers it or the CRA does. Interest on unpaid taxes compounds at the prescribed rate (7% annually as of 2026). Penalties for failure to report can apply on top.

Recovery, as noted earlier, runs through the CRA Competent Authority Services Division. A late or protective election may be accepted, but the process is unpredictable, and the time and professional fees involved often exceed the cost of getting it right the first time.

Distributions from a Roth IRA while you are in Canada

With a valid election in place and no Canadian Contribution, distributions from a Roth IRA to a Canadian-resident owner follow a clean treaty path. Under Article XVIII(1) of the treaty, distributions that qualify as tax-free under US Roth rules — generally meaning the account has been open at least 5 years and the owner is age 59½ or older — are also tax-free in Canada. No Canadian tax, no Canadian reporting beyond informational disclosure.

Non-qualified distributions (early withdrawals, account under 5 years) get more complex. The US side may apply a 10% early-withdrawal penalty plus ordinary income tax on the earnings portion of the withdrawal under IRC §408A(d). The Canadian side, if the election is in place, still treats the Roth as a pension and the distribution remains protected from Canadian tax. Any US tax paid is eligible for a foreign tax credit on the Canadian return via Form T2209.

US withholding on Roth distributions to a non-resident alien defaults to 30%. Under the treaty, periodic pension payments are reduced to 15% withholding when the recipient has filed a Form W-8BEN with the custodian claiming treaty benefits. For lump-sum distributions or non-periodic withdrawals, the 30% default may still apply unless other treaty positions are claimed. Coordinate with the Roth custodian before any distribution if you are no longer a US-resident taxpayer.

Sequence-of-withdrawal questions — which account to draw from first when you have a Roth, an IRA, an RRSP, and a TFSA — are a separate planning topic. We cover the broader framework in our analysis of decumulation strategy across both accounts

Roth IRA vs Canadian TFSA: what’s really the equivalent?

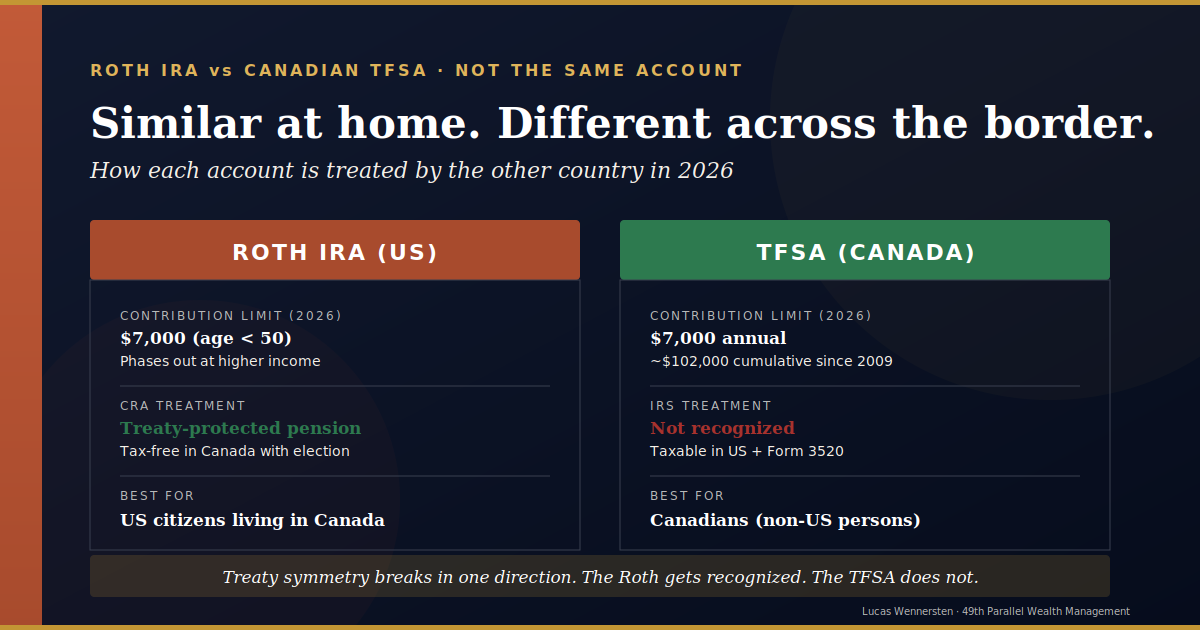

The most common framing online is that the TFSA is Canada’s Roth IRA. The framing is correct at the surface level — both are after-tax contribution accounts with tax-free growth and tax-free qualified withdrawals — and incorrect at the regulatory level, where the differences matter for cross-border families.

The TFSA was created by the Canadian government in 2009 with annual contribution limits ($7,000 in 2025 and 2026, cumulative $109,000 since 2009 for anyone resident throughout). Contributions are not deductible. Growth is tax-free in Canada. Withdrawals are tax-free in Canada. The account is fully tax-free for any Canadian holder.

The Roth IRA was created by US Congress in 1997. The 2026 contribution limit is $7,500 ($8,600 if you are age 50 or older). Direct contributions phase out at higher US income levels — between $153,000 and $168,000 of MAGI for single filers in 2026, and between $242,000 and $252,000 for married filing jointly. Contributions are not deductible. Growth is tax-free in the US. Qualified withdrawals are tax-free in the US.

The cross-border asymmetry is critical. The IRS does not recognize the TFSA as a tax-free account. For US persons (US citizens, green card holders, US-resident taxpayers), a TFSA is treated as either a foreign trust (full Form 3520/3520-A reporting) or a foreign investment account (annual taxable accrual on internal income). Either way, the TFSA is generally a bad tax structure for any US person living in Canada. The CRA, by contrast, recognizes the Roth as a pension under the treaty when the election is made. This is why US citizens in Canada often have Roths but should generally avoid TFSAs — the symmetry breaks in one direction only. We cover the inverse case for US persons in detail in our explainer on how the IRS taxes RRSP holdings for US dual citizens

Strategy: convert before you move

If you have a Traditional IRA and you are planning a move to Canada, the question of whether to convert the Traditional to a Roth IRA before crossing the border is one of the highest-leverage planning decisions you face. The math is rarely obvious and the answer depends on multiple variables, but the structural logic is consistent.

When you convert a Traditional IRA to a Roth IRA, you pay US federal income tax on the converted amount at your current US marginal rate. There may be state income tax in your departure state as well. After conversion, the Roth grows tax-free, and qualified withdrawals are tax-free.

Done while still a US resident, the conversion tax bill is calculated at US rates. Once you are a Canadian resident, the same conversion is treated as a Canadian Contribution — it contaminates the Roth, and the conversion amount is also subject to Canadian tax. The Canadian rate is generally higher than the US rate (top combined federal-provincial rates exceed 53% in most provinces, versus a US top federal rate of 37%). The double-rate problem makes post-move conversions costly.

Pre-move conversions are not always optimal, however. If your US-side current marginal rate is high (you are still working, in a top bracket) and you expect to be in a lower bracket once retired and in Canada, deferring withdrawals through a regular IRA may be cheaper overall. The break-even analysis turns on age, expected retirement bracket, time horizon to first withdrawal, and provincial tax rate at retirement.

Run the actual conversion math before you cross the border. Once the move is complete, the door on tax-efficient conversions is largely closed.

Frequently asked questions

Can a Canadian open a Roth IRA?

No, generally. Roth IRA contributions require US-source earned income subject to FICA. A Canadian-resident person without US-source earned income cannot make a new contribution to a Roth IRA. Almost everyone who holds a Roth IRA as a Canadian resident is a former US resident, a US citizen who moved north, or a beneficiary of an inherited Roth IRA.

What happens to my Roth IRA when I move to Canada?

The account can stay in the US — you do not have to close or transfer it. Without action, Canada taxes the annual internal growth of the Roth at your marginal rate. With the Article XVIII(7) treaty election filed by the deadline of your first Canadian tax return, Canada respects the Roth as a pension and the tax-free growth continues uninterrupted for as long as you are a Canadian resident.

What is the Article XVIII(7) treaty election?

A one-time irrevocable election under the Canada-US Tax Treaty that designates your Roth IRA as a pension for Canadian tax purposes. The election preserves tax-free growth and tax-free qualified withdrawals on the Canadian side. It is filed as a letter (not a prescribed CRA form) to the Competent Authority Services Division in Ottawa by the due date of your first Canadian tax return after becoming resident.

Is there a CRA form for the Roth IRA treaty election?

No. There is no prescribed CRA form. The election is a letter containing specific required information per CRA Income Tax Folio S5-F3-C1: your details, the trustee’s details, the account number, the date you became Canadian resident, the balance on that date, and the signed election statement referencing Article XVIII(7). One letter per Roth IRA account.

What is a Canadian Contribution and why does it matter?

Any contribution made to the Roth IRA while you are a Canadian resident, including conversions from a Traditional IRA and rollovers from a qualified plan (but not Roth-to-Roth rollovers). The trap: it permanently splits the Roth into two portions. The pre-contribution balance keeps its tax-free status. The contribution and all future growth on that portion become annually taxable in Canada at your marginal rate, forever. The split is irreversible.

Does converting a Traditional IRA to a Roth while in Canada count as a Canadian Contribution?

Yes. A conversion executed while you are a Canadian resident counts as a Canadian Contribution and contaminates the treaty election. This is why standard cross-border advice is to complete any planned Roth conversions before the move to Canada, paying the conversion tax at US rates rather than the higher combined Canadian rates.

What if I missed the treaty election deadline?

Not automatically lost. Contact the CRA Competent Authority Services Division — they may accept a late or protective election, particularly when the omission was an honest oversight. Until the late election is accepted, the CRA can include the Roth’s annual growth in your Canadian taxable income retroactively. Consult a cross-border tax accountant immediately if you discover the deadline has passed.

Are Roth IRA distributions taxed in Canada?

With a valid Article XVIII(7) election and no Canadian Contribution: qualified distributions are tax-free in Canada under Article XVIII(1) of the treaty, provided they qualify as tax-free in the US (account 5+ years and owner 59½+). Without the election, distributions get complex. US withholding on distributions to non-residents defaults to 30%, reduced to 15% for periodic pension payments with proper treaty documentation.

Do I have to report my Roth IRA on Form T1135?

No, if you filed the Article XVIII(7) election and have made no Canadian Contribution. The Roth is then exempt from T1135 (Foreign Income Verification) reporting. If the election was not filed OR a Canadian Contribution was made, the Roth must be included on T1135 if the cost amount of all your foreign property exceeds CAD $100,000.

Is a Canadian TFSA the same as a Roth IRA?

Functionally similar from each country’s domestic perspective — both are after-tax contributions with tax-free growth and tax-free qualified withdrawals — but legally completely different accounts under different regulatory regimes. The cross-border asymmetry matters most: TFSAs are not recognized by the IRS and create complex US tax problems for US persons, while Roths are recognized by the CRA via treaty election. US citizens living in Canada often hold Roths but should generally avoid TFSAs.

Get the election right the first time

The Roth IRA treaty election is one of the cleanest, lowest-cost pieces of cross-border tax planning a Canadian-resident Roth holder can do. The letter takes ten minutes to draft. The cost is a postage stamp. The benefit is decades of preserved tax-free growth on what is, for most cross-border families, one of the largest single retirement assets they hold.

The cost of getting it wrong is also asymmetric. The election is irrevocable in one direction (you can elect, you cannot un-elect). The Canadian Contribution rule is irreversible in the other (one contribution permanently splits the account). And the late-election remedy via the CRA Competent Authority Services Division is unpredictable, expensive, and not guaranteed.

If you are planning a move to Canada with one or more Roth IRAs, or if you have already moved and want to confirm the election was filed correctly, book a complimentary consultation . We will walk through the specific situation, identify whether the election has been filed and is current, flag any Canadian Contribution exposure, and coordinate the planning with your existing tax accountant. Lucas Wennersten is CFP®-licensed in both Canada and the United States and holds the CFA charter; 49th Parallel Wealth Management is dually registered to advise on both sides of the border.

Lucas Wennersten is the founder of 49th Parallel Wealth Management and a dual-certified financial planner (CFP® US & Canada) and Chartered Financial Analyst (CFA). With a career spanning both Arizona and Toronto, Lucas brings firsthand experience navigating cross-border finances to every client relationship.