| DISCLAIMER: This article provides general educational information about Canadian and US estate tax rules. It is not legal, tax, accounting, or financial advice. Tax rules change. Confirm current details with the Canada Revenue Agency, the Internal Revenue Service, a cross-border tax accountant, and a qualified cross-border financial advisor before making decisions that depend on these programs. |

By Lucas Wennersten, CFP® (US & Canada), CFA · Published May 2026 · 11 minute read

Canada doesn’t have an inheritance tax. It has something else — and almost nobody gets it right

A client emailed me last month, panicked. Her mother had died in Toronto in February. She had heard from a relative that the Canadian government was going to “take half” of the family home and the modest brokerage account her mother left behind.

She was wrong. But not in the way she expected.

Canada does not have an inheritance tax. Not the way many countries do. Not the way the United States does. Heirs in Canada do not file an inheritance tax return. Heirs do not pay a percentage of what they receive to the CRA.

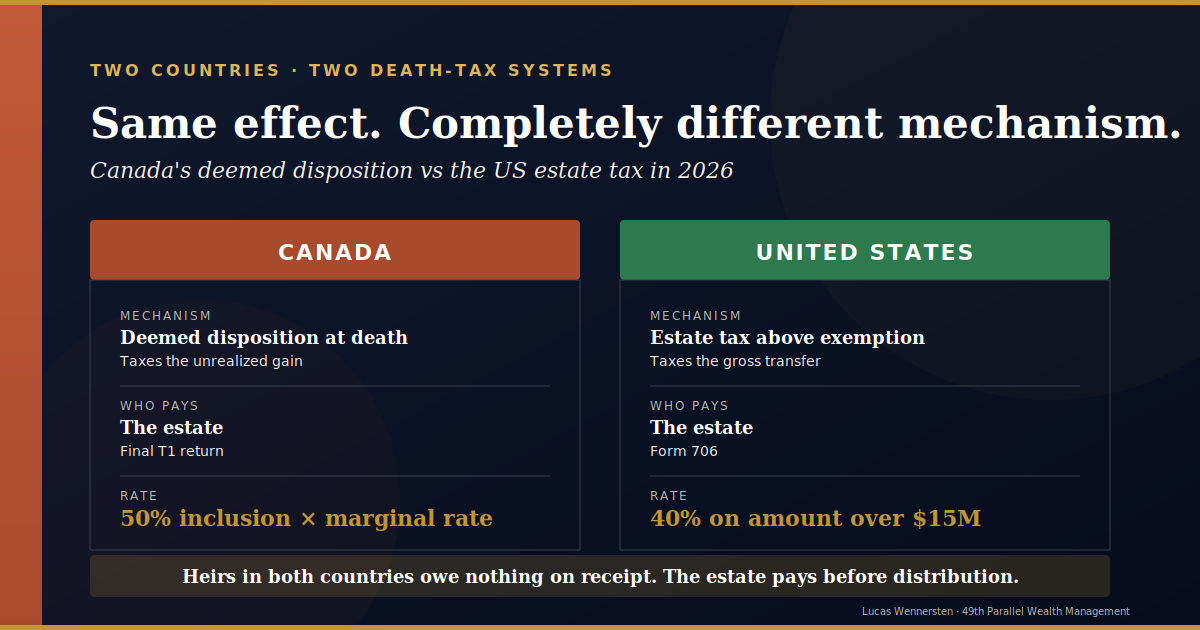

What Canada has is something different: deemed disposition. At death, the deceased is treated as if they sold every capital asset they owned at fair market value the moment before they died. Capital gains crystallize. The estate pays tax on the unrealized appreciation. Heirs receive the net amount.

Similar effect in the end. Completely different mechanism. And once you add cross-border elements — a Canadian inheriting from a US parent, an American inheriting from a Canadian parent — almost every retail article gets the details wrong.

Here’s how it actually works in 2026, and what your family actually owes.

How Canada’s deemed-disposition system actually works

Under section 70(5) of the Income Tax Act, every person who dies is deemed to have disposed of all their capital property at fair market value (FMV) immediately before death. Per the CRA’s deceased-taxpayer guide T4011, the deemed disposition triggers capital gains tax on the unrealized appreciation in those assets between when they were acquired and the date of death.

The capital gain is the difference between FMV at death and the adjusted cost base — what the deceased originally paid, plus eligible adjustments. Fifty percent of that gain is included in the deceased’s income on their final T1 return, filed by the executor. The proposed increase to 66.67% on gains above $250,000 was cancelled by the federal government on March 21, 2025 — the inclusion rate remains 50% for all individuals in 2026.

That 50% inclusion is then taxed at the deceased’s marginal rate on the final return. In Ontario, a top-bracket taxpayer faces a combined federal-provincial marginal rate around 53.5%. The effective tax on a deemed-disposition gain is therefore approximately 50% × 53.5% = 26.8% of the gain itself, not the gross value of the asset.

Three exceptions matter most:

- Spousal rollover (section 70(6)): assets passing to a surviving spouse or common-law partner roll over at the deceased’s adjusted cost base. The deemed-disposition trigger defers to the second spouse’s death. This is the single most important tax-planning lever in Canadian estates.

- Principal residence exemption: the deemed gain on the family home is fully sheltered. One designated principal residence per family unit per year. This eliminates what would otherwise be the largest single gain in most middle-class Canadian estates.

- Registered accounts: RRSPs and RRIFs are not subject to deemed disposition the same way. Instead, the full fair market value of the registered plan is included as ordinary income on the final return — unless the plan rolls to a surviving spouse or financially-dependent child. The tax bite on a large RRSP without a surviving spouse can be brutal.

The estate, not the heirs, pays this tax. Heirs receive the net amount after the executor settles the deceased’s final return. For deeper coverage of how cross-border estates work in practice, see our cross-border estate planning framework.

How US estate tax differs: exemption-based, not disposition-based

The US estate tax works on a completely different premise. Per IRS estate tax guidance, the system is exemption-based. Each US person can transfer a defined dollar amount of wealth at death without owing any federal estate tax. Below that line: zero tax. Above it: 40% on the overage.

In 2026, the exemption is $15 million per person — $30 million for a married couple using portability — up from $13.99 million in 2025. This increase was made permanent by the One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025. The widely-anticipated TCJA sunset that would have dropped the exemption back to roughly $7 million did not happen. Starting in 2027, the $15 million figure adjusts annually for inflation.

Two consequences flow from this. First, the federal US estate tax now affects very few estates — somewhere around 0.1% of Americans, or about 4,000 estates per year nationally. Second, 12 US states plus the District of Columbia impose their own state-level estate or inheritance taxes, often with much lower exemption thresholds, so state-level planning still matters even for estates well under $15 million.

For the gift side: the annual gift tax exclusion remains $19,000 per recipient in 2026 ($38,000 for married couples splitting gifts). Gifts to a non-US-citizen spouse have a special annual exclusion of $194,000 — important for mixed-citizenship couples where one spouse is Canadian.

The mechanism is fundamentally different from Canada’s. Canada taxes the gain. The US taxes the gross transfer value above an exemption. A $20 million estate consisting entirely of cash with zero unrealized gains owes Canada nothing on deemed disposition (no gain), but owes the US a substantial estate tax (the gross value is above the exemption). The reverse is also true.

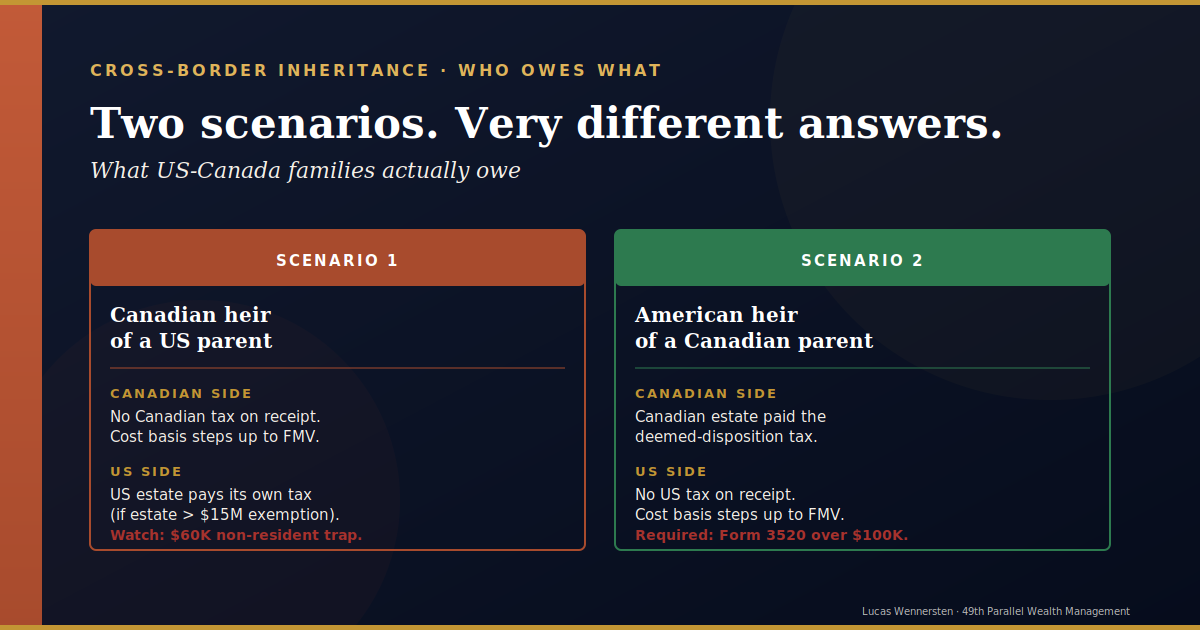

Scenario 1: You’re a Canadian inheriting from a US parent

This is the more common cross-border scenario in practice. A Canadian-resident adult child inherits from an American parent who died in the United States. The question that drives the consultation: “What do I owe?”

On the Canadian side, nothing. Canada has no inheritance tax. You owe the CRA no tax on the receipt of the inheritance itself. The Canadian-side cost basis of any inherited assets is reset to the fair market value as of the parent’s date of death — a clean stepped-up basis for your future Canadian capital gains calculations.

On the US side, the analysis depends entirely on the parent. If the US parent was a US citizen or US-domiciled resident, their estate had access to the full $15 million federal exemption. For the typical middle-class American estate, the federal estate tax is zero. State-level estate or inheritance tax may apply depending on the state of residence — Massachusetts, New York, and Oregon are particularly aggressive, each with their own state exemption thresholds well below the federal.

The cross-border trap is different and catches many cross-border families. If the deceased was a non-US-domiciled individual — for example, a Canadian who owned US property at death, or a US permanent resident who never naturalized — their US estate tax exemption is not $15 million. It is $60,000. This is the same $60,000 figure that has been on the books for decades, unindexed for inflation. The exemption applies to US-situs assets only, but it captures more than people expect: directly-held US real estate, US-listed stocks held in a US brokerage, and certain other US-source assets all count. We cover this trap in detail in our analysis of US estate tax exposure for Canadians holding US assets.

The US-Canada Tax Treaty, specifically Article XXIX-B, partially addresses this disparity for Canadians by providing a pro-rata extension of the unified credit and a Canadian credit for US estate tax paid. The treaty text is available from the Department of Finance Canada. The mechanics are technical and the available relief depends on the size of the worldwide estate, but the credit can be meaningful in HNW cross-border cases.

For inherited assets that you continue to hold, the cost basis step-up at death operates on both sides of the border. Future Canadian capital gains use the FMV at the parent’s death as the new ACB. Future US capital gains — if you remain subject to US tax for any reason — use the FMV at death as the new basis under section 1014.

Scenario 2: You’re an American inheriting from a Canadian parent

This is the scenario that drives more of the actual planning calls at our firm — typically from Americans retiring in Canada, or US citizens who left Canada decades ago and have a parent still in Vancouver or Toronto.

On the Canadian side, the Canadian parent’s estate paid the deemed-disposition capital gains tax on the parent’s final T1. By the time the inheritance reaches you, the Canadian tax has already been settled. You owe Canada nothing as the heir. There is no Canadian inheritance tax to file or report.

On the US side, the analysis is more involved. The receipt of an inheritance from a non-US person is not subject to US income tax. But if the gross value of inheritances and gifts from non-US persons exceeds $100,000 in a calendar year, the US recipient must file IRS Form 3520. This is an informational return — it does not generate a tax bill — but the penalties for non-filing are severe, starting at 5% of the unreported amount per month up to 25%.

Inherited Canadian-situs assets receive a stepped-up cost basis under section 1014 for your future US-side capital gains calculations. The FMV at the Canadian parent’s date of death becomes the new US-side basis.

Two specific asset types require closer attention. Inherited RRSPs and RRIFs are not treated as ordinary inheritances under the treaty. The plan must usually be collapsed, with the Canadian estate paying the full income inclusion on the final return. Withholding tax then applies on distributions to the US heir, with treaty relief available. The mechanics are similar to issues we cover for your first tax year in Canada as an American, but in reverse — you’re a US person receiving from a Canadian source.

The second issue is foreign trust exposure. If your inheritance arrives via a Canadian alter-ego trust, joint-partner trust, or testamentary trust, you may have ongoing Form 3520 and Form 3520-A reporting obligations as a US beneficiary of a foreign trust. The penalties stack annually. This is one of the most common cross-border compliance failures we see — the heir takes the inheritance, files nothing, and discovers years later that the IRS treats the situation as a foreign-trust reporting violation.

Provincial probate fees: not the same as inheritance tax

Probate fees are the single most commonly confused element of the Canadian death-tax picture. They are not inheritance tax. They are administrative charges paid to the provincial court to confirm the executor’s authority to act on the estate. The fee structure varies dramatically by province.

In Ontario, the fee is called the Estate Administration Tax. It is 0% on the first $50,000 of estate value and 1.5% on everything above. A $1 million Ontario estate owes $14,250 in EAT (the first $50,000 is exempt). A $5 million estate owes $74,250. The fee is paid at the time of probate application — typically months before the deemed-disposition capital gains return is filed.

British Columbia charges 0.6% on estate value between $25,000 and $50,000, and 1.4% on everything above $50,000. Alberta caps probate fees at a flat $525 maximum regardless of estate size. Quebec charges nothing in probate fees for notarized wills, which is one reason notarial wills are the dominant form in that province. Manitoba eliminated probate fees entirely in 2020.

These fees are levied on the assets that pass through the probated estate. Assets held in joint tenancy with right of survivorship transfer outside probate. Registered accounts with a named beneficiary transfer outside probate. Life insurance with a named beneficiary transfers outside probate. Real estate held in joint tenancy transfers outside probate. Strategic use of these designations can dramatically reduce the probate fee bite in high-fee provinces like Ontario and British Columbia.

Probate fees are paid by the estate before distribution to heirs. Heirs do not owe probate fees directly. This is why the “Canada has no inheritance tax” statement is technically true even though Ontario residents pay what looks like one — the EAT is a probate administration fee, not a tax on the heir.

What the estate owes vs what heirs owe

In Canada: the estate pays. The executor files the deceased’s final T1, pays the deemed-disposition capital gains tax, pays probate fees, and only then distributes the net assets to heirs. Heirs receive the net amount. Heirs themselves file no inheritance tax return and owe nothing on the receipt.

In the US: the estate pays the federal estate tax (if applicable above the $15 million exemption). The executor files Form 706 and settles before distribution. Heirs receive the net amount with stepped-up basis. Exception: a handful of US states impose true inheritance taxes payable by the heir — Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. These are state-level inheritance taxes with rates varying by relationship to the deceased (children typically pay less than nephews). They are separate from the federal estate tax and are the only place in the North American system where the heir actually writes a cheque to a tax authority.

Strategies to minimize the bite

Five strategies do most of the work in cross-border estate planning:

- Principal residence exemption — designate the family home properly to eliminate the gain on what is usually the largest single asset in a middle-class Canadian estate.

- Spousal rollover — assets passing to the surviving spouse defer Canadian deemed disposition to the second death. In cross-border couples, the spouse’s country of residence and citizenship affects the rollover’s interaction with US rules.

- Lifetime gifting under US annual exclusion — $19,000 per recipient per year ($38,000 split) reduces the gross estate without using any lifetime exemption. For HNW Canadians with US-citizen children or grandchildren, this is an underused lever.

- Joint ownership and beneficiary designations — bypass probate in high-fee provinces. Caveats apply where joint accounts trigger attribution rules or accidentally trigger immediate dispositions.

- Estate freezes for business owners — cap the deemed-disposition gain at current FMV by transferring future appreciation to the next generation via preferred shares and common shares. The Lifetime Capital Gains Exemption increased to $1.25 million effective June 25, 2024, multiplying the value of a properly executed freeze.

Liquidity planning matters as much as tax minimization. A $5 million Canadian estate with a $2 million deemed-disposition gain plus Ontario EAT may owe $300,000 in tax and fees before any distribution. If the estate’s assets are illiquid — the family business, real estate — the executor may face forced sales at unfavourable timing. Permanent life insurance with the estate as beneficiary is the traditional liquidity solution.

Frequently asked questions

Does Canada have an inheritance tax?

No. Canada does not have an inheritance tax. Heirs in Canada do not file an inheritance tax return and do not owe tax on the receipt of an inheritance. What Canada has is deemed disposition, where the deceased’s estate pays capital gains tax on unrealized appreciation in capital assets as of the date of death. The estate pays before distribution; heirs receive the net amount.

What is deemed disposition at death?

Deemed disposition is the rule under section 70(5) of the Income Tax Act that treats the deceased as having sold all their capital property at fair market value the moment before death. Capital gains crystallize, 50% of the gain is included in the deceased’s income on the final T1 return, and the estate pays tax at the deceased’s marginal rate. Two key exceptions: spousal rollover and the principal residence exemption.

How is the principal residence exemption applied at death?

The principal residence exemption fully shelters the capital gain on a property that was the deceased’s designated principal residence for every year of ownership. Only one principal residence can be designated per family unit per year. For most middle-class Canadian estates, the family home is the largest single asset, and the PRE eliminates what would otherwise be the largest single deemed-disposition gain.

As a Canadian, do I pay US estate tax if I inherit from a US parent?

No, you do not pay it personally. The US estate (the deceased parent’s estate) pays the US estate tax if applicable, before distribution. You receive the net amount. The Canadian heir’s future Canadian capital gains calculations use the fair market value at the parent’s death as the new adjusted cost base, giving a clean stepped-up basis on the Canadian side.

As an American, do I pay any Canadian tax if I inherit from a Canadian parent?

No Canadian inheritance tax — Canada does not have one. The Canadian parent’s estate paid the deemed-disposition capital gains tax on the final T1 before distribution. Your US obligation is informational: if the gross value of inheritances and gifts from non-US persons exceeds $100,000 in a year, you must file IRS Form 3520. This is not a tax return — no tax is due — but penalties for non-filing are severe.

What is the $60,000 US estate tax exemption trap?

Non-US individuals not domiciled in the United States have only $60,000 of US estate tax exemption for US-situs assets, not the $15 million that applies to US citizens and US-domiciled residents. This catches Canadians who own US real estate, US-held brokerage accounts, or US stocks at death. The US-Canada Tax Treaty Article XXIX-B provides a partial pro-rata extension of the unified credit, but the exposure can still be substantial for HNW Canadians with US assets.

How does the US-Canada Tax Treaty help Canadians with US estate tax?

Article XXIX-B of the US-Canada Tax Treaty provides two main relief mechanisms. First, a pro-rata extension of the US unified credit based on the ratio of US-situs assets to worldwide assets, which expands the effective US exemption beyond the bare $60,000. Second, a Canadian credit for US estate tax paid on US-situs assets, which prevents double taxation when the same assets generate Canadian deemed-disposition tax and US estate tax.

Are probate fees the same as inheritance tax?

No. Probate fees are administrative charges paid to the provincial court to validate a will and confirm the executor’s authority. They are paid by the estate, not the heir. Ontario calls them Estate Administration Tax (1.5% on estate value above $50,000); BC charges 1.4% above $50,000; Alberta caps fees at $525; Quebec and Manitoba charge nothing for valid notarized or registered wills. Joint ownership and beneficiary designations bypass probate.

What’s the difference between deemed disposition and US estate tax?

Deemed disposition is a capital gains tax — it taxes the unrealized appreciation in assets at the deceased’s marginal rate, on 50% of the gain (the inclusion rate). US estate tax is a transfer tax — it taxes the gross value of the estate above the $15 million exemption at a flat 40% rate. A $10 million estate with no unrealized gains owes Canada nothing on deemed disposition but would owe the US estate tax on the portion above the exemption (if applicable based on US-person status).

Can I avoid or reduce Canadian capital gains tax at death?

Several strategies reduce the deemed-disposition tax burden. Spousal rollover defers the trigger to the second spouse’s death. The principal residence exemption eliminates the gain on the family home. Estate freezes cap the gain at current FMV for business owners and let future appreciation accrue to heirs. Charitable bequests provide a full deduction on the final return. Permanent life insurance creates liquidity to pay the tax without forced asset sales. These are layered, not exclusive — most cross-border estate plans use several.

Plan your cross-border estate with the right starting facts

Most cross-border estate-planning conversations start with a wrong premise. “Canada will take half.” “The US will tax my inheritance.” “Mom’s RRSP will be 50% tax at death.” Almost none of these are correct as stated. The actual rules are more nuanced, more navigable, and more amenable to planning than the fear narrative suggests.

If you are modelling a cross-border estate — whether you are the parent planning ahead, the heir trying to understand what’s coming, or an executor working through a recent loss — the facts in this article are the starting point, not the endpoint. Specific situations turn on details: domicile, citizenship, residence, asset location, ownership structure, beneficiary designations. Book a complimentary consultation to walk through your specific picture. Lucas Wennersten is CFP®-licensed in both Canada and the United States, holds the CFA charter, and 49th Parallel Wealth Management is dually registered to advise on both sides of the border.