Estate Planning for Mixed-Citizenship Couples: When One Spouse Is a US Citizen and the Other Is Canadian

By Lucas Wennersten, CFP® (US & Canada), CFA · 49th Parallel Wealth Management · Reading time: ~12 minutes

DISCLAIMER · This article provides general information about cross-border estate planning for couples with mixed US and Canadian citizenship. It is not personalized tax, legal, or financial advice. Tax laws change, the rules summarized here have technical requirements not fully captured in a single article, and your specific situation depends on your assets, residency, citizenship history, and the law of your province or state. Consult a cross-border tax attorney and dual-licensed financial advisor before acting on any of the strategies described.

Cross-border families share a quiet assumption — that being married protects them from the worst of the cross-border tax mess. For most cross-border couples, that’s broadly true. For mixed-citizenship couples — where one spouse is a US citizen and the other is Canadian — it isn’t.

The US estate tax system treats a non-US citizen surviving spouse very differently from a US citizen one. The unlimited marital deduction that allows assets to pass tax-free between US citizen spouses doesn’t apply when the survivor is a non-citizen. Annual gifts between spouses are capped at a fraction of what they would otherwise be. And once the US citizen spouse’s worldwide assets — including everything they own in Canada — start being valued for US estate tax purposes, the planning gaps that didn’t matter while both spouses were alive can become expensive within months of the first death.

This article is for cross-border couples where one spouse holds US citizenship (by birth, naturalization, or descent) and the other is a Canadian citizen and resident. It walks through how cross-border estate planning works when the marital deduction doesn’t behave the way most planners assume, what a Qualified Domestic Trust (QDOT) does, why FATCA quietly attaches to your joint checking account, and how a real $4 million household plays out in practice. The work is technical. The fixes are not.

The unlimited marital deduction problem: why non-US citizen spouses are taxed differently

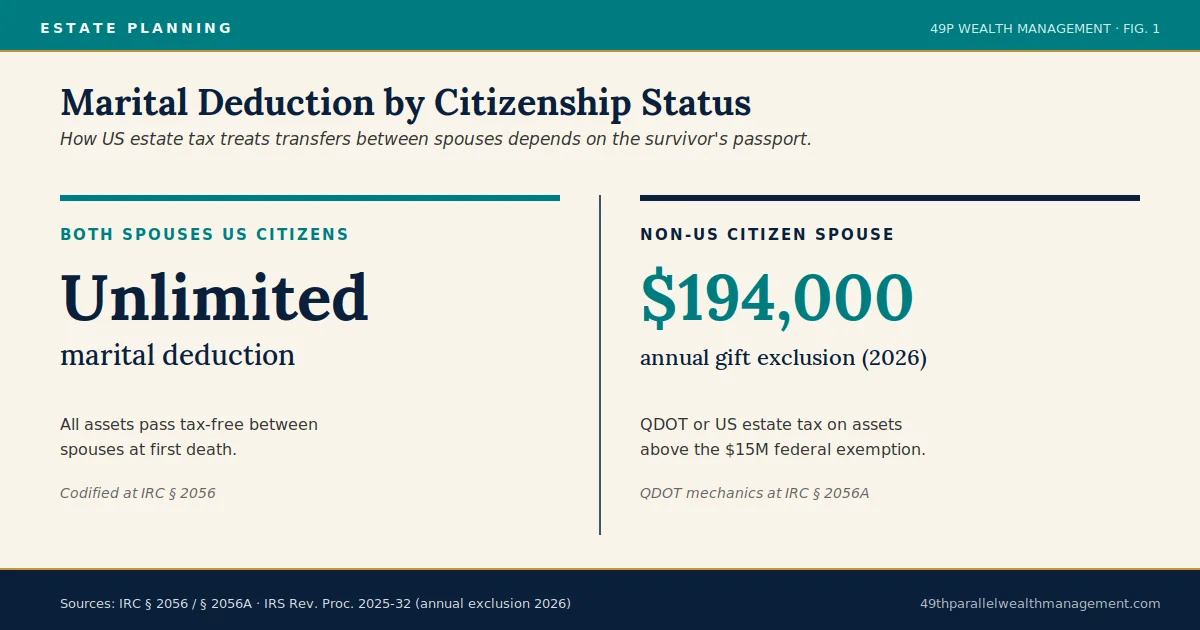

The US estate tax allows a deceased US citizen to transfer unlimited assets to a surviving US citizen spouse without triggering federal estate tax. This is the unlimited marital deduction, codified at IRC Section 2056. It is one of the most foundational provisions in the US estate tax system. It does not apply when the surviving spouse is not a US citizen.

When a US citizen dies and leaves assets to a non-US citizen spouse, those transfers become taxable to the deceased’s estate to the extent they exceed the federal estate tax exemption ($15 million USD per individual in 2026). For an estate above that threshold, the missing marital deduction can mean a 40% federal estate tax bill on assets that would have passed tax-free to a US citizen spouse.

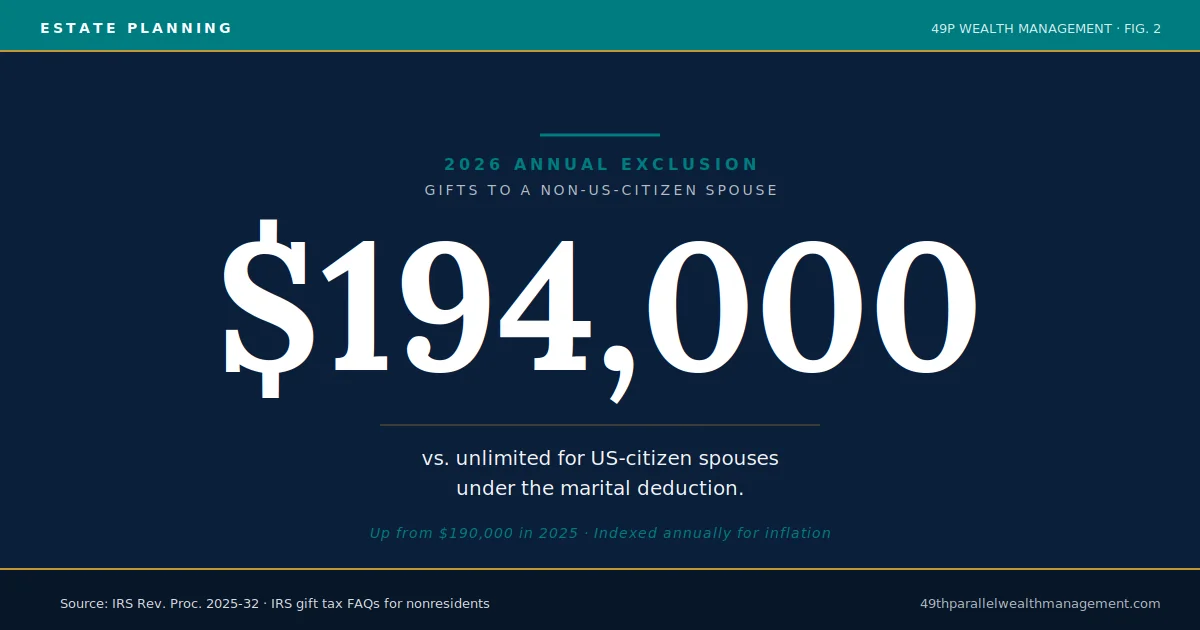

The same restriction applies to gifts during life. A US citizen can give an unlimited amount to a US citizen spouse during the marriage with no gift tax consequences. The same gift to a non-US citizen spouse is capped at the annual exclusion amount: $194,000 USD for 2026, indexed each year (IRS frequently asked questions on gift taxes for nonresidents). Gifts above that annual cap to a non-citizen spouse start using up the citizen spouse’s lifetime exemption.

The reasoning behind the rule is that a non-US citizen spouse may be able to leave the country with the inherited assets and never pay US estate tax on them. The unlimited marital deduction works for citizen-to-citizen transfers because at the surviving spouse’s eventual death, the assets are still within reach of the IRS. Without that backstop, the IRS limits the amount that can flow to a non-citizen spouse without immediate taxation.

Two things follow from this:

First, the size of the estate matters. For couples whose combined assets are well below $15 million USD per spouse, the missing marital deduction is largely theoretical. The federal exemption alone shelters most or all of the estate. For couples above that threshold — and for high-asset couples in expensive markets like Toronto, Vancouver, or the Bay Area, this happens faster than people expect — the gap is real.

Second, citizenship status of the surviving spouse, not domicile, is what controls. A Canadian citizen who has lived in the US for thirty years and holds a green card is still a non-US citizen spouse for marital deduction purposes. Naturalization, or one of the workarounds described below, is what closes the gap.

QDOT trusts: the workaround for non-citizen spouses

The Qualified Domestic Trust, defined at IRC Section 2056A, is the standard mechanism the US tax code provides for closing the marital deduction gap. A properly structured QDOT allows assets passing to a non-US citizen surviving spouse to qualify for the marital deduction — but the deduction is conditional, not absolute.

The mechanics are this: instead of leaving assets directly to the non-citizen spouse, the deceased spouse leaves them to a trust meeting QDOT requirements. The surviving spouse receives income from the trust during their lifetime. US estate tax on the trust assets is deferred — not eliminated — until either (a) the surviving spouse takes principal distributions from the trust, or (b) the surviving spouse dies. At those points, the deferred US estate tax becomes payable on IRS Form 706 or its QDOT-specific equivalent, Form 706-QDT.

For the trust to qualify as a QDOT, three structural requirements must be met. At least one trustee must be a US citizen or US corporation. That trustee must have the right to withhold US estate tax on any principal distribution before the distribution is made. And if the trust value exceeds $2 million USD, additional security is required: either a US bank as trustee, a bond posted to the IRS at 65% of the trust’s fair market value, or an irrevocable letter of credit at the same 65% Treasury Regulation §20.2056A-2(d) sets all three options.

Three things are worth understanding clearly:

QDOTs defer estate tax — they do not eliminate it. The same federal estate tax that would have been due at the first death is paid later, when the surviving spouse dies or takes principal. The benefit is the deferral period, during which the surviving spouse can use the income from the trust, and the assets can grow.

Income distributions are not taxed under the QDOT framework. Only principal distributions trigger the withheld tax. The surviving spouse can take ordinary investment income from the trust without losing the deferral. Hardship distributions of principal can also be made without triggering tax in defined cases, but those rules are narrow and fact specific.

Naturalization closes out the QDOT requirement. If the non-citizen surviving spouse becomes a US citizen before the first US estate tax return is filed (and meets continuous-residency conditions in the US during the period between death and naturalization), the marital deduction applies as if the spouse had always been a citizen, and the QDOT structure is unwound. Some Canadian-citizen surviving spouses pursue naturalization specifically for this reason.

QDOTs are powerful but they come with costs: trustee fees, ongoing administrative complexity, potentially restricted investment flexibility, and the possibility that the surviving spouse outlives the trust value or wants to move back to Canada. Whether a QDOT is the right answer, whether the spouse should pursue naturalization, or whether the estate is small enough that neither matters depends on the specific numbers. There is no rule of thumb worth applying without doing the math.

FATCA, FBAR, and joint accounts: the reporting trap

The US estate tax problem is the headline issue for mixed-citizenship couples. The reporting issue is the quiet one — and it can be more disruptive on a daily basis.

A US citizen is subject to US tax and reporting on their worldwide income and assets, regardless of where they live. When the US citizen spouse has any signature or financial interest in a Canadian financial account, US reporting attaches to that account. Two separate reporting regimes apply.

The first is the Foreign Bank Account Report. FinCEN Form 114 — commonly called the FBAR — requires US persons to report foreign financial accounts when the aggregate balance exceeds $10,000 USD at any point during the year. The threshold is per filer, not per account. A US citizen spouse who has signature authority on the Canadian spouse’s checking account, savings account, joint investment account, or any combination that crosses $10,000 USD in aggregate must file.

The second is FATCA reporting. IRS Form 8938 — Statement of Specified Foreign Financial Assets — applies at higher thresholds (varying by filing status and residency) but covers a wider range of assets, including foreign mutual funds, foreign retirement accounts, and certain insurance products with cash value.

For mixed-citizenship couples, three patterns recur:

Joint checking and savings accounts are the most common reporting trigger. Once added to a joint Canadian account, the US citizen spouse must include the full account balance on FBAR — not just their proportional share. The Canadian spouse’s separate accounts to which the US spouse has no signature authority do not need to be reported by the US spouse.

Canadian mutual funds and ETFs trigger PFIC reporting on the US citizen’s share. Most Canadian-domiciled investment funds are classified as Passive Foreign Investment Companies under the IRS PFIC rules. PFIC tax treatment is punitive — gains can be taxed at the highest US ordinary income rate plus an interest charge — and reporting is on Form 8621 annually. Holding Canadian funds in a joint account makes them a US problem; holding them in the Canadian spouse’s name only does not.

Registered accounts should generally be in the Canadian spouse’s name only. TFSAs, FHSAs, and RESPs offer no US tax deferral and may be classified as foreign trusts requiring additional reporting if the US citizen spouse has any beneficial interest. Keeping these accounts in the Canadian spouse’s name avoids triggering US reporting on them.

Beneficiary designations across two estate systems

Estate plans for mixed-citizenship couples often focus on wills and miss the beneficiary designations on registered accounts. The designations frequently override the will. They are also where most of the cross-border tax friction shows up.

For a Canadian-resident spouse holding an RRSP or RRIF where the surviving spouse is a US citizen: the standard rule is that a direct beneficiary designation to a qualifying spouse allows the account to roll over tax-free for Canadian purposes under spousal rollover provisions. The full tax burden that would have been triggered by the deemed disposition at death is deferred until the surviving spouse withdraws the funds. This works regardless of the surviving spouse’s citizenship for Canadian tax purposes.

The US treatment of the same account when the surviving spouse is a US citizen is more nuanced. Under the Canada-United States Tax Convention, a US person can elect to defer US tax on the growth inside an inherited Canadian retirement account, treating it analogously to a US-deferred retirement plan. The election is made annually on the US tax return and must be properly documented. Without the election, the inheritance can lose treaty protection, and growth becomes taxable in the US each year — which compounds quickly on a Canadian tax-deferred plan.

For a US citizen spouse holding an IRA or 401(k): naming the Canadian spouse as direct beneficiary is generally optimal, but it triggers Canadian and treaty considerations. Periodic distributions from the inherited IRA to the Canadian-resident spouse face a 15% US withholding tax under Article XVIII of the Canada-US Tax Treaty (lump-sum withdrawals can default to 30% absent valid treaty documentation), with the income reportable on the spouse’s Canadian return and the withheld US tax claimable as a foreign tax credit. The inherited IRA itself can remain US-tax-deferred for the surviving spouse if managed correctly, but the Canadian tax treatment of distributions follows different rules from those that would apply to an RRSP.

Three actions to take regardless of the size of the estate:

Confirm primary and contingent beneficiaries are correct on every registered account on both sides of the border. Many cross-border families have stale designations from before they crossed the border, before they married, or before children were born. The designations override the will.

If the US citizen spouse holds an IRA or 401(k), document the Canadian-resident contingent beneficiary in writing and confirm the plan administrator can accept a non-US-resident beneficiary. Some US plans have administrative limits or require a US trustee.

If the Canadian spouse holds an RRSP or RRIF and the US citizen spouse is the beneficiary, document the treaty election plan for the year of death. The election is filed by the surviving spouse, not by the deceased — and the surviving spouse will be grieving, possibly disoriented, and unlikely to research IRS treaty procedures. Have the plan written down before it’s needed.

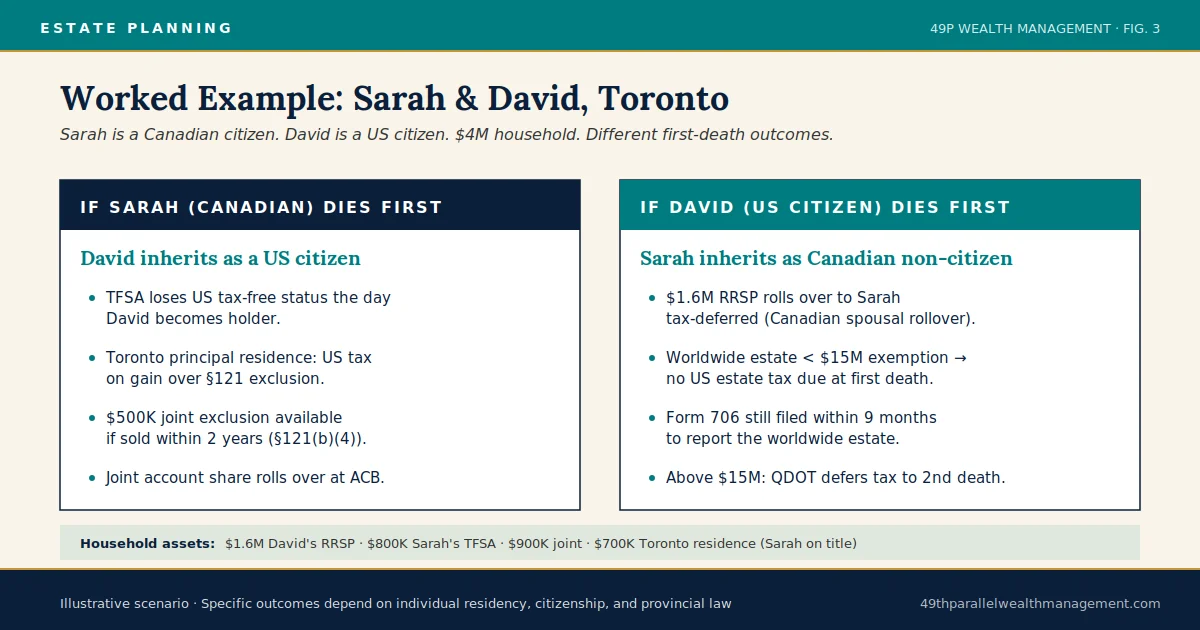

A worked example: Sarah and David in Toronto

Sarah is a Canadian citizen and resident. David is a US citizen who has lived in Canada for fifteen years; he never naturalized as a Canadian citizen. They are married, live in Toronto, and hold the following:

- $1.6M in David’s RRSP (rolled in from his US 401(k) over the years)

- $800K in Sarah’s TFSA (held in her name only because the TFSA is not US-tax-deferred — keeping it out of David’s hands avoided triggering US reporting and PFIC issues)

- $900K in a joint non-registered investment account

- $700K Toronto principal residence (Sarah holds title alone; David is on the mortgage)

- Combined household: ~$4M

If Sarah dies first.

Sarah’s TFSA, principal residence, and her share of the joint investment account become part of her estate. The principal residence qualifies for the Canadian principal residence exemption and passes to David tax-free for Canadian purposes. The TFSA, with David named as successor holder, rolls over without triggering its deemed disposition — though TFSA contribution room going forward is lost. Sarah’s share of the joint investment account passes to David at adjusted cost base.

David, as a US citizen, must now address all of these inherited assets through US tax filings. The TFSA loses any tax-free status from the US perspective the moment David becomes the holder — the family had been carefully avoiding this exposure by keeping the TFSA in Sarah’s name, and that protection ends at her death. The principal residence, even though Canadian, is subject to US tax on any gain over the Section 121 exclusion. The standard exclusion is $250,000 USD for a single filer. Critically, if David sells the home within two years of Sarah’s death and has not remarried, IRC §121(b)(4) lets him claim the full $500,000 USD joint exclusion as a single filer — provided the couple met the joint-return ownership and use tests immediately before Sarah’s death. Without preparation, David could find himself with US tax due on the inherited principal residence even though Canada exempts it entirely.

If David dies first.

David’s RRSP rolls over to Sarah on a tax-deferred basis under spousal rollover. The TFSA continues in Sarah’s name. The principal residence stays in Sarah’s name. The joint investment account passes to Sarah at adjusted cost base.

The complication is the US estate tax filing on David’s worldwide assets. David’s effective interest in the household is below the $15M federal exemption, so no US estate tax is owed at his death — but the size of his estate (his RRSP, his share of the joint investments, his share of the residence value, and any US-sited property he held) must be reported on Form 706 within nine months of death. If David held any US-sited assets — for example, a vacation property in Arizona — those assets may face separate US estate tax considerations even when the worldwide estate is below the exemption.

Without a QDOT in place, if David’s worldwide estate ever exceeds $15M and Sarah remains a non-US citizen, the estate above the exemption faces US estate tax at first death. With a QDOT, the tax is deferred until Sarah’s death.

The numbers in this example sit well below the QDOT threshold. The reporting obligations, beneficiary structures, and treaty elections are not optional anyway — they apply regardless of the estate size. The QDOT planning becomes critical at higher net worth; the rest of the planning becomes critical the day the couple’s documents are first prepared.

Frequently asked questions

Does the unlimited marital deduction apply if my spouse is a Canadian citizen?

No. The US unlimited marital deduction applies only when the surviving spouse is a US citizen. If your spouse is a Canadian citizen and not also a US citizen, assets transferred to them at your death may be subject to US estate tax above the $15 million USD federal exemption. The annual gift exclusion for transfers to a non-US citizen spouse during life is $194,000 USD for 2026, indexed annually.

What is a QDOT trust and when do you need one?

A Qualified Domestic Trust defers US estate tax on assets passing to a non-US citizen surviving spouse. The trust must have at least one US trustee with the right to withhold estate tax on principal distributions. QDOTs are typically used when a US citizen dies leaving assets to a non-citizen Canadian spouse and the estate exceeds the federal exemption.

Should my Canadian spouse become a US citizen for estate planning purposes?

Naturalization solves the marital deduction problem but has other consequences. The new US citizen becomes subject to worldwide US income taxation, FBAR and FATCA reporting, and PFIC rules on Canadian investment accounts. Whether the trade is worth it depends on the size of the estate, the spouse’s income, and how much Canadian-source income they have. It is rarely a small decision.

Are our joint Canadian bank accounts a problem if I am a US citizen and my spouse is Canadian?

Yes, in two ways. The US citizen spouse must report the entire joint account on FBAR if total foreign accounts exceed $10,000 USD at any point in the year, and on Form 8938 if FATCA thresholds are exceeded. If the Canadian spouse contributes most of the funds to a joint account, the IRS may also treat that as a gift to the US spouse, though this is rarely a tax issue at typical levels.

Can my Canadian spouse hold a TFSA, RESP, or FHSA without triggering my US tax obligations?

Yes — these registered accounts should generally be held in the Canadian spouse’s name only. TFSAs are not recognized as tax-deferred by the IRS and may be classified as foreign trusts if the US citizen spouse has any beneficial interest. RESPs face similar issues. Keeping these in the Canadian spouse’s name only avoids triggering US tax and reporting on the US citizen spouse.

What happens to RRSPs when a Canadian dies and leaves them to a US citizen spouse?

The RRSP balance is fully taxable on the deceased’s final Canadian return unless it passes to a qualifying spouse via spousal rollover. If the surviving US citizen spouse claims the rollover, the account remains tax-deferred for Canadian purposes, and the US views it as ongoing tax-deferred under the Canada-US Tax Treaty if a treaty election is filed annually. Without that election, growth is taxed currently in the US.

Do mixed-citizenship couples need separate wills for each country?

For most mixed-citizenship couples with assets in both countries, jurisdiction-specific wills (one Canadian, one US) per spouse is the cleanest approach. The wills must coordinate so they do not conflict or accidentally revoke each other. Powers of attorney also typically need to be jurisdiction-specific because a US-state POA may not be recognized in a Canadian province.

Should we name each other as RRSP or IRA beneficiaries directly?

Direct beneficiary designations are usually optimal but require treaty handling. RRSP held by the Canadian spouse with US citizen survivor: direct designation enables spousal rollover but requires annual US treaty election. IRA held by the US citizen spouse with Canadian survivor: 15% withholding tax applies on distributions; the inherited IRA can remain tax-deferred under the treaty if managed correctly.

What happens to the marital deduction when both spouses become US citizens?

If both spouses are US citizens at the time of the first death, the unlimited marital deduction applies to all assets passing to the surviving spouse. This is one reason some Canadian spouses choose naturalization specifically for estate planning purposes — though the US income tax and reporting consequences must be weighed against the estate tax benefit.

Get a coordinated estate plan for your situation

Mixed-citizenship marriage doesn’t make estate planning impossible. It makes it specific. The work has to be done in coordination with cross-border tax planning, with both spouses’ citizenship and residency status accounted for, and with the actual numbers in your household — not industry rules of thumb that assume both spouses share a passport.

This article describes the general framework cross-border families face. Your specific plan depends on your assets, your residency, your citizenship history, your beneficiaries, your domicile state if you spend time in the US, and the law of the province in which you reside. Information here is not a substitute for individual cross-border legal and tax advice.

If you would like to walk through your situation with a dual-licensed cross-border advisor, book a complimentary consultation with Lucas Wennersten at 49th Parallel Wealth Management.