Retiring in Canada as an American: Social Security, RRSPs, RMDs, and Getting the Income Right

By Lucas Wennersten, CFP® (US & Canada), CFA Founder, 49th Parallel Wealth Management | Published: May 2026 Reading time: ~10 minutes · ~2,200 words |

Your income sources don’t stop at the border — but the tax rules that govern them change entirely. A plain-language guide to Social Security, RRIF decumulation, US RMDs, the Roth IRA advantage, currency risk, and the optimal income sequence for American retirees in Canada.

IMPORTANT NOTE This article is for informational and educational purposes only. It does not constitute financial, tax, or investment advice. Rules for Social Security, RRSPs, RRIFs, US RMDs, and the Canada-US Tax Treaty are subject to change. Individual circumstances vary significantly. Always work with a qualified cross-border financial advisor and tax specialist before making retirement income decisions. 49th Parallel Wealth Management is registered as an investment adviser in the United States. |

FREE DOWNLOAD The American’s 2026 Canada Relocation Checklist Includes the retirement planning section: pre-move Roth conversion window, RRIF setup, RMD coordination, Social Security claiming, and Medicare decisions. Free download: 49thparallelwealthmanagement.com/american-canada-relocation-checklist |

AMERICANS IN CANADA — COMPANION SERIES Part 1: How Long Can an American Stay in Canada? Part 2: What Does Canada Actually Cost an American? Part 3: The Tax Reality No One Tells Americans Moving to Canada Part 4: What Nobody Tells Americans Before Their First Full Year Part 5: So You Want to Make It Official Deep-Dive: Healthcare Coverage for Americans Moving to Canada Deep-Dive: Buying Property in Canada as an American Deep-Dive: Retiring in Canada as an American — this post |

Retiring to Canada as an American is one of the most financially complex transitions a person can make. Not because the income sources change — your Social Security still pays, your IRA still exists, your pension still deposits — but because every one of them is governed by a different set of rules once you cross the border.

The Canada-US Tax Treaty coordinates the two systems and prevents most double taxation. But the coordination is not automatic. It requires elections, annual filings, sequencing decisions, and account structure choices that work very differently in retirement than during your working years. Made right, these decisions can significantly reduce your combined lifetime tax burden. Made wrong, they create compounding overpayments that are difficult to reverse.

This guide covers the retirement-specific planning layer that most Americans do not encounter until they are already in Canada and the first filing season has arrived.

Social Security in Canada: The Treaty Treatment

This is the first thing most Americans want to know when they consider retiring to Canada: what happens to their Social Security?

Under the Canada-US Tax Treaty, US Social Security benefits received by a Canadian resident are taxed only in Canada — not by the IRS. Canada includes 85 percent of your Social Security benefit in your Canadian taxable income, consistent with how Canada treats CPP and OAS. You receive the full deposit and pay Canadian income tax on 85 percent of it at your marginal rate.

For most American retirees in Canada, this is a favorable outcome. The 15 percent that is excluded provides a modest effective exemption, and for those in lower Canadian tax brackets — particularly in early retirement before RMDs begin — the effective rate on Social Security can be meaningfully lower than under full US taxation.

Does the Treaty Treatment Affect When You Should Claim?

The Spousal Coordination Dimension

If you have a Canadian spouse receiving CPP and OAS, coordinating Social Security timing with RRIF drawdown and pension income splitting can smooth household income across the two accounts more efficiently than optimizing each independently. This is a household-level planning exercise, not an individual one.

RRSP and RRIF: Decumulation for Americans

Americans who accumulated RRSP savings during their working years in Canada now face the decumulation question: how and when to draw those funds down in a way that minimizes combined Canadian and US tax.

The RRSP to RRIF Conversion

Your RRSP must be converted to a RRIF by December 31 of the year you turn 71. You can convert earlier if you choose. Once converted, mandatory minimum withdrawals begin the following year — the conversion year itself has no mandatory withdrawal.

The minimum withdrawal percentage is applied to your RRIF balance on January 1 of each year:

| Age | Min. Rate | On $500K Balance | On $1M Balance |

| 71 | 5.28% | $26,400 | $52,800 |

| 72 | 5.40% | $27,000 | $54,000 |

| 75 | 5.82% | $29,100 | $58,200 |

| 80 | 6.82% | $34,100 | $68,200 |

| 85 | 8.51% | $42,550 | $85,100 |

| 90 | 11.92% | $59,600 | $119,200 |

| 95+ | 20.00% | $100,000 | $200,000 |

The OAS Clawback Problem

RRIF minimums are added to your Canadian taxable income. If total income — RRIF withdrawals, Social Security at 85 percent inclusion, CPP, OAS, and other income — exceeds approximately $93,208 in 2026, your OAS benefit is reduced by 15 cents per dollar above that threshold. At approximately $151,668 in net income, OAS is fully clawed back.

American retirees with a substantial RRIF balance and US income can easily cross this threshold even without needing the extra cash. Strategies include: converting RRSP to RRIF earlier to draw it down before Social Security begins; using spousal pension income splitting to spread RRIF income; and timing Social Security deferral to smooth income across the years when RRIF minimums accelerate.

CONSIDER EARLY VOLUNTARY DRAWDOWNAmericans retiring to Canada in their mid-to-late 60s — before US RMDs begin at 73 and before RRIF conversion is mandatory at 71 — have a window where income may be lower than it will be once mandatory distributions from both systems run simultaneously. Drawing down RRSP/RRIF voluntarily in this window reduces future mandatory minimums, prevents OAS clawback, and may create room for Roth conversions at lower combined rates. Model this window explicitly before you reach 71. |

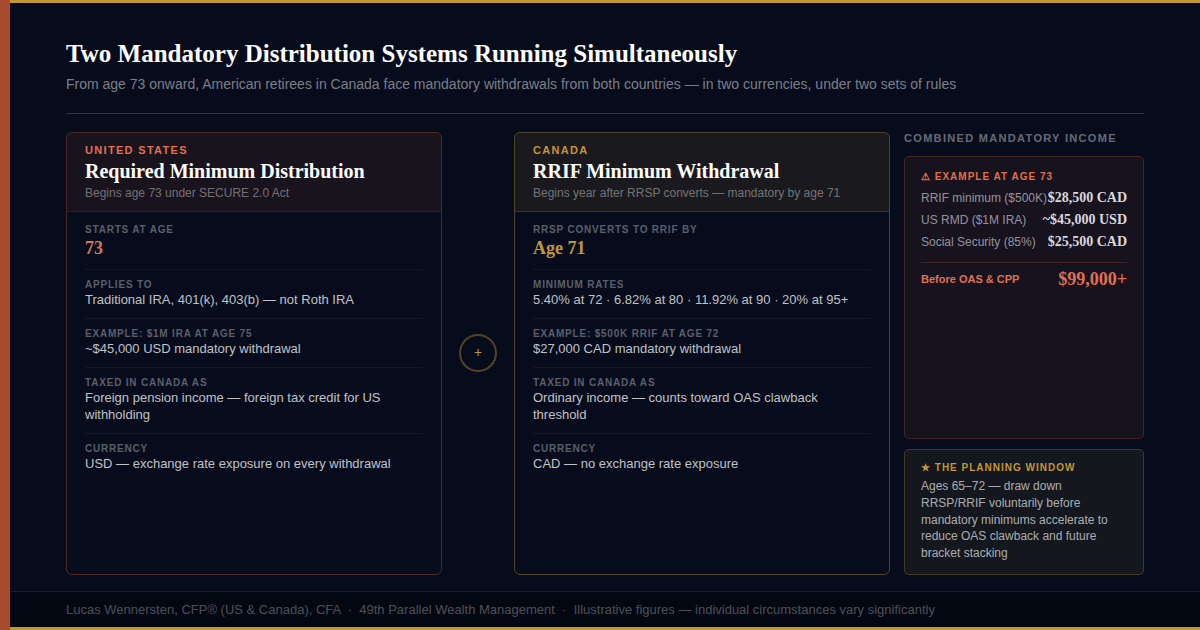

US RMD starting at age 73 versus Canadian RRIF minimum starting at age 72 — two mandatory distribution systems running simultaneously for American retirees in Canada with combined income examples |

US Required Minimum Distributions: They Don’t Stop at the Border

Required Minimum Distributions from US IRAs and 401(k)s begin at age 73 under the SECURE 2.0 Act and continue every year regardless of where you live. Moving to Canada does not pause, suspend, or alter US RMD obligations. From age 73 onward you will take your RMD from your US accounts and your Canadian RRIF minimum — both, every year, simultaneously.

How RMDs Are Taxed in Canada

Under the Canada-US Tax Treaty, traditional IRA and 401(k) distributions — including RMDs — are recognised as pension income. Withdrawals are taxable in Canada as foreign pension income, and you receive a foreign tax credit for any US withholding tax deducted at source. The standard non-resident withholding rate on IRA distributions is 30% gross, reduced to 15% under the treaty for periodic payments. The foreign tax credit prevents double taxation, but both the Canadian T1 and US return require careful reporting to apply the credit correctly.

The Two-System Mandatory Income Problem

A retiree with a $500,000 RRIF at age 73 (generating ~$28,500 in minimums) and a $1,000,000 US IRA (generating ~$45,000 in RMDs) faces over $73,500 in mandatory income before Social Security, OAS, CPP, or any investment income. That level typically triggers OAS clawback and pushes marginal rates on additional RRIF withdrawals well above what proactive early drawdown would have produced.

The window between retirement and the start of mandatory distributions from both systems — typically ages 65 to 72 — is the most important planning horizon for American retirees in Canada. What you do with it determines the tax efficiency of the following 25+ years.

The Roth IRA in Canadian Retirement: Your Most Valuable Account

Of all the accounts an American retiree in Canada can hold, the Roth IRA is the most valuable — and the one most at risk of being inadvertently damaged by a missed filing.

Under the Canada-US Tax Treaty, qualified Roth IRA withdrawals are tax-free in Canada, the same as they are in the United States. No US tax. No Canadian tax. This is the only account that provides this treatment in both countries simultaneously.

THE ROTH IRA ELECTION — FILE IN YEAR ONETreaty protection for your Roth IRA is not automatic. You must file a specific election with the CRA in the year you become a Canadian tax resident. This election is part of your Canadian T1 return. If you miss it in year one, the CRA can treat income and gains inside your Roth IRA as fully taxable in Canada for all subsequent years. If you have already been a Canadian resident and have not confirmed this election was filed, address it immediately with a cross-border tax specialist. |

Why the Roth IRA Is Particularly Valuable for Retirees in Canada

In Canadian retirement, most income is taxable: RRIF withdrawals, RMDs, Social Security at 85 percent inclusion, CPP, OAS. The Roth IRA is the exception. Withdrawals do not add to Canadian taxable income, do not contribute to OAS clawback, and do not affect income-tested benefits. For retirees managing the clawback threshold, the Roth provides a source of tax-free income that does not count against you.

The Roth IRA has no RMDs during the owner’s lifetime. You can hold it as long as you live and draw from it only when tax-efficient to do so — filling income in low-bracket years without triggering clawback or pushing into a higher rate.

Currency Risk in a Fixed-Income Retirement

During your working years, currency exposure is a nuisance. In retirement, when income is relatively fixed and spending is ongoing, it becomes a structural feature of your financial life that requires active management.

If your retirement income is primarily in US dollars — Social Security, IRA/401(k) distributions, US pension — but your expenses are in Canadian dollars, the CAD/USD exchange rate affects your real purchasing power every month. A 10 percent weakening of the USD is effectively a 10 percent reduction in Canadian spending capacity from those income sources. Over a 20 to 30 year retirement, sustained moves of this magnitude are not unusual.

Managing Currency Exposure in Retirement

- Currency alignment, not constant conversion — hold CAD for Canadian expenses and USD for US obligations. Convert in larger amounts deliberately rather than continuously at bank rates carrying a 2–3 percent spread.

- Use Norbert’s Gambit for large conversions — buying a security listed in both currencies, journaling it, and selling in the target currency converts at the bid-ask spread rather than the bank retail rate. Savings of 1.5–2.5 percent on large amounts are typical.

- Model your currency break-even — at what CAD/USD rate does your income become insufficient for Canadian expenses? Build explicit buffers. A rate comfortable at 1.35 may be strained at 1.15.

- Social Security deferral adds currency buffer — a larger monthly benefit from deferring to 70 provides more cushion against USD weakness than a smaller early benefit.

Optimal income sequencing for American retirees in Canada — taxable accounts first, then RRSP/RRIF, RMDs, Social Security, and Roth IRA last Optimal income sequencing for American retirees in Canada — taxable accounts first, then RRSP/RRIF, RMDs, Social Security, and Roth IRA last |

The Income Sequencing Framework

The sequence in which you draw from your accounts has a larger impact on lifetime after-tax income than almost any other decision. Here is the general framework:

| # | Source | Rationale | Timing |

| 1 | Taxable brokerage (CA & US) | Draw taxable first to allow registered and Roth to keep compounding. Capital gains may be at lower rates than ordinary income. | Ages 65–72 |

| 2 | RRSP/RRIF voluntary (above minimums) | Draw down voluntarily before mandatory minimums accelerate. Reduces future OAS clawback. Creates room for Roth conversions at lower rates. | Ages 65–71 |

| 3 | RRIF mandatory minimums | Non-discretionary from 72+. Coordinate with OAS clawback threshold. Use pension income splitting where possible. | Age 72+ mandatory |

| 4 | US Social Security | Defer to 70 if health allows. Taxed at 85% inclusion in Canada only. Larger benefit = more currency buffer. | Optimal: age 70 |

| 5 | US RMDs (IRA / 401k) | Non-discretionary from 73. Coordinate with RRIF minimums to manage combined mandatory income. | Age 73+ mandatory |

| 6 | Roth IRA | Draw last. Tax-free in both countries. No OAS clawback impact. No US RMDs. Use to fill income gaps in high-bracket years. | As needed / last |

THE PRE-RETIREMENT ROTH CONVERSION WINDOW If you are approaching retirement but have not yet moved to Canada or begun mandatory distributions, you may have a window for Roth conversions at relatively low US tax rates. Converting traditional IRA balances to Roth before Canadian residency and before mandatory distributions begin reduces future RMDs, reduces future Canadian taxable income, and builds a larger tax-free Roth balance. This is one of the highest-value planning decisions available to Americans on the path to Canadian retirement. |

Healthcare in Retirement: The Cross-Border Layer

Healthcare planning in retirement has its own cross-border dimensions. The full coverage framework is in our healthcare deep-dive. The retirement-specific highlights:

- Medicare Part B decision — the permanent 10% per year disenrolment penalty is more consequential for retirees than working-age adults. Most retirees in Canada keep Part A and carefully evaluate Part B based on US travel expectations and any possibility of returning.

- Long-term care planning — Canadian provincial health does not fully cover long-term residential care. Ontario residents in long-term care pay $62 to $110 CAD per day depending on room type. US long-term care insurance policies typically do not cover Canadian facilities. Retirement income projections must account for long-term care costs explicitly.

- Provincial health presence requirements — most provinces require physical presence for a minimum of days per year to maintain coverage. OHIP requires 153 days in Ontario per 12-month period. For retirees splitting time between Canada and the US, this adds a third day-count constraint alongside the VHT six-month rule and the US Substantial Presence Test.

The Bottom Line

Retiring to Canada as an American is entirely achievable — and for many people, deeply rewarding. But the financial complexity is real. The two mandatory distribution systems running simultaneously from age 72 onward, the OAS clawback that penalises large combined incomes, the Roth IRA election that must be filed in year one, and the currency exposure that runs through every dollar of US-denominated income: these are not afterthoughts. They are the architecture of your retirement.

The good news is that the window before mandatory distributions begin is genuinely powerful. Managed well, the years between retirement and age 72 can significantly reduce the tax burden of the years that follow. That window is where the most valuable planning happens.

If you are an American approaching retirement and considering Canada, or already in Canada and managing an income structure that feels more complex than it should, book a complimentary consultation with our team. From the Desert to the Tundra™, we work across both systems so you don’t have to choose between them.

Frequently Asked Questions

Can I collect US Social Security if I retire in Canada?

Yes. Social Security is payable regardless of where you live. Under the Canada-US Tax Treaty, benefits received by a Canadian resident are taxed only in Canada — not by the IRS. Canada includes 85 percent of the benefit in your taxable income. Payments can be deposited directly to a Canadian bank account.

How is US Social Security taxed in Canada?

Under the treaty, Social Security received by a Canadian resident is taxed only in Canada. Canada includes 85 percent of the benefit in your taxable income, consistent with how it treats CPP and OAS. The effective rate depends on your total income picture.

When must I convert my RRSP to a RRIF?

By December 31 of the year you turn 71. No mandatory withdrawal is required in the conversion year. Minimums begin the following year, starting at approximately 5.28 percent of the account balance at age 71 and rising to 20 percent at age 95 and older. The minimum is calculated on the January 1 balance each year.

Do US Required Minimum Distributions still apply if I live in Canada?

Yes. US RMDs from IRAs and 401(k)s begin at age 73 under the SECURE 2.0 Act and continue regardless of where you live. Moving to Canada does not alter this obligation. RMD withdrawals are taxable in Canada as foreign pension income with foreign tax credit coordination to prevent double taxation.

How is my Roth IRA treated when I retire in Canada?

Under the Canada-US Tax Treaty, qualified Roth IRA withdrawals are tax-free in Canada — the same as in the US. However, treaty protection is not automatic. You must file a specific election with the CRA in the year you become a Canadian resident. Missing this election in year one means the CRA can treat Roth IRA income as fully taxable.

What is the optimal income sequence for American retirees in Canada?

The general framework: draw taxable brokerage accounts first, then RRSP/RRIF voluntarily before mandatory minimums, then RRIF mandatory minimums from 72, coordinate Social Security timing, take US RMDs as required from 73, and draw Roth IRA last as it is tax-free in both countries with no US RMDs. The right sequence for your situation depends on account balances, income levels, and full circumstances.

How does the OAS clawback affect American retirees in Canada?

OAS benefits are reduced by 15 cents per dollar of net income above approximately $93,208 in 2026. RRIF withdrawals, Social Security at 85 percent inclusion, and US RMDs all count toward this threshold. American retirees with significant US income often need to plan RRIF timing carefully to avoid or minimise OAS clawback.

How does currency risk affect retirement income as an American in Canada?

If your income is primarily in US dollars but expenses are in Canadian dollars, the CAD/USD rate affects your real purchasing power every month. A 10 percent weakening of the USD reduces effective Canadian spending power from USD income by 10 percent. Currency alignment, deliberate large-amount conversions, and modelling the exchange rate break-even are key retirement planning steps.

Should I claim Social Security before or after moving to Canada?

The optimal claiming age depends on health, longevity, other income, and spousal coordination — not country of residence. However, deferring to 70 produces a larger monthly benefit that provides more currency buffer if the USD weakens against CAD over your retirement.

What happens to my Medicare when I retire to Canada?

Medicare does not cover healthcare received in Canada. Most retirees keep Part A (no premium for most). Part B costs $185 USD per month in 2025 with no Canadian coverage. Disenrolling from Part B creates a permanent 10 percent annual surcharge on re-enrolment. See our healthcare deep-dive for the full Medicare decision framework.

0 thoughts on “Retiring in Canada as an American: Social Security, RRSPs, RMDs, and Getting the Income Right”

Pingback: Roth IRA for Canadians: How to Keep Your Account Tax-Free After Moving North - Crossing the 49th Parallel