The $15M Estate Tax Exemption Under the Big Beautiful Bill: What It Means for US Citizens in Canada

By : Lucas Wennersten, CFP® (US & Canada), CFA · 49th Parallel Wealth Management · Reading time: ~10 minutes

DISCLAIMER · This article describes US and Canadian tax provisions current at the time of writing. The Big Beautiful Bill provisions discussed are based on the version signed in 2025; subsequent guidance from Treasury, IRS, and CRA may refine application details. This is general information, not personalized tax, legal, or financial advice. Your specific situation depends on your assets, residency, citizenship history, and the law of your province or state. Consult a cross-border tax attorney and dual-licensed financial advisor before acting on any of the strategies described.

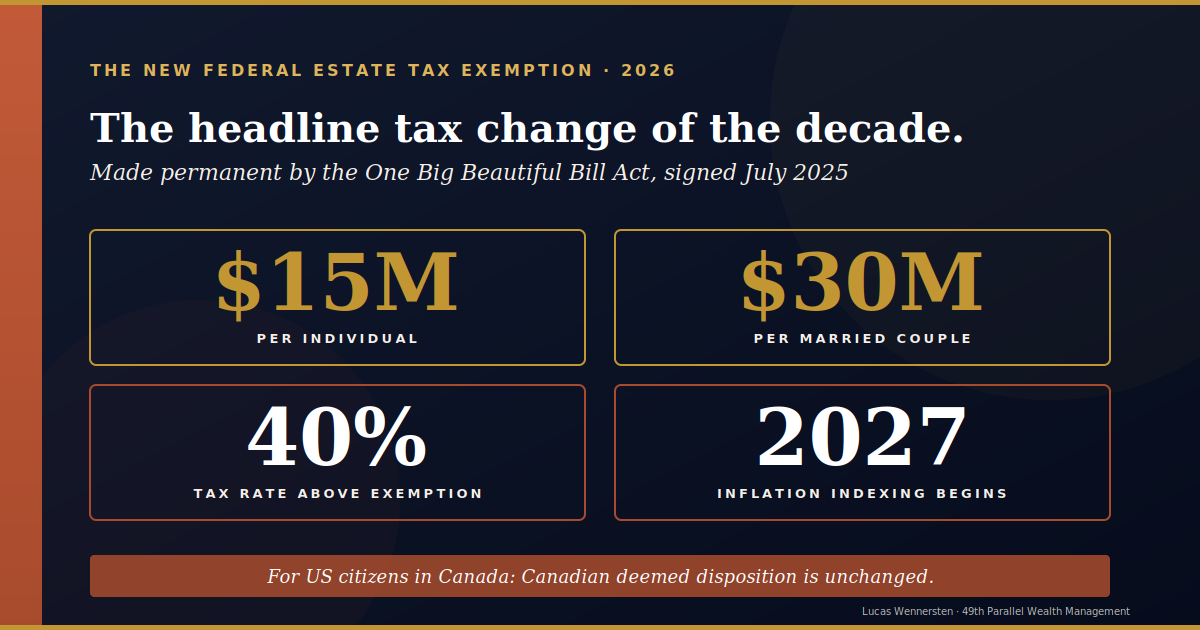

In 2025, Congress made the federal estate tax exemption permanent at $15 million per individual. For most Americans, that’s the headline tax change of the decade. For Americans living in Canada, it’s only half the story.

The One Big Beautiful Bill Act, signed in 2025, did three structural things to US estate tax: it locked the exemption at $15 million per individual starting in 2026, indexed for inflation; it matched the Generation-Skipping Transfer (GST) exemption to the same threshold; and it cancelled the scheduled 2025 sunset that would have dropped the exemption back to about $7 million.

For US citizens resident in Canada — by passport, by birth, or by descent — these changes are real wins. They also miss the part of the tax problem Congress couldn’t touch. The Canadian deemed disposition rule, which treats most assets as if you sold them on the day you die, is unchanged. The two countries don’t recognize each other’s exemptions. The same assets are still taxed in mechanism, if not always in dollars.

This article is for US citizens resident in Canada whose worldwide estate is approaching or above the federal exemption. It walks through how cross-border estate planning works when one side of the equation just shifted, what BBB changed, what it didn’t, and the planning moves to consider before December 2026.

The Big Beautiful Bill estate provisions: a plain-language summary

$15 million — the new permanent federal estate tax exemption per individual under the Big Beautiful Bill from 2026

$15 million — the new permanent federal estate tax exemption per individual under the Big Beautiful Bill from 2026

Three structural changes are worth understanding individually.

$15M exemption permanent. The federal estate tax exemption — the amount each individual can pass to non-spouse beneficiaries without owing US estate tax — was scheduled to drop from $13.99 million in 2025 back to roughly $7 million in 2026 when the 2017 Tax Cuts and Jobs Act provisions sunset. The Big Beautiful Bill kept it from dropping. Starting January 1, 2026, the exemption is $15 million per individual, indexed annually for inflation (IRS Estate and Gift Tax FAQs). There is no scheduled sunset under current law, though Congress can change the threshold in future legislation. For a married couple with proper portability planning, the combined exemption is $30 million.

GST exemption matched. The Generation-Skipping Transfer tax — the second layer of US estate tax, which applies when wealth skips a generation by going directly to grandchildren — was raised in lockstep. The GST exemption is also $15 million per individual for 2026. For families using trusts to skip generations, this means $30 million per couple can flow to grandchildren without GST tax. Unlike the regular estate exemption, there is no portability of the GST exemption between spouses, so allocation strategy matters.

Annual gift exclusion held. The annual gift tax exclusion — what each individual can give per recipient per year without using lifetime exemption — remains at $19,000 USD for 2026, unchanged from 2025. The annual exclusion for gifts to a non-US-citizen spouse, however, increased: $194,000 for 2026, up from $190,000 in 2025 (per IRS Rev. Proc. 2025-32). This figure is indexed annually and is a strategic planning lever for cross-border couples specifically.

For couples with combined estates under $30 million USD, the federal estate tax is no longer a binding constraint. The exemption alone shelters most or all of the estate. For high-asset clients above that threshold, the BBB changes the math — but it doesn’t remove the need for sophisticated planning. For US citizens resident in Canada, the calculation is different again — because BBB only addresses the US side. For broader 2026 cross-border tax updates, see tax changes US Canada 2026.

Why $15M doesn’t solve the problem for US citizens in Canada

The US estate tax exemption is generous. The Canadian estate tax doesn’t exist. So in headline terms, US citizens in Canada appear to be in an excellent spot — both countries’ laws favor them.

The reality is more nuanced because Canada uses a different mechanism: deemed disposition.

Under Canadian Income Tax Act Section 70(5), most assets are treated as if you sold them at fair market value on the day you died. Capital gains on the appreciation are taxed on the deceased’s final Canadian return. There is no Canadian federal estate tax — but there is substantial capital gains tax on appreciated assets, and it can apply to property well below any US estate tax threshold. The mechanism is different. The result, for an appreciated asset, is similar.

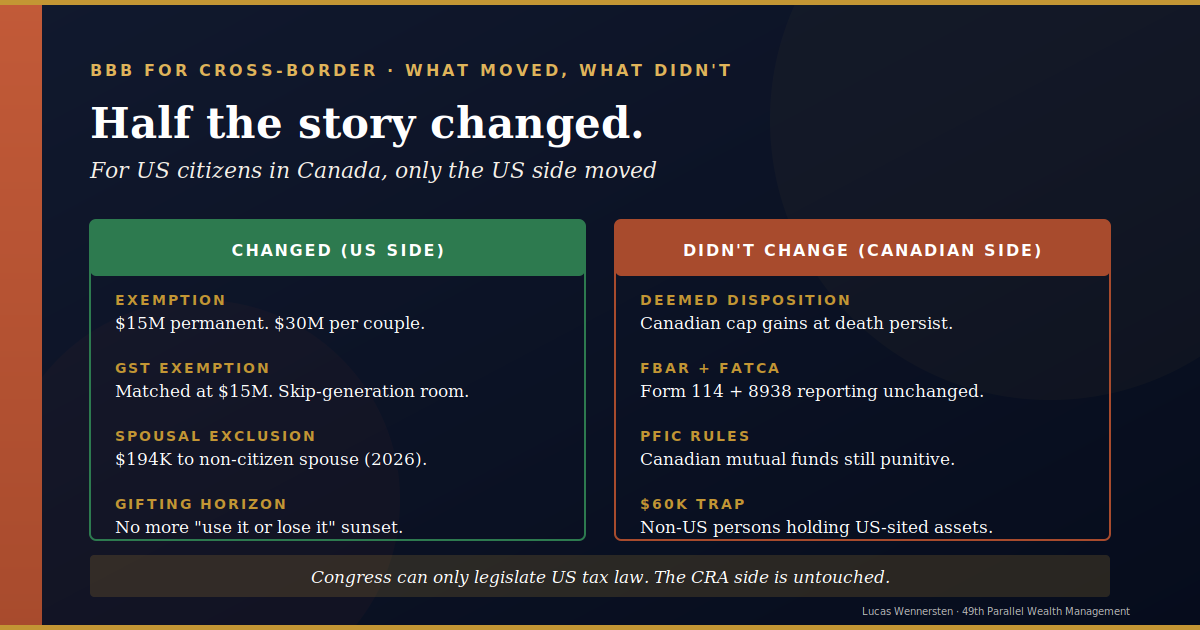

The BBB doesn’t change Canadian deemed disposition. It can’t. Congress only legislates US tax law. The CRA continues to apply deemed disposition based on its own rules, and US citizens who are Canadian residents are subject to it. Two consequences worth understanding follow.

First, the same assets are still taxed twice in mechanism. A US citizen resident in Canada faces Canadian deemed disposition on Canadian-side appreciated assets at death AND must report the worldwide estate on IRS Form 706 within nine months. The US estate tax may be zero (because of the $15M exemption), but the form must still be filed and the assets must still be valued. Tax preparation costs and administrative burden don’t vanish just because no estate tax is owed.

Second, the two countries don’t recognize each other’s exemptions. The $15M US exemption protects against US estate tax. It does not reduce Canadian deemed disposition tax. The Canada-United States Tax Convention provides limited treaty relief — primarily a US estate tax credit for Canadian estate tax paid (Article XXIX-B) — but this is a credit against US tax, not against Canadian tax. For Canadian-side capital gains owed at death, no comparable credit exists.

The practical implication: a US citizen in Canada with a $5 million estate above pre-acquisition cost basis still owes substantial Canadian capital gains at death, regardless of what BBB did with the US exemption. The threshold concern in cross-border estate planning isn’t ‘do I face US estate tax?’ — for most Canadian-resident US citizens, it’s now no. The question that matters is ‘do I face Canadian deemed disposition tax, and how do I manage it?’ That answer is unchanged.

What changed for the Canadian-resident-US-citizen specifically

While Canadian deemed disposition is unchanged, the BBB does shift the planning calculus for US citizens in Canada in four meaningful ways.

Lifetime gifting strategy expands. With the federal exemption locked at $15 million, the planning concern of ‘gift now to capture the exemption before it drops’ is gone. Gifts to non-US-citizen spouses are still capped at the annual exclusion ($194,000 USD for 2026) — that didn’t change. But gifts to children, grandchildren, and other beneficiaries can now be planned over a longer time horizon. The strategic question shifts from ‘use it or lose it’ to ‘gift to remove future appreciation from the taxable estate.’

GST exemption opportunities widen. The matched $15 million GST exemption is significant for cross-border families using trusts to provide for grandchildren. Skipping a generation can now move $30 million per couple without GST tax. Allocating GST exemption efficiently requires deliberate choice — there’s no portability — so the timing of allocations matters. For families with appreciated Canadian assets they want to pass through trust structures, GST allocation strategy is one of the highest-leverage decisions available post-BBB.

ILIT funding strategies recalibrate. An Irrevocable Life Insurance Trust holds life insurance outside the taxable estate, providing tax-free death benefit. Before BBB, ILITs were widely used by US citizens with estates above the (then-lower) exemption to provide US estate tax liquidity. With $15M exemption permanent, fewer estates face federal estate tax, and ILIT funding decisions should be re-examined. ILITs remain useful for liquidity (paying Canadian deemed disposition tax, providing wealth transfer to non-citizen spouses, equalizing inheritance for children with different residency status) — but they’re no longer essential for many estates that previously needed them. Premium reduction or partial unwinding deserves a conversation with the original advisor.

Trust structures designed for lower exemption thresholds may need restructuring. Plans drafted assuming the 2025 sunset may now be over-engineered. Bypass trusts and other estate-tax-minimization structures can lock up assets unnecessarily. For some clients, simplification — including unwinding QDOT structures or revising spousal trusts — is now possible. Any plan written between 2018 and 2025 deserves a fresh look against the permanent $15M exemption. The most expensive estate plan is the one that solves yesterday’s problem.

What hasn’t shifted: the obligation to report worldwide assets to the IRS via Form 706 (when above filing thresholds), to comply with FBAR and FATCA reporting on Canadian accounts, and to navigate PFIC rules on Canadian mutual funds and ETFs. These remain part of every Canadian-resident US citizen’s tax life, regardless of estate size.

Five planning moves to consider before December 2026

Five planning moves for US citizens in Canada to consider before December 2026 after the Big Beautiful Bill

These are recommendations to consider with cross-border tax counsel as part of your overall Canada-US tax strategy — not personalized advice. Each requires individual analysis based on your assets, residency, and family situation.

- Review your existing estate plan against the higher exemption. If your plan was drafted under the lower exemption ($5-13M range), structures designed to minimize estate tax — bypass trusts, QTIP-QDOT combinations, complex multi-generational trust structures — may now be over-engineered. Your estate attorney can compare current trust structures against the $15M permanent exemption and identify simplification opportunities. Simplification reduces administration costs and inheritance complexity.

- Re-evaluate GST exemption allocation. If you have grandchildren or are considering generation-skipping transfers, the matched $15M GST exemption gives you more room to plan. Decisions about which assets to allocate GST exemption to (and via what trust structures) can have substantial long-term tax consequences across generations. The decision is largely once-per-allocation — you can’t easily reverse it once made — so this is an area where deliberation matters more than speed.

- Use lifetime gifting to a non-citizen Canadian spouse to manage future US exposure. If your spouse is a Canadian citizen, the $194,000 annual exclusion (2026) still applies. Strategic gifting can move appreciating assets to your Canadian spouse — outside your eventual US estate — over time. This is a multi-year strategy, but with the BBB extending the planning runway, the math now favors steady gifting over a forced single-year move. Pair this with a review of any QDOT structures that may no longer be necessary.

- Audit your ILIT. If you maintain an ILIT funded with substantial premiums for US estate tax liquidity, the math may have shifted. With the federal exemption permanent at $15M, you may be paying premiums to solve a problem that no longer fully exists. Whether to reduce premiums, fully fund a smaller benefit, or unwind the structure depends on Canadian-side liquidity needs and the specific terms of the trust. The question is worth a focused review with your insurance professional and estate attorney.

- Coordinate your Canadian and US wills around the new permanent exemption. Many cross-border families have jurisdiction-specific wills (one Canadian, one US, per spouse). The wills must coordinate — they can’t conflict, accidentally revoke each other, or assume different exemption thresholds. With the permanent $15M federal exemption, US wills drafted assuming a lower threshold should be reviewed. The same applies to powers of attorney and beneficiary designations. Ensure assumptions in the documents match the law that’s now actually in force.

These moves aren’t urgent in the regulatory sense — there’s no December 2026 statutory deadline tied to BBB. They’re urgent in the practical sense: estate plans drift over time, and the BBB created a moment to reset assumptions. Doing the review while the rule changes are recent is more efficient than catching up two years from now.

What the Big Beautiful Bill did NOT change

What the Big Beautiful Bill changed vs didn’t change for cross-border estate planning between Canada and the US

For US citizens in Canada, five things remain in force exactly as they were before BBB.

US worldwide income taxation. As a US citizen, you remain subject to US tax on your worldwide income, regardless of where you live. BBB addressed estate tax, not income tax for citizens.

FBAR and FATCA reporting. FinCEN Form 114 (FBAR) and IRS Form 8938 (FATCA) requirements are unchanged. Canadian financial accounts above the reporting thresholds must still be disclosed annually. From the Canadian side, CRA Form T1135 continues to require reporting of foreign property over CAD $100,000.

PFIC treatment. Canadian mutual funds and ETFs continue to be classified as Passive Foreign Investment Companies under IRS Form 8621 reporting. PFIC tax treatment — gains taxed at the highest US ordinary income rate plus an interest charge — remains punitive. Holding Canadian funds at all is a US tax decision; BBB didn’t change that calculus.

Canadian deemed disposition. Income Tax Act Section 70(5) applies as before. Canadian appreciation is taxed at death whether or not US estate tax is owed. The BBB has no effect on the Canadian side.

$60K nonresident exemption for US-sited assets. For non-US persons (not US citizens, not green card holders) holding US-sited property, the federal estate tax exemption is just $60,000 USD — unchanged by BBB. This affects Canadians (who are not also US citizens) who own US property: vacation homes, US stocks, US-located businesses. It does not affect US citizens, who get the full $15M exemption regardless of where they live or where the property is sited.

The BBB recalibrated US estate tax thresholds. It didn’t redesign the cross-border tax landscape. The structural complexities of dual-system planning persist.

Frequently asked questions

What is the new estate tax exemption under the Big Beautiful Bill?

The Big Beautiful Bill made the federal estate tax exemption permanent at $15 million USD per individual starting in 2026, indexed annually for inflation. Before this change, the exemption was scheduled to drop back to about $7 million USD when the 2017 Tax Cuts and Jobs Act provisions sunset. The Generation-Skipping Transfer (GST) tax exemption was also matched at $15 million.

Does the $15 million exemption apply to US citizens living in Canada?

Yes. The US taxes citizens on their worldwide estate regardless of where they live, and the same $15 million exemption applies. A US citizen who is a Canadian resident at death gets the full exemption against US estate tax. The catch is that Canada also taxes the estate through deemed disposition, and the two countries don’t recognize each other’s exemptions.

How does Canadian deemed disposition still affect a US citizen in Canada?

Canada does not have an estate tax, but the CRA treats most assets as if you sold them on the day you died, triggering capital gains on any appreciation under Income Tax Act Section 70(5). This applies to US citizens who are Canadian residents the same as it applies to anyone else. The US estate tax exemption does not reduce or offset the Canadian deemed disposition tax.

Did the Big Beautiful Bill change the GST tax exemption?

Yes. The GST tax exemption was raised in lockstep with the estate exemption to $15 million USD per individual starting in 2026, also indexed for inflation. This is significant for cross-border families using trusts to skip generations, because more wealth can pass to grandchildren without GST tax. Note that GST exemption is not portable between spouses — each individual’s exemption must be allocated separately.

Should I still consider lifetime gifting now that the exemption is permanent?

Yes. Lifetime gifting still removes future appreciation from your taxable estate, which can be valuable even with a high exemption. Gifts to a non-US-citizen spouse are still capped at the annual exclusion ($194,000 USD for 2026, indexed) — the unlimited marital deduction does not apply. Strategic gifting can also use up GST exemption efficiently and reduce future Canadian-side capital gains exposure on appreciating assets.

What did the Big Beautiful Bill NOT change for US citizens in Canada?

Five things to know: US worldwide income taxation for citizens is unchanged; FBAR and FATCA reporting requirements are unchanged; PFIC treatment of Canadian mutual funds and ETFs is unchanged; the Canadian deemed disposition at death is unchanged; and the $60,000 estate tax exemption for non-US persons holding US-sited assets is unchanged. The bill only changed exemption thresholds, not structural rules.

Do I need to update my estate plan because of the Big Beautiful Bill?

Probably yes if you are a US citizen with assets above $7-15 million USD. Plans drafted assuming the 2025 sunset may now be over-engineered for the higher permanent exemption. Trusts designed to use the lower exemption may need restructuring. Plans should also be reviewed if you live in Canada to ensure they coordinate with Canadian deemed disposition treatment.

How does the BBB affect ILIT planning for US citizens in Canada?

Irrevocable Life Insurance Trusts remain useful but the calculus shifts. If the $15 million exemption covers your federal estate, the ILIT’s role moves from avoiding US estate tax to providing liquidity for Canadian deemed disposition or to fund US estate tax on US-sited property held by a non-US-citizen spouse. The structure should be reviewed by a cross-border attorney.

When do the Big Beautiful Bill estate provisions take effect?

The $15 million exemption and matched GST exemption take effect for estates and gifts after January 1, 2026. The exemption is indexed for inflation in subsequent years. There is no scheduled sunset under current law, though Congress can change exemption thresholds in future legislation.

Get a coordinated cross-border estate review

The Big Beautiful Bill simplified the federal estate tax landscape for many US clients. For US citizens resident in Canada, it didn’t simplify the cross-border picture — it just changed the inputs. Your estate plan should reflect the actual rules in force, not the rules the planner assumed in 2017 or 2024.

This article describes the framework most Canadian-resident US citizens face. Your specific plan depends on your assets, your residency status, your spouse’s citizenship, your beneficiaries, and the law of your province. Information here is not a substitute for individual cross-border legal and tax advice.

If you would like to walk through your situation with a dual-licensed cross-border advisor, book a complimentary consultation with Lucas Wennersten at 49th Parallel Wealth Management.

About the author

Lucas Wennersten is the founder of 49th Parallel Wealth Management and a dual-certified financial planner (CFP® US & Canada) and Chartered Financial Analyst (CFA). With a career spanning Arizona and Toronto, Lucas brings firsthand experience navigating cross-border finances to every client relationship. He writes and speaks on wealth management, cross-border tax strategy, and retirement planning for Canadians and Americans living between two countries.