Concentrated Stock When You Move to Canada: The $5M Diversification Problem

By Lucas Wennersten, CFP® (US & Canada), CFA · 8-minute read

This article is general education, not personalized tax, legal, or financial advice. Cross-border rules around concentrated holdings are intricate, fact-specific, and change over time. Before acting on a large position, speak with a cross-border advisor about your situation.

It is one of the most common ways serious wealth is built and one of the most dangerous ways it is held: a single stock. A founder, a long-tenured executive, or a tech employee with years of equity vesting ends up with $5 million — or far more — concentrated in one company. The position carries two well-known risks. One is concentration: a single company’s stumble can erase a decade of saving. The other is the tax bill that diversifying would trigger, because selling a low-basis position can hand 20% to 35% of the gain to the tax authorities. Cross the border between Canada and the US, and a third dimension appears — one that can work dramatically for or against you, depending entirely on timing. Handled well, it belongs in your cross-border wealth management plan years before any sale.

Here is how the concentrated-stock problem actually changes when you move — and the levers that matter at this scale.

First, the good news: Canada hands you a fresh cost base

This is the single most important and least understood fact for anyone moving to Canada with appreciated stock. When you become a Canadian tax resident, Canada deems you to have acquired most of your property — including your shares — at fair market value on the day you arrive.

In plain terms, your Canadian cost base resets to the value on your move date. Canada does not tax the gain that accrued before you became a resident. If you bought (or vested) the stock at $1 and it is worth $200 the day you land, Canada treats your cost as $200 — and only taxes appreciation from there.

This is the deemed-acquisition rule, and it is set out for newcomers in the CRA’s guidance.

It means a brand-new Canadian resident often sits on a position with a huge US gain but almost no Canadian gain. That asymmetry is the foundation of nearly every smart move that follows. See the CRA’s Newcomers to Canada guidance, and Income Tax Folio S5-F1-C1 on exactly when residency — and the reset — begins.

Now the catch: if you are a US citizen, the basis does not reset for the IRS

Here is where it gets cross-border. The US taxes its citizens and green-card holders on worldwide income no matter where they live — citizenship-based taxation. Moving to Canada does nothing to reset your cost basis for US purposes. To the IRS, your basis is still the original $1.

So a US citizen who moves to Canada and later sells ends up with two different gains on the same shares: a small Canadian gain (measured from the bumped cost base) and a large US gain (measured from original cost). The Canada-United States Tax Convention and the foreign tax credit system exist to prevent true double taxation — but because the two gains are different sizes and can fall in different years, the credits do not always line up cleanly. Coordinating the two is the heart of the planning. For the US treatment of the gain itself, see IRS Topic No. 409, Capital Gains and Losses.

For a non-US citizen moving to Canada, the picture is far simpler: once you are a Canadian resident, the US generally does not tax your gains on publicly traded US stock at all, and Canada only taxes the post-arrival gain. That combination can be close to a clean slate.

The most powerful move is also the simplest: time the sale to the move

Because the Canadian cost base resets on arrival, the period right after you become a resident is often the best window to diversify on the Canadian side. Sell while the share price is still near your bumped cost base and the Canadian capital gain is small — sometimes negligible. Wait years, let the stock climb further, and you rebuild a Canadian gain you could have avoided.

For a non-US person, that is frequently the entire strategy: arrive, then diversify promptly. For a US citizen, the US gain is still waiting regardless, so the timing question becomes a coordination question — in which year do you realize, and how do the US and Canadian taxes and credits interact? That is a question for a deliberate Canada-US tax strategy, not a year-end scramble.

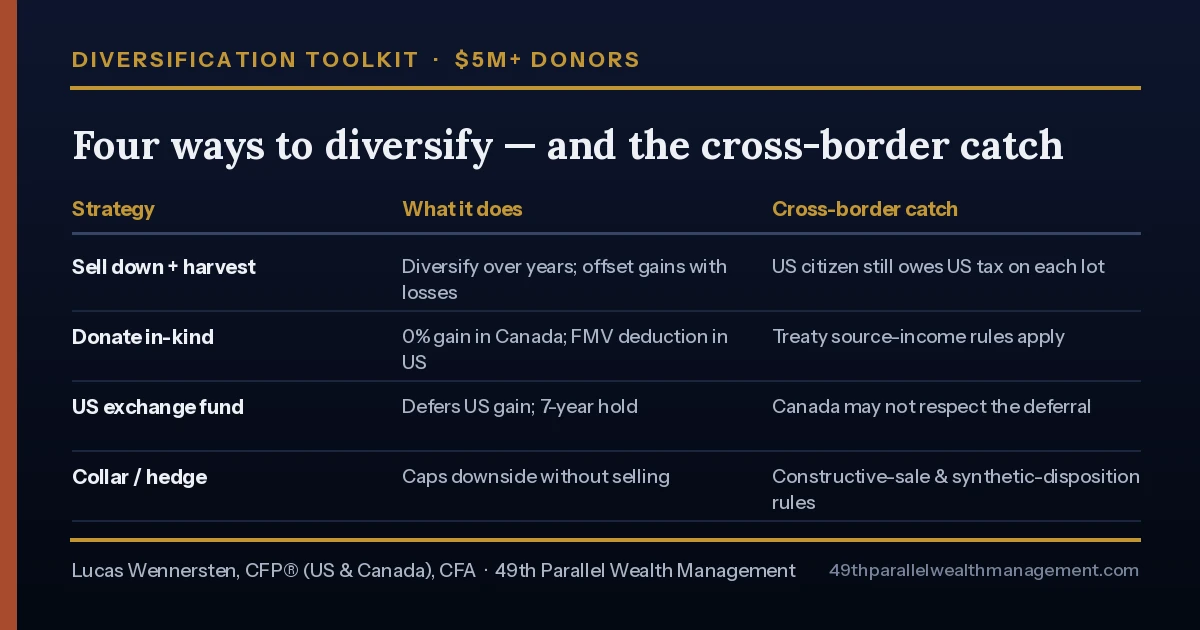

When you can’t just sell: the diversification toolkit

Sometimes selling all at once is not feasible — the position is too large, the tax too high in a single year, or there are lock-ups and insider constraints. Several tools can help, but each one travels across the border differently, and that is where most generic advice falls apart.

Sell down over time with a managed overlay. Diversifying gradually spreads the gain across tax years. Pairing it with a separately managed account that harvests losses elsewhere in the portfolio can offset some of the gain as you trim the position. Straightforward, liquid, and it works in both countries.

Donate appreciated shares. If you are charitably inclined, gifting the stock in-kind is often the most tax-efficient diversification of all on the Canadian side — the accrued gain is taxed at a 0% inclusion rate and you receive a full-value receipt. We cover the mechanics in our guide to donating appreciated securities across the border.

Exchange funds (a US tool). A US exchange fund lets you contribute concentrated shares for a diversified partnership interest and defer US capital gains, typically with a seven-year lock-up. The catch for cross-border families: this is a US deferral, and Canada will not necessarily respect it — for a Canadian resident, contributing shares can itself be treated as a disposition at fair market value, on top of K-1 reporting, foreign-property filing, and offshore-fund complications. Do not assume the US deferral survives the move; this one needs specific advice.

Collars and hedging. Options strategies — a costless collar, for example — can cap downside on a position without selling it. But both countries police this: the US constructive sale rules (IRS Publication 550) and Canada’s synthetic-disposition rules can deem the position sold for tax purposes if you hedge away too much of the risk. A hedge can buy time; it cannot quietly become a tax-free sale.

Borrow against the position. Securities-based lending lets you raise cash for diversification or spending without triggering a sale at all — useful as a bridge, though it adds leverage and rate risk that has to be managed inside the broader cross-border investment management plan.

Two wrinkles the wealthy should know

QSBS does not cross the border. US founders often count on the Section 1202 qualified small business stock exclusion to shelter a large chunk of gain. Canada has no equivalent and will not honour the US exclusion — a Canadian resident is taxed by Canada on that gain. The saving grace is the same cost-base reset above: Canada only taxes the post-arrival portion, so timing the move and the sale around each other matters enormously.

Shares of a Canadian company can be different. “Taxable Canadian property” — broadly, shares deriving most of their value from Canadian real estate, among other categories — is excluded from the arrival cost-base bump and follows its own rules. If your concentrated position is in a private Canadian company, do not assume the reset applies.

A pre-move checklist

If a concentrated position and a cross-border move are both on your horizon, work through:

- Establish your exact Canadian residency date — it sets the cost base for every share you hold.

- Document the fair market value of the position on that date — it is the number Canada will use.

- Know your US status — citizen, green-card holder, or neither changes the entire analysis.

- Decide the diversification window — selling early in Canadian residency often minimizes the Canadian gain.

- Coordinate the two tax systems — for US persons, model the US gain, the Canadian gain, and the foreign tax credits together, not separately.

- Pressure-test any US tool (exchange fund, QSBS, collar) for Canadian treatment before relying on it.

- Consider whether donating part of the position achieves diversification and a tax benefit at once.

The bottom line

A concentrated stock position is a cross-border planning problem disguised as an investment one. Canada hands newcomers a powerful gift — a reset cost base — that rewards acting early and punishes drift. The US, for its citizens, never lets go of the original basis, which makes coordination, not cleverness, the deciding factor. Get the timing and the structure right, and you can diversify a once-in-a-career position for a fraction of the tax a careless sale would cost. Get it wrong, and you pay twice for the privilege of doing it late.

Frequently asked questions

Does Canada tax the gain that built up on my stock before I moved?

Generally no. When you become a Canadian resident, you are deemed to acquire most property at fair market value on your arrival date, so Canada only taxes appreciation after you move. The gain that accrued before immigration is outside the Canadian net.

Do I get a step-up in cost basis when I become a Canadian resident?

For Canadian tax purposes, yes — your cost base resets to fair market value on the day you become a resident. This does not apply to the US side, and it does not apply to taxable Canadian property such as certain private-company or real-estate-heavy shares.

I am a US citizen — does moving to Canada lower my US tax on the stock?

No. The US taxes citizens and green-card holders on worldwide gains regardless of where they live, and your US cost basis stays at the original figure. Moving changes your Canadian treatment, not your US treatment.

When is the best time to sell after moving to Canada?

Often early in your Canadian residency, while the share price is still close to the reset cost base, so the Canadian gain is small. For US citizens the US gain remains, so the timing must be coordinated across both tax systems rather than driven by the Canadian side alone.

Can I use a US exchange fund to diversify as a Canadian resident?

Exchange funds defer US capital gains, but the deferral is a US concept that Canada may not respect. For a Canadian resident, contributing shares can itself be treated as a disposition, and the structure adds foreign reporting and offshore-fund complications. Get specific advice before assuming it works.

Can I hedge with a collar instead of selling?

You can use options to limit downside without selling, but both the US constructive-sale rules and Canada’s synthetic-disposition rules can deem the position sold if you hedge away too much risk. A collar can buy time; it is not a tax-free exit.

Does donating the shares help me diversify tax-efficiently?

Yes. Gifting appreciated shares in-kind to a registered charity eliminates the Canadian capital gain at a 0% inclusion rate and gives you a full-value receipt, which makes it one of the most efficient ways to trim a concentrated position if you are charitably inclined.

Is US qualified small business stock (Section 1202) recognized in Canada?

No. Canada has no equivalent to the Section 1202 gain exclusion and will tax the gain on its own terms. The cost-base reset on arrival is the main Canadian-side mitigant, which is why timing the move matters for founders.

What if my concentrated stock is in a Canadian company?

Shares that qualify as taxable Canadian property are excluded from the arrival cost-base bump and follow separate rules. If your position is in a private Canadian company, do not assume the reset applies — confirm the treatment first.

Holding a large single-stock position and a cross-border move on the horizon? Book a complimentary consultation and we will model the timing and the tax in both countries before you act.

More

from Seven Figures, Two Countries

Cross-Border

Charitable Giving: A Guide for Wealthy Canada-US Families — Article XXI, in-kind gifts, and the

cross-border philanthropy levers that work in both countries.

The

US Exit Tax When You Renounce: The Real Math at $5M+ — §877A mark-to-market, retirement, and the

§2801 transfer tax that follows you forever.

T1135

Foreign Reporting: The Form That Can Cost More Than the Tax — The CRA’s foreign-property inventory that

calculates no tax but punishes silence.

Holding

a large single-stock position and a cross-border move on the horizon? Book a

complimentary consultation and we will model the timing and the tax in both

countries before you act.

This article is general education, not personalized tax, legal, or

financial advice. Rules differ by province and state and change over time.

Speak with a cross-border advisor before acting. — 49th Parallel Wealth

Management.

From the Desert to the Tundra™

0 thoughts on “Concentrated Stock When You Move to Canada: The $5M Diversification Problem”

Pingback: T1135 Foreign Reporting: The Form That Can Cost More Than the Tax - Crossing the 49th Parallel