2026 Tax Changes: US & Canada Side by Side

DISCLAIMER: This article is for educational purposes only and does not constitute tax, legal, or financial advice. Tax rules change frequently. Always consult a qualified cross-border tax professional before making decisions based on the information below. |

Every fall, the IRS adjusts over 60 tax provisions for inflation. In 2026, those adjustments are more significant than usual thanks to the One Big Beautiful Bill, which made permanent the bracket structure introduced by the 2017 Tax Cuts and Jobs Act. For cross-border families, the year brings simultaneous changes on both sides of the border — new IRS thresholds and new CRA limits — that need to be read together, not in isolation.

This post puts both sets of numbers in one place and draws out what they mean specifically for Canadians in the US, Americans in Canada, and dual citizens managing financial lives on both sides of the 49th Parallel.

2026 US Tax Adjustments (IRS)

The following figures are sourced from the IRS inflation adjustment guidance for tax year 2026, which incorporates the One Big Beautiful Bill amendments.

Standard Deduction

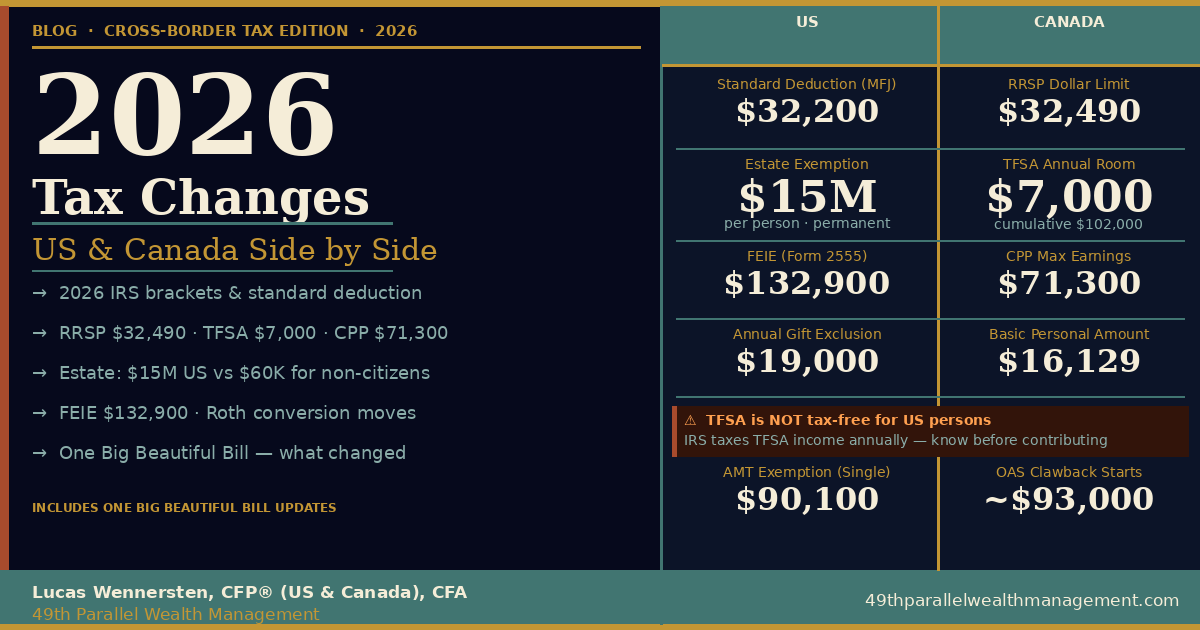

- Married Filing Jointly / Surviving Spouse: $32,200

- Head of Household: $24,150

- Single / Married Filing Separately: $16,100

- Additional deduction (65+ or blind): +$1,650 each

2026 Ordinary Income Tax Brackets

Rate | Single | Married Filing Jointly |

10% | $0 – $12,400 | $0 – $24,800 |

12% | $12,401 – $50,400 | $24,801 – $100,800 |

22% | $50,401 – $105,700 | $100,801 – $211,400 |

24% | $105,701 – $201,775 | $211,401 – $403,550 |

32% | $201,776 – $256,225 | $403,551 – $512,450 |

35% | $256,226 – $640,600 | $512,451 – $768,700 |

37% | Over $640,600 | Over $768,700 |

Estate, Gift & Key Credits

- Federal estate & gift tax exemption: $15,000,000 per person ($30M per couple) — made permanent under OBBB

- Annual gift exclusion: $19,000 per recipient

- Non-citizen spouse exclusion: $194,000

- Foreign Earned Income Exclusion (Form 2555): $132,900

- AMT exemption: $90,100 (Single) / $140,200 (MFJ)

- Health FSA: $3,400 contribution / $680 carryover

Cross-border note: Non-US-citizen residents have a US estate tax exemption of only $60,000 — not $15 million. If a Canadian owns US-situs assets (US real property, US brokerage accounts), their estate could face US estate tax at 40% on the excess. This is one of the most common planning gaps we see. Proper trust structure and Canada-US estate planning can eliminate this exposure. |

2026 Canadian Tax Adjustments (CRA)

The CRA adjustments run on a different cycle from the IRS — here are the key 2026 figures for cross-border families.

CRA Item | 2025 | 2026 |

RRSP dollar limit | $31,560 | $32,490 |

TFSA annual room | $7,000 | $7,000 |

TFSA cumulative (since 2009) | $95,000 | $102,000 |

Basic Personal Amount | $16,129 | $16,129 (indexed) |

CPP max pensionable earnings | $68,500 | $71,300 |

CPP employee contribution rate | 5.95% | 5.95% |

OAS clawback threshold | ~$90,997 | ~$93,000 (est.) |

CPP2 max earnings | $73,200 | $81,200 |

For full details on RRSP contribution rules, see the CRA’s RRSP guide. For TFSA contribution room and rules, see the CRA’s TFSA page.

TFSA warning for US persons: The TFSA annual limit is $7,000 in 2026. If you are a US citizen, green card holder, or US tax resident living in Canada, do not treat a TFSA as tax-free. The IRS does not recognize it as a tax-advantaged account. Income earned inside your TFSA is generally taxable to you in the US each year. This is among the costliest cross-border planning mistakes we see — and it is irreversible once the income has been earned. |

5 Strategic Takeaways for Cross-Border Families

- Bracket management: Wider 2026 US brackets create more room for Roth conversions and capital gain harvesting before the 37% threshold. If you are in the 22% or 24% bracket, this is a favorable year to model a conversion. For cross-border clients, coordinate with your Canadian tax position — a US Roth conversion is not a Canadian taxable event, but your Canadian income affects the overall analysis.

- RRSP vs. Roth: The 2026 RRSP limit of $32,490 and the Roth IRA limit of $7,000 ($8,000 if 50+) represent complementary tools. RRSP contributions reduce Canadian taxable income; Roth contributions grow tax-free in the US. Which to prioritize depends on your residency, income split between countries, and withdrawal timeline. This is exactly the analysis a cross-border financial planning review is designed to produce.

- Estate planning window: The $15 million exemption is permanent under OBBB, but political winds change. More importantly for cross-border families — the $60,000 US estate tax exemption for non-US-citizen residents makes Canada-US estate planning essential if you own US-situs assets. Trust structures, titling strategies, and treaty elections can all help.

- FEIE and the Canada-US Treaty: The $132,900 FEIE applies only to earned income — not RRSP withdrawals, CPP, or investment income. US citizens in Canada who rely on the FEIE to zero out US tax owe it to themselves to model whether the Foreign Tax Credit election under the Canada-US Tax Treaty produces a better result, particularly as Canadian source income rises.

- Tax filing deadlines: Canadian T1 is due April 30 (balance owing), with an extension to June 15 for self-employed. US citizens and green card holders in Canada get a June 15 automatic extension for Form 1040, but interest on any balance owing runs from April 15. FBAR (FinCEN 114) is due April 15, auto-extended to October 15. Cross-border tax planning includes coordinating these deadlines so you are not caught by penalties in either country.

Frequently Asked Questions

What is the standard deduction for 2026?

The 2026 standard deduction is $32,200 for married filing jointly, $24,150 for head of household, and $16,100 for single filers — set by the IRS under the One Big Beautiful Bill inflation adjustments.

What is the RRSP contribution limit for 2026?

The 2026 RRSP dollar limit is $32,490, up from $31,560 in 2025. Your actual deduction room is 18% of your prior-year earned income up to this limit, plus unused room carried forward.

What is the TFSA contribution limit for 2026?

The 2026 TFSA annual limit is $7,000. Cumulative room since 2009 is $102,000. Important: US persons face US tax on TFSA income because the IRS does not recognize it as tax-advantaged.

What is the federal estate tax exemption for 2026?

The US federal estate and gift tax exemption is $15,000,000 per person ($30M per couple), made permanent under OBBB. Non-US-citizen residents have only $60,000 in US exemption — making cross-border estate planning essential.

What is the Foreign Earned Income Exclusion for 2026?

The 2026 FEIE is $132,900, claimed via Form 2555. It applies to earned income only — not RRSP withdrawals, CPP, OAS, or investment income.

Did the One Big Beautiful Bill change the 2026 tax brackets?

Yes. OBBB made the TCJA bracket structure permanent and applied inflation adjustments, resulting in wider brackets at each rate. This creates more planning room for Roth conversions and gain harvesting.

What is the 2026 TFSA limit for Canadians who moved to the US?

If you became a US tax resident, you stop accumulating TFSA room from that year forward. Existing room is preserved, but contributions may create US tax complications. Withdrawing before US residency is often the cleaner path.

How do 2026 CPP changes affect cross-border retirees?

The CPP maximum pensionable earnings ceiling is $71,300 in 2026. CPP paid to US residents is subject to 15% Canadian withholding under the Treaty, with a credit available on the US return.

Should I do a Roth conversion in 2026?

Wider 2026 brackets make it a favorable year to evaluate conversions. For cross-border clients, model the Canadian impact as well — a Roth conversion is a US taxable event and may interact with Canadian income. Work with a cross-border advisor.

What CRA deadlines matter for cross-border families in 2026?

Canadian T1: April 30 balance owing (June 15 for self-employed). US Form 1040 for Canadians abroad: June 15 automatic extension, interest from April 15. FBAR (FinCEN 114): April 15, auto-extended to October 15.

At 49th Parallel Wealth Management

Tax season creates clarity — two returns, two currencies, two sets of rules. Reading them together rather than in isolation is the foundation of sound cross-border tax planning. At 49th Parallel Wealth Management, we hold dual licensing in both Canada and the US and work exclusively with cross-border families who need both sides of the picture.

Whether you are optimizing a Roth conversion from Canada, reviewing your estate exposure, or simply making sure you are not missing RRSP room — book a complimentary consultation and let’s work through the 2026 numbers together.

From the Desert to the Tundra™