US Tax Slip Deadlines for 2026: W-2s, 1099s, K-1s, and Why Your Filing May Be Delayed

By Lucas Wennersten, CFP® (US & Canada), CFA · 6 minute read · Updated May 14, 2026

Every tax season begins with the same question:

“Am I still waiting on a tax slip, or is it safe to file?”

Understanding US tax slip deadlines is critical, especially if you receive income from employment, investments, or private funds. While many forms have statutory deadlines, others — most notably 1099 investment forms and K-1s — are frequently delayed or amended, sometimes weeks or even months after the official deadline.

For Canada-US cross-border filers, the timing problem is doubled: you’re waiting on both US tax slips AND Canadian tax slips (T4, T5, T3, NR4) before you can file accurately in either country.

This guide explains when each major US tax slip is supposed to arrive, why amended forms are common, how long amended 1099s typically take, how K-1s can delay filing well into spring or beyond, and how to plan your filing timeline to avoid costly amendments — including the cross-border complication that catches dual filers off guard every year.

Key US Tax Slip Deadlines (At a Glance)

W-2 — Wage and Salary Income

Issued by: Employers · Statutory deadline: January 31 · 2026 effective date: February 2 (because January 31, 2026 falls on a Saturday)

Reliability: High. Most W-2s arrive on time and are accurate. Corrections happen but are uncommon compared to investment-related slips. Per IRS Form W-2 instructions, employers must furnish W-2s to employees and file with the SSA by January 31.

1099-NEC — Non-Employee Compensation

Issued by: Businesses paying contractors · Statutory deadline: January 31 · 2026 effective date: February 2

Reliability: Moderate. Errors typically relate to classification (employee vs contractor) or timing, but usually surface quickly within a few weeks of issuance.

1099-DIV / 1099-INT / 1099-B — Investment Income

Issued by: Brokerage firms, banks, custodians · Statutory deadline: February 15 · 2026 effective date: February 17 (because February 15, 2026 is a Sunday and February 16 is Presidents Day)

Reliability: Low to moderate. Amendments: common. These are the most frequently amended tax slips each year, often because final income characterization is not known by February. Per IRS general instructions for 1099 forms, brokers can issue corrected 1099s any time during the year — there is no formal cutoff.

Schedule K-1 — Partnership and Trust Income

Issued by: Partnerships, S corporations, trusts, estates · Statutory deadlines:

- Partnerships (Form 1065) and S-corps (Form 1120-S): March 15 — entity files Schedule K-1 with the return

- Trusts and estates (Form 1041): April 15 — aligned with personal return deadline

- Extensions: 6-month extensions push K-1 deadlines to September 15 (partnerships/S-corps) or October 15 (trusts/estates)

- Tax payments are due on the original deadline regardless of any extension filed

Why 1099 Investment Forms Are Often Amended

Investment 1099s depend on final income characterization, which often isn’t known by February. Common causes include:

- Mutual fund capital gain reclassifications (ordinary vs long-term)

- Foreign tax credit adjustments — particularly for international funds

- Real Estate Investment Trust (REIT) income reclassifications between ordinary, qualified, and return-of-capital

- Return-of-capital recalculations from underlying holdings

- Late-reported partnership income inside funds (one K-1 inside the fund delays the fund’s 1099 to its investors)

Brokerages often issue a “best available” version by the statutory deadline, then correct it later when underlying data is finalized.

Amended 1099s: The Real-World Timeline

In practice, amended 1099s arrive in this pattern:

- Late February to mid-March: Most common amendment window

- Early April: Still normal for complex portfolios with international or REIT holdings

- Late April: Happens, especially with REITs or foreign holdings still finalizing characterization

- Mid-May: Not unusual in complex high-income portfolios

- June (rare): Typically tied to partnership-heavy funds where underlying K-1s arrived late

For investors with private funds, REIT ETFs, or international exposure, waiting until late March or April to file is often the safer move.

Schedule K-1s: The Biggest Source of Delays

What is a K-1?

A Schedule K-1 reports income from:

- Partnerships and LLCs taxed as partnerships

- Private equity funds and hedge funds

- Certain real estate and alternative investments

- S corporations distributing pro-rata income to shareholders

- Trusts and estates distributing income to beneficiaries

Why K-1s Delay Tax Filing

K-1 timing is a function of the entity’s own books and underlying investments:

- Partnerships rely on their own underlying investments — if those issue K-1s, your K-1 has to wait for them

- Income may be sourced across multiple states or countries, each requiring its own reporting

- Final tax treatment (ordinary income vs capital gain vs return-of-capital) often isn’t known until weeks after March 15

- Many alternative investments routinely use extensions, pushing K-1 issuance to September or October

It is common for K-1s to arrive in late March or early April even without entity extensions, and as late as September-October with extensions.

How K-1 Investments Affect Your Filing Strategy

If you invest in partnerships or alternative investments:

- Filing early increases amendment risk significantly

- Filing an extension is often prudent, not problematic

- Additional state filings may be triggered for each state where the partnership has activity

- Extension Form 4868 does NOT delay payment — estimated tax must still be paid by April 15

Best-Practice Filing Timeline by Investor Profile

Match your filing window to the complexity of your income:

Investor Profile | Recommended Filing Window |

W-2 only (employment income) | Early February — once W-2 arrives and is verified |

1099 investment income (standard brokerage) | Mid-March — wait through the most common amendment window |

REITs / foreign funds / international exposure | Late March to April — corrections trail into mid-April |

K-1s / private partnerships / hedge funds | File extension — Form 4868 by April 15, then file when K-1s arrive |

Cross-border (US + Canadian slips) | April — wait for both T-slips AND amended 1099s |

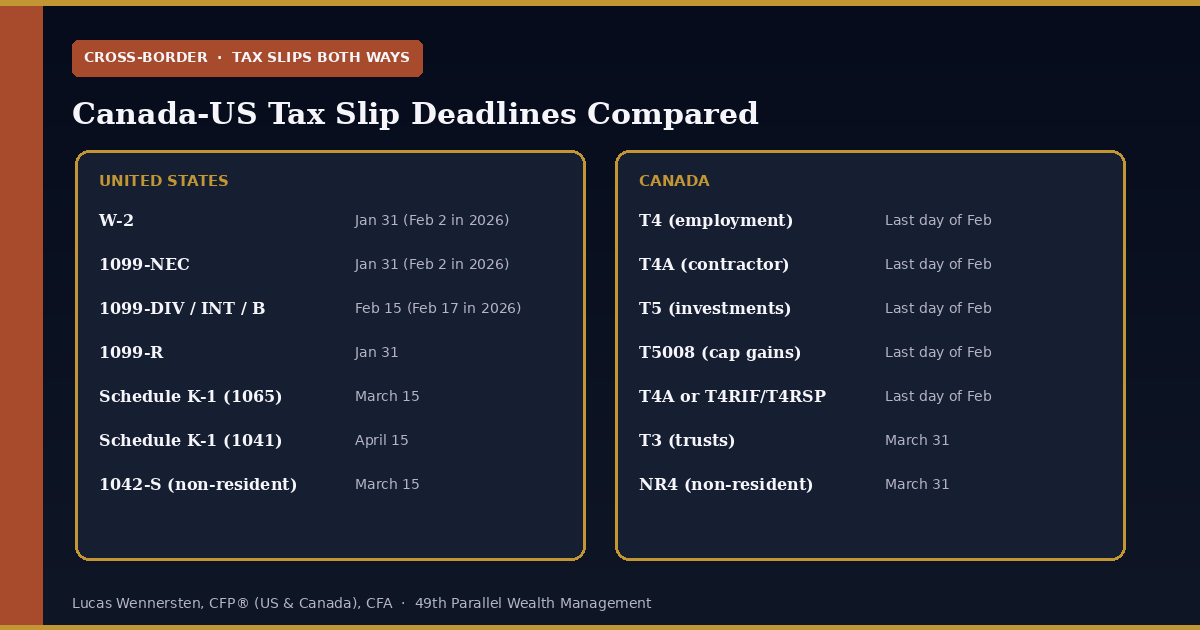

The Canada-US Cross-Border Timing Problem

Canadians earning US income, Americans earning Canadian income, and dual residents face a doubled timing problem. You’re waiting for tax slips from two countries with different statutory deadlines, and your filing in either jurisdiction depends on having complete information from both. Filing one return before the other’s slips arrive often leads to amendments in both countries.

Here’s how the major tax slips line up across the border:

Income Type | US Slip (Deadline) | Canadian Slip (Deadline) |

Employment | W-2 (Jan 31) | T4 (last day of Feb) |

Self-employment / contractor | 1099-NEC (Jan 31) | T4A (last day of Feb) |

Investment income | 1099-DIV/INT (Feb 15) | T5 (last day of Feb) |

Brokerage capital gains/losses | 1099-B (Feb 15) | T5008 (last day of Feb) |

Trust / fund distributions | Schedule K-1 (March 15 / April 15) | T3 (March 31) |

Non-resident withholding | 1042-S (March 15) | NR4 (March 31) |

Retirement plan distributions | 1099-R (Jan 31) | T4A or T4RIF/T4RSP (last day of Feb) |

Why this matters for cross-border filers: Canadian T-slip deadlines (mostly late February or March 31) often arrive AFTER US 1099 deadlines but BEFORE US K-1s. If you file your US return early to claim a refund, you may need to amend it once your Canadian foreign tax credit calculation finalizes — which requires the Canadian slips. Conversely, filing your Canadian return early means estimating US tax paid before the actual US filing is complete.

The right approach for most cross-border filers: file extensions in BOTH countries and process both returns together in late March or April once all slips from both directions have arrived. Canada-US tax strategy is fundamentally a timing problem as much as a calculation problem — and getting the timing wrong creates amendments in both countries simultaneously.

The Bottom Line

Don’t file before you have all your slips. Most amendments come from filers who rushed — chasing a refund, beating a perceived deadline, or simply wanting to finish. The cost of an amendment (preparer fees, IRS or CRA processing delays, treaty mechanics that re-cascade) almost always exceeds the cost of waiting an extra month.

For cross-border filers, the math is even clearer: an extension on both sides costs nothing and prevents the doubled-amendment cycle that haunts cross-border tax preparation every spring. Current 2026 IRS thresholds and current Canadian rates apply to the year you actually file — confirm before submitting either return.

Frequently Asked Questions

Q: Can I file my US tax return before all my 1099s arrive?

A: Yes, but if an amended 1099 is issued later, you may need to amend your return. Amendments cost time and money — preparer fees, IRS processing delays, and potential refund recapture. For most investors with brokerage accounts, waiting until mid-March is the safer move.

Q: Should I wait if my brokerage warns of upcoming corrections?

A: Usually yes. When a brokerage labels a 1099 as preliminary or warns that corrections are coming, that’s a strong signal the final version will be different. Filing on a known-incomplete 1099 nearly guarantees an amendment within 60 days.

Q: Are amended tax returns a big deal?

A: They are manageable but can delay refunds (sometimes by months), increase tax preparation costs (most preparers charge for amendments), and create compliance complexity — especially cross-border, where an amendment in one country can require an amendment in the other.

Q: Why do K-1s arrive so late?

A: Because partnerships must finalize their own books before issuing accurate allocations to investors. Many partnerships invest in other partnerships, creating a cascade of K-1 dependencies. K-1s commonly arrive in late March or early April, and partnerships using extensions can push issuance to September or October.

Q: Does filing an extension increase audit risk?

A: No. Extensions are routine and common for complex taxpayers. The IRS does not view extension-filers any differently from on-time filers from an audit-selection standpoint. Filing accurately is far more important than filing fast.

Q: What are the Canadian tax slip deadlines?

A: Most Canadian information slips (T4, T4A, T5, T5008) are due by the last day of February — typically February 28 or 29 in a leap year. T3 trust slips and NR4 non-resident slips are due by March 31. For full Canadian tax slip detail, see our companion article on Canadian tax slip deadlines.

Q: How do K-1 investments affect Canadian filers reporting US partnership income?

A: Canadian filers receiving K-1 income from US partnerships face the same K-1 timing problem AND must report the same income on their Canadian T1 with appropriate foreign tax credits. Because K-1s often arrive after the Canadian April 30 personal filing deadline, Canadian filers with US partnership exposure typically need to file extensions in both countries. The Canadian-side filing depends on knowing the final K-1 numbers.

Q: Do I have to wait for both US and Canadian slips if I’m a cross-border filer?

A: In practical terms, yes. Filing one country’s return without the other’s slips often requires later amendment to align foreign tax credit calculations. The clean approach is to file extensions in both countries (Form 4868 in the US, no formal extension needed in Canada — just file by June 15 if you have foreign income), then complete both returns together once all slips have arrived.

Q: When can I file if I only have W-2 income with no investments?

A: As soon as your W-2 arrives, typically in early February. W-2 income is the most reliable category and rarely produces amendments. The waiting-game advice is specifically for investment income, partnership income, and cross-border filers — pure employment-income filers can file early without significant amendment risk.

Cross-Border Tax Filing Help

If you file in both the US and Canada, the slip-timing problem multiplies. The amendments that follow rushed filings often produce errors in foreign tax credit calculations that cascade across multiple years. Book a complimentary consultation with 49th Parallel Wealth Management to coordinate your cross-border tax timing before the rush of next spring’s filing season.

This article is for general educational purposes and is not tax, legal, or investment advice. IRS and CRA deadlines are confirmed for the 2026 tax year as of publication. Statutory holidays and weekend adjustments may shift the effective deadline by 1-2 business days. Confirm current deadlines with the IRS or CRA before filing.