DISCLAIMER: This article provides general educational information about US Social Security policy changes and their interaction with Canadian retirement programs. It is not legal, tax, accounting, or financial advice. Eligibility rules and benefit amounts change. Confirm current details with the Social Security Administration, the Internal Revenue Service, the Canada Revenue Agency, and a qualified cross-border financial advisor before making decisions that depend on these programs. |

By Lucas Wennersten, CFP® (US & Canada), CFA · Originally published March 2025 · Refreshed May 2026 · 10 minute read

Susan worked 30 years in Ontario and 10 in the US. For four decades, that combination cost her $613 a month — until January 2025

Susan spent 30 years as an Ontario teacher and 10 earlier years in the United States in her 20s. She built up a full Canada Pension Plan and earned the 40 US Social Security credits required to claim a US benefit. Two countries, two careers, two retirement systems contributed to by every paycheque.

From the original 1983 Reagan-era Windfall Elimination Provision through 2024, that combination would have slashed her US Social Security benefit by up to $613 per month. The penalty was triggered by her CPP. Same career. Same contributions. More than half her US benefit erased before she ever cashed a cheque.

On January 5, 2025, President Biden signed the Social Security Fairness Act in one of his final acts in office. The Windfall Elimination Provision was repealed. The Government Pension Offset (GPO) was repealed alongside it. Both changes were made retroactive to January 2024.

Sixteen months later, Susan and approximately 3.1 million other affected retirees have received roughly $17 billion in retroactive lump-sum payments. Monthly benefits have been restored to their full unreduced amount, permanently.

Here’s what every Canadian with US Social Security — current beneficiary, future filer, surviving spouse — needs to know about what changed, what you may be owed, and what’s still at issue in May 2026.

What the Windfall Elimination Provision was, and why Canadians got caught in it

The Windfall Elimination Provision was a federal rule, in place since the Social Security Amendments of 1983, that reduced the US Social Security benefit of workers who also received a pension from work not covered by Social Security. It was originally designed to prevent perceived double-dipping by US public-sector workers — teachers in states that opted their employees out of the Social Security system, federal employees on the Civil Service Retirement System before 1984, certain police and fire retirees — who were earning pensions through systems where Social Security taxes were not withheld.

The intent was domestic. The reach was global. Foreign pensions were swept into the definition of “non-covered employment,” and Canada Pension Plan benefits qualified. A Canadian who had worked enough US years to earn the 40-credit US Social Security minimum, but whose career was primarily Canadian, found their US benefit reduced because they also collected CPP. The reduction had nothing to do with whether they had paid US Social Security taxes during their American years — they had. The reduction was triggered solely by the presence of the foreign pension.

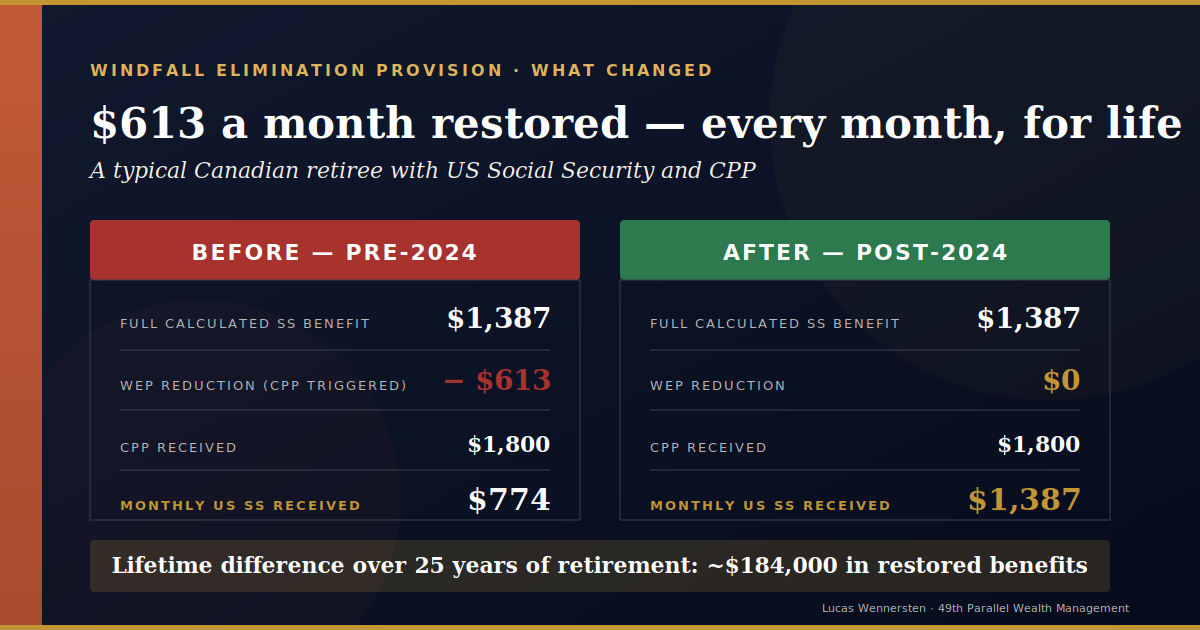

The math, pre-repeal, was harsh. WEP modified the first “bend point” in the Social Security benefit formula — the portion that delivers the steepest replacement rate to lower lifetime earners. Instead of replacing 90 percent of earnings up to the first bend point, WEP could replace as little as 40 percent. The maximum reduction was capped at half of the monthly CPP amount, or $613 in 2025 — whichever was less. A Canadian receiving $1,800 per month in CPP saw their US Social Security benefit reduced by the full $613 every month, for life.

The Substantial Earnings exception offered some relief: workers with 30 or more years of substantial US earnings were exempt from WEP entirely. Most cross-border careers didn’t reach that threshold. Cross-border workers who spent a portion of their career in each country were precisely the people the rule punished hardest.

What the Social Security Fairness Act actually changed

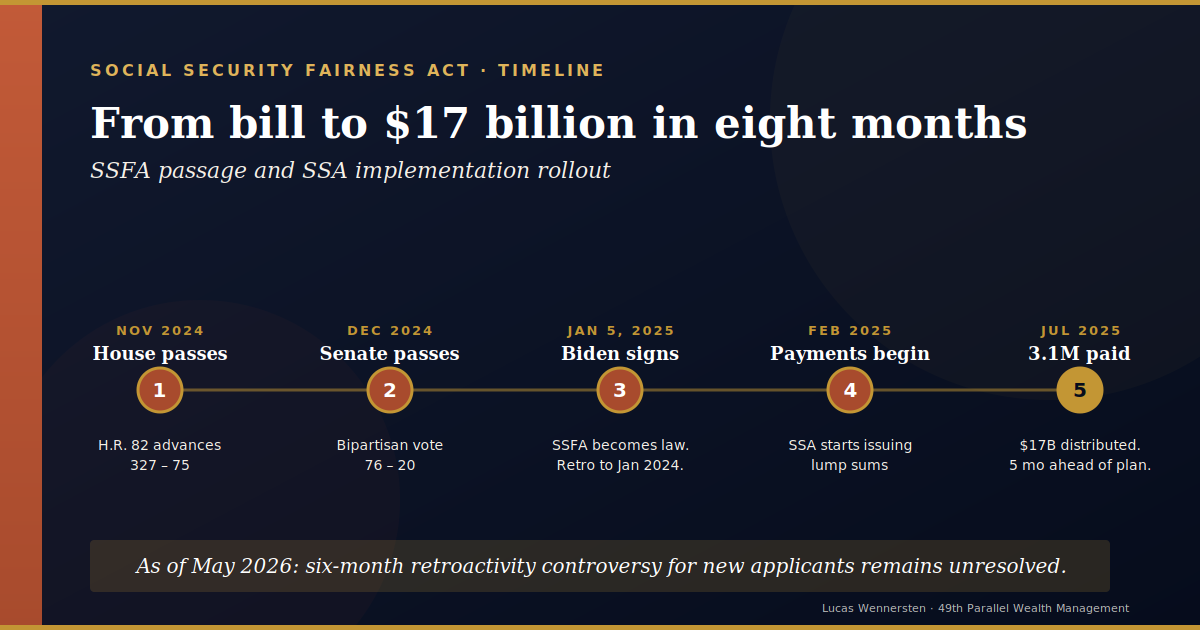

The Social Security Fairness Act of 2023 (H.R. 82) passed the US House in November 2024 by 327 votes to 75, and the Senate in December 2024 by 76 to 20. President Biden signed it into law on January 5, 2025. Per the official Social Security Administration explainer, the law repealed both the Windfall Elimination Provision and the Government Pension Offset effective January 2024 — meaning December 2023 was the last month either reduction applied to anyone’s benefit.

Two provisions were eliminated in a single piece of legislation. WEP, which reduced a worker’s own Social Security benefit when they also received a non-covered pension. And GPO, which reduced spousal and survivor Social Security benefits by two-thirds of the recipient’s own non-covered pension — a rule that had zeroed out benefits entirely for many surviving spouses.

SSA implementation was faster than initially projected. By July 2025, the agency had processed over 3.1 million payments totaling approximately $17 billion in retroactive benefits. Automatic adjustments for beneficiaries who were already collecting Social Security with WEP or GPO reductions were largely complete by mid-2025 — roughly five months ahead of original projections. The Congressional Budget Office estimates the repeal will cost approximately $196 billion in additional benefit payments over the following decade.

For Canadians, this is unambiguously good news. Anyone who was previously affected by either provision has had their benefits restored. The Railroad Retirement Board Social Security Fairness Act FAQ applies the same rules to railroad retirees, parallel to SSA’s treatment.

What the repeal specifically means for Canadians with CPP

The single largest change for cross-border retirees is straightforward: receiving CPP no longer reduces your US Social Security benefit by a single dollar. The relationship between the two systems is finally clean. You earn CPP through your Canadian career. You earn US Social Security through your American career. You collect both at full strength.

The monthly benefit increase varies based on individual circumstances. Canadians whose US careers were shorter than 30 years and whose CPP amounts are typical have generally seen $300 to $613 per month restored. Those whose pre-repeal benefit was capped at the maximum WEP reduction of $613 see exactly that amount returned. Over a 25-year retirement, the lifetime difference for a Canadian who would have hit the maximum WEP reduction is roughly $184,000 in restored Social Security benefits — meaningful retirement income.

The Government Pension Offset repeal carries equal weight for surviving spouses. The GPO previously reduced spousal and survivor Social Security benefits by two-thirds of the recipient’s own non-covered pension. For Canadian widows and widowers of US workers who had been zeroed out by the offset, full survivor benefits are now restored — both prospectively and retroactively.

The US-Canada Totalization Agreement, in place since 1984, still governs how Social Security and CPP credits are coordinated when you have a split career. The WEP repeal does not change Totalization mechanics. It only removes the reduction that used to be applied after the underlying benefit was calculated. For most Canadians, this is a strict improvement: the Totalization Agreement helps you qualify when your US work alone is borderline insufficient, and the WEP no longer haircuts what you qualify for. For broader context on retirement-stage cross-border planning, see our framework on cross-border retirement planning.

Three common misconceptions worth clearing up directly: the WEP repeal does not affect CPP — your CPP amount is unchanged. The repeal does not change the Canadian tax treatment of US Social Security received in Canada — that is governed by the US-Canada Tax Treaty and continues to apply normally. And the repeal does not change US Social Security’s eligibility requirements — you still need 40 credits (generally 10 years of substantial US earnings) to qualify.

|

Have you been paid back? Three scenarios

Whether you’ve already been made whole — or whether you need to take action — depends on which of these three groups you fall into.

Scenario 1 — You were already collecting US Social Security with a WEP reduction

The Social Security Administration automatically recalculated your benefit and issued a retroactive lump-sum payment covering January 2024 through the implementation date. Most automatic adjustments completed by mid-2025. To confirm: log into your MySSA account and verify that your current monthly benefit reflects no WEP reduction. If it still does, contact SSA directly. You generally do not need to file any new application or paperwork — the adjustment is supposed to be automatic.

Scenario 2 — You never applied for US Social Security because you knew WEP would have eaten most of it

This is the group with the highest urgency. Apply now through the SSA online application portal or call 1-800-772-1213. Under current SSA interpretation, new applicants are limited to six months of retroactive benefits from their application date — not the full retroactive period back to January 2024. Every month you wait is potentially a month of retroactive eligibility you lose permanently. Bipartisan senators (Collins, Cassidy, Cornyn, Fetterman) have been pushing SSA to reverse this interpretation, but as of May 2026 the six-month limit remains in effect.

Scenario 3 — You’re not yet collecting and will apply in the future

Standard SSA rules apply going forward. No WEP reduction will ever be applied to your benefit. The strategic decision becomes when to claim Social Security relative to CPP — a pure actuarial question rather than a WEP-avoidance puzzle (see the timing section below).

The ongoing six-month retroactivity controversy

There is a live policy dispute that affects Scenario 2 applicants directly, and any Canadian considering filing now should understand it before deciding when to apply.

The plain text of the Social Security Fairness Act appears to entitle all affected individuals to retroactive payments back to January 2024. The Social Security Administration, however, is applying a separate, pre-existing six-month-retroactivity limit on new Social Security applications to people who didn’t formally file during the WEP era because the Government Pension Offset would have zeroed their spousal benefit.

A real-world example reported in the federal employee press: an 81-year-old retired CSRS employee whose wife collects her own Social Security contacted SSA in late January 2025 about spousal benefits under the SSFA. After processing, he received seven months of back-pay — July 2024 forward — not the full 13 months back to January 2024. His spousal benefit had been zeroed by GPO for years; he had never formally applied because there had been nothing to receive.

In April 2026, a bipartisan group of senators sent a letter to the SSA Administrator demanding that the agency follow the plain text of the SSFA and provide full retroactivity to all applicants regardless of application date. The policy has not changed as of May 2026.

Practical implication for cross-border retirees: file your application immediately if you have been holding off. The six-month clock runs from your application date, not from the SSFA’s effective date. Delay only costs you retroactive eligibility. If the senator-led push to extend full retroactivity to new applicants eventually succeeds, that would be a windfall on top of what you would already receive — but you cannot count on it.

|

Tax treatment of the retroactive lump sum

Lump-sum retroactive payments received in 2025 are taxable income for 2025 and are reported on your 2025 Form 1099 issued in January 2026. A lump-sum election method is available under IRS rules that may let you spread the income across the years it represented, rather than being taxed on the full amount in the year received. The election can substantially reduce the tax hit for a recipient who would otherwise be pushed into a higher bracket by a multi-year lump sum landing in a single year.

Canadian residents face additional complexity. Under the US-Canada Tax Treaty Article XVIII(5), a Canadian-resident recipient of US Social Security is generally taxed only in Canada, with 85 percent of the benefit included in Canadian income. A retroactive lump sum representing 12+ months of payments potentially pushes the recipient into a higher Canadian tax bracket in the year received. There is some debate among cross-border tax practitioners about whether the US lump-sum election translates cleanly to Canadian tax treatment — practical answer: model the tax impact with a cross-border accountant before filing.

Non-resident Canadians who received the lump sum and have limited Canadian income may benefit from a Section 217 election to be taxed as a Canadian resident for the year. This is a planning opportunity worth running the numbers on — for some retirees it materially reduces tax owed. For others it is neutral or worse. The right answer depends on your specific income profile, deductions, and family situation.

How the repeal changes Social Security and CPP timing for cross-border retirees

Pre-repeal, many cross-border advisors recommended a specific timing pattern: start US Social Security at 62 to bank as many pre-WEP years as possible, then delay CPP to age 70. The logic was to minimize lifetime WEP losses by collecting unreduced Social Security for as many years as possible before CPP triggered the haircut.

That heuristic is now obsolete. WEP is gone. The Social Security and CPP timing decision is now pure actuarial mathematics — life expectancy, cash flow needs, and the delayed-credit schedules each system offers. Decisions about stopping CPP contributions and when to draw each benefit return to their underlying logic without the WEP distortion.

Practically: delaying US Social Security from 62 to 70 increases the monthly benefit by roughly 76 percent in real terms. CPP delay credits add 0.7 percent per month from age 65 to age 70, for a maximum 42 percent increase. The combined math now favors patience for most cross-border retirees in good health and without an urgent cash flow need. For retirees with shorter life expectancy or immediate income requirements, earlier claiming may still be optimal. Run actual claiming models — the simple WEP-era heuristics no longer apply.

If you’re modelling how this fits into your broader retirement picture — whether you’re an American retiring in Canada or a Canadian preparing to draw US Social Security from south of the border — the math has shifted but the framework is straightforward. WEP is one fewer variable to manage.

Frequently asked questions

Was the Windfall Elimination Provision really repealed?

Yes. The Social Security Fairness Act (H.R. 82) repealed the Windfall Elimination Provision and the Government Pension Offset on January 5, 2025, retroactive to January 2024. The WEP no longer reduces any Social Security beneficiary’s payment. The repeal is permanent — there is no scheduled sunset or expiration.

Did the WEP repeal apply to Canadians with CPP?

Yes. The WEP previously reduced US Social Security benefits for Canadians who also received CPP, because CPP was treated as a non-covered pension under the rule. With WEP repealed, CPP no longer triggers any reduction in US Social Security. Canadians who had been receiving reduced benefits have had their full amounts restored, both prospectively and retroactively to January 2024.

How much more will I get from Social Security now that WEP is gone?

It varies. The monthly increase depends on your US earnings history and CPP amount, but typical affected Canadians have seen $300 to $613 per month restored. The maximum WEP reduction in 2025 was $613 per month, so anyone whose benefit had been reduced by that amount sees the full $613 returned. Over a 25-year retirement, the lifetime difference can exceed $180,000.

Do I need to do anything to get my benefits adjusted?

If you were already collecting US Social Security with a WEP reduction, no — the Social Security Administration automatically recalculated your benefit and issued a retroactive lump-sum payment, with most adjustments completed by mid-2025. If you never applied because WEP would have reduced your benefit substantially, you should apply now via ssa.gov/apply. Time is of the essence because of the six-month retroactivity rule for new applicants.

What if I never applied for Social Security because of WEP — can I still file?

Yes, and you should file immediately. New applicants are currently limited to six months of retroactive benefits from their application date under SSA’s interpretation of the rules — not the full retroactive period back to January 2024. Every month you wait is potentially a month of retroactive eligibility you lose. Bipartisan senators have asked SSA to reverse this interpretation, but it remains in effect as of May 2026.

Will I get back payments going to January 2024 if I apply now?

Probably not. SSA’s current policy limits new applicants to six months of retroactive benefits from their application date. So if you apply in May 2026, your retroactive benefit would generally start in November 2025, not January 2024. There is ongoing bipartisan pressure on SSA to extend full retroactivity to new applicants, but the policy has not changed.

Are the retroactive lump-sum payments taxable?

Yes. Lump-sum payments received in 2025 are taxable income for 2025 and are reported on your 2025 Form 1099 issued in January 2026. A lump-sum election method is available that may let you spread the income over the years it represented; the IRS instructions for Social Security benefits explain the calculation. Canadian residents have additional tax treaty considerations — speak with a cross-border tax professional before filing.

Does the WEP repeal affect my CPP benefits?

No. The WEP repeal only changed how US Social Security calculates benefits for people who receive non-covered pensions like CPP. Your CPP amount, when you collect it, and the rules around it are entirely unchanged. The repeal removes a US-side penalty; it does not modify the Canadian side of the equation at all.

How does this change when I should start Social Security if I also have CPP?

The pre-repeal heuristic of starting Social Security early and delaying CPP to age 70 was designed to minimize lifetime WEP losses. With WEP gone, the timing decision is pure actuarial math — life expectancy, cash flow needs, and the delayed-credit schedules. For most cross-border retirees in good health, delaying both benefits past 65 is now cleaner, but the right answer depends on your specific situation.

Is the Government Pension Offset (GPO) also repealed?

Yes. The Social Security Fairness Act repealed both WEP and GPO at the same time. The GPO had reduced spousal and survivor benefits by two-thirds of the recipient’s non-covered pension. Surviving spouses of US workers who had been zeroed out by the offset are now eligible to receive their full Social Security survivor benefit alongside their own pension.

Plan your cross-border retirement with confidence

The Windfall Elimination Provision shaped cross-border retirement planning for four decades. With it gone, the structural complexity of coordinating US Social Security and CPP has materially decreased. But the broader cross-border planning picture — RRSP and RRIF income sequencing, US Medicare versus Canadian provincial coverage, capital gains treatment of US property, estate planning across two tax systems — remains intricate.

If you are modelling a cross-border retirement and want a clear picture of how the WEP repeal interacts with the rest of your plan — whether you have already been adjusted by SSA, are owed a retroactive payment you haven’t received, or are deciding when to start drawing Social Security and CPP — book a complimentary consultation. Lucas Wennersten holds the CFP® designation in both Canada and the United States and the CFA charter, and 49th Parallel Wealth Management is dually registered to advise on both sides of the border. For related reading, see our framework on Social Security taxation legislation and the broader Canada-US planning FAQ.