What Nobody Tells Americans Before Their First Full Year in Canada

Banking resets. Credit scores that disappear. Investment accounts that can’t follow you. The practical surprises nobody puts in the relocation guide.

AMERICANS IN CANADA SERIES Monday: How Long Can an American Stay in Canada? Tuesday: What Does Canada Actually Cost an American? Wednesday: The Tax Reality No One Tells Americans Moving to Canada Thursday: What Nobody Tells Americans Before Their First Full Year in Canada Friday: So You Want to Make It Official: The American’s Guide to Moving to Canada |

This week we covered how long you can stay, what it costs, and how the tax system works. Today is different. Today is the things that will actually surprise you when you arrive — not the big-picture policy questions but the Tuesday-morning-at-the-bank moments that nobody warned you about.

Most relocation guides are written for the planning phase. This one is written for the first twelve months after you arrive, when the plans meet reality and the gaps start to show.

|

1. Your Credit Score Starts at Zero

This is the one that surprises people most. US and Canadian credit bureaus — Equifax and TransUnion both operate in both countries — maintain completely separate files. Your 750 FICO score does not exist in Canada. When you arrive, your Canadian credit history is blank.

What this means in practice:

- Getting a Canadian credit card is difficult without a credit history. Many banks will require a secured card — meaning you deposit money as collateral to get a card with a matching limit.

- Renting an apartment is harder. Most Canadian landlords run credit checks, and a blank file looks the same as a bad file to a landlord who doesn’t know the context.

- Financing a car requires a local credit history or a large deposit.

- Building Canadian credit typically takes 12 to 24 months of consistent, on-time use of a secured card or credit-builder product.

PRACTICAL STEP Apply for a secured credit card with your new Canadian bank on the same day you open your account. Use it for a small recurring expense and pay it in full every month. This is the fastest way to begin building a Canadian credit file. After 6 to 12 months you can typically convert it to an unsecured card and your file will have enough history to function normally. |

2. Canadian Banking Is Different — and Slower to Set Up Than You Expect

Opening a Canadian bank account is straightforward, but there are friction points Americans don’t expect.

- You need a Canadian address — most major banks require proof of Canadian address before opening a full account. If you have not yet established a permanent address, this creates a chicken-and-egg problem. Some banks offer a newcomer account for people who have recently arrived and are still getting settled.

- Your US banking relationships don’t transfer — your credit history with your US bank, your overdraft arrangements, your relationship pricing — none of it carries over. You start as a new customer.

- Interac e-Transfer is not Venmo or Zelle — the Canadian digital payments system works differently from US peer-to-peer payment apps. Most Canadian landlords, tradespeople, and individuals expect payment by Interac e-Transfer. Get comfortable with it quickly.

- Wire transfers between your US and Canadian accounts incur fees and exchange rates — services like Wise or Norbert’s Gambit via a brokerage can significantly reduce the cost of moving larger amounts between countries compared to bank wire rates.

Keep your US bank account open. Most US banks will allow you to maintain your account as a non-resident, though some may restrict certain services. You will need your US account for paying US obligations, maintaining US investment accounts, and receiving US income or Social Security.

3. The OHIP Wait Period Is Real — and It Has to Be Planned For

Canada’s provincial health coverage is one of the most cited reasons Americans are drawn to moving north. But there is a gap between when you arrive and when coverage actually begins.

In Ontario, OHIP requires a three-month waiting period before coverage starts. British Columbia eliminated its waiting period. Alberta has a three-month period. Every province has different rules.

During the wait period, you have no provincial health coverage. A visit to a Canadian hospital or clinic will be billed directly to you at uninsured rates, which can be significant.

THE GAP COVERAGE SOLUTION Before your move date, arrange one of the following: • Extend your current US travel or health insurance to cover the gap period in Canada • Purchase a short-term expat health insurance policy that covers you in Canada for the wait period • If you have a spouse with Canadian health coverage, confirm whether you are covered as a dependent during the wait period Do not arrive in Canada without coverage and assume you are protected. The wait period is enforced regardless of your circumstances. |

Beyond the initial wait period, the practical reality of Canadian healthcare differs from US private insurance in ways that take adjustment. Wait times for specialist referrals and elective procedures are longer than many Americans are accustomed to. If you travel to the US regularly, confirm whether your provincial plan covers you south of the border (typically it provides limited out-of-province coverage) and consider a supplemental travel health policy.

4. Your US Investment Accounts Cannot Simply Follow You

This is the financial surprise that catches the most people off guard, and it has the most long-term consequences.

When you become a Canadian tax resident, your US brokerage is typically notified — either by you or through routine compliance checks. Most US brokerages will then restrict your account in some or all of the following ways:

- Trading restrictions: you may no longer be able to buy new positions, add to existing ones, or purchase certain securities that require a US address for distribution

- Mutual fund redemption: certain mutual funds cannot be held by non-US residents and may be force-liquidated

- Account closure: some smaller brokerages close accounts entirely for non-US residents

This does not mean your investments disappear. Existing stock, ETF, and bond holdings are typically grandfathered — you can hold them and sell them, but you may not be able to add. The practical implication is that your US accounts shift from active to maintenance mode.

At the same time, you will want to open Canadian investment accounts for ongoing investing. RRSP contributions reduce your Canadian taxable income. Non-registered accounts in Canada allow ongoing investing in Canadian and international securities.

THE TFSA REMINDER As covered in last week’s post, TFSAs have no protection under the Canada-US Tax Treaty. Income inside a TFSA is fully taxable to the IRS. Do not contribute to a TFSA without specific guidance from a cross-border tax specialist. The RRSP is generally the more appropriate registered account for Americans in Canada. |

5. The Currency Effect Is Ongoing, Not One-Time

Most people think about currency conversion as a one-time cost of moving. The reality is that currency exposure is an ongoing factor in your financial life as an American in Canada.

- Your income currency and expense currency may differ — if you receive US Social Security, a US pension, or income from US investments in USD while paying Canadian living expenses in CAD, the exchange rate affects your effective purchasing power every month.

- CAD/USD fluctuates meaningfully — the rate has ranged from near parity to 1.45 CAD per USD in recent years. A 10% move in the exchange rate is a 10% change in your effective income if you are converting regularly.

- Bank exchange rates are expensive — converting through your bank for everyday transactions can cost 2 to 3 percent in spread. For regular conversions above a few thousand dollars, services like Wise, or the Norbert’s Gambit strategy through a self-directed brokerage, offer meaningfully better rates.

The long-term solution for most Americans in Canada is currency alignment: hold CAD for Canadian expenses and USD for US obligations, and convert deliberately in larger amounts at better rates rather than continuously at bank rates.

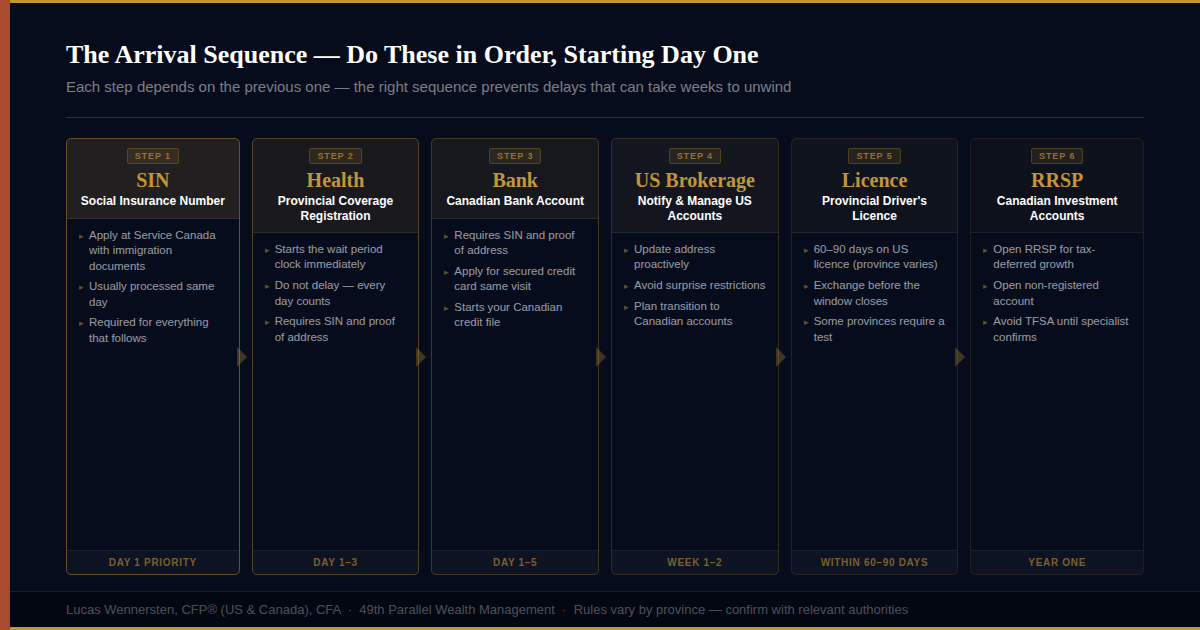

6. The Administrative Setup Takes Longer Than One Afternoon

There is a sequence of administrative steps that every newcomer to Canada must complete, and they depend on each other in ways that create delays if you do not sequence them correctly.

- Apply for a Social Insurance Number (SIN) — required to work, open a bank account, file taxes, and access government services. Apply at a Service Canada office with your immigration documents. Usually processed same day.

- Register for provincial health coverage — begin the three-month wait period clock. Do this as early as possible after arrival. You need your address and proof of immigration status.

- Open a Canadian bank account — requires your SIN and proof of address. If you don’t have a Canadian address yet, ask about newcomer accounts.

- Apply for a provincial driver’s licence — most provinces allow 60 to 90 days on your US licence. Exchange it before the window closes. The process and any testing requirements vary by province and US state.

- File for provincial health coverage benefits and any provincial credits — some provinces offer newcomer benefits. File your provincial registration promptly.

- Set up Canadian investment accounts — RRSP, and a non-registered account. Do this in year one to begin accumulating RRSP room usage and establish Canadian account history.

None of these steps are difficult individually. The friction comes from doing them in the wrong order, or discovering that step three requires something from step one that you have not yet completed. Plan the sequence before you arrive.

Frequently Asked Questions

Can I keep my US bank account when I move to Canada?

Yes, but with limitations. You can maintain your US bank account after moving, but some banks restrict services for non-US residents. You will need a Canadian account for day-to-day living and must report all foreign accounts on your annual FBAR filing if the aggregate balance exceeds $10,000 USD.

Does my US credit score transfer to Canada?

No. US and Canadian credit bureaus maintain completely separate files. Your US credit history does not carry over. When you arrive in Canada, your Canadian credit file is blank. Building Canadian credit typically takes 12 to 24 months.

How long do I have to wait for OHIP after moving to Ontario?

Three months. British Columbia eliminated its wait period. Alberta has a three-month period. Rules vary by province. You must arrange private health insurance to cover the gap. Arrive without coverage and any healthcare you receive will be billed at uninsured rates.

Can I bring my US investment accounts to Canada?

Not directly. Your US brokerage will typically restrict your ability to trade, add positions, or receive certain distributions once you become a Canadian resident. Existing holdings are generally retained but the account shifts to maintenance mode. Open Canadian accounts separately for ongoing investing.

What happens to my US health insurance when I move to Canada?

Most US employer plans terminate when you are no longer a US resident. Individual US plans typically cannot be maintained by non-residents. Transition to provincial coverage but arrange private gap insurance before you arrive to cover the wait period.

How does currency conversion affect daily life in Canada?

If your income is in USD and your expenses are in CAD, the exchange rate affects your purchasing power every month. A 10% movement in CAD/USD is effectively a 10% change in your real income. Build currency alignment into your account structure early — holding CAD for Canadian expenses and USD for US obligations reduces ongoing exposure.

Can I contribute to a TFSA as an American in Canada?

Technically yes, but the Canada-US Tax Treaty provides zero protection for TFSAs. Income inside a TFSA is fully taxable to the IRS. Do not contribute to a TFSA without specialist guidance. The RRSP is generally the more appropriate registered account for Americans in Canada.

Do I need a Canadian driver’s licence?

Yes, within the window allowed by your province — typically 60 to 90 days after establishing residency. After that you must exchange your US licence for a provincial one. Requirements vary by province and US state of issue.

The First Year Is the Most Important Year

Everything you do — or do not do — in year one sets the baseline for everything that follows. The credit file you build, the accounts you open, the elections you file on your Canadian tax return, the gap coverage you arrange before arrival: these decisions compound over time. Getting them right in year one is dramatically easier than fixing them in year three.

Tomorrow’s post brings the series together with the full action framework: permanent residency pathways, the pre-move financial checklist, and how to structure a cross-border life that actually works. If you want to talk through your specific situation before then, book a complimentary consultation.