Healthcare Coverage for Americans Moving to Canada: The Complete Guide

Provincial health covers less than most Americans expect. A plain-language guide to the OHIP gap, what supplemental insurance covers, what happens to your US Medicare, and how to build the right coverage stack as an American in Canada.

IMPORTANT NOTE This article provides general information about healthcare coverage options for Americans moving to Canada. Insurance products, provincial rules, and Medicare regulations change. Always confirm current plan details with a licensed insurance broker and verify provincial health coverage rules with your provincial ministry of health before making coverage decisions. 49th Parallel Wealth Management is registered as an investment adviser in the United States and does not sell insurance products. |

FREE DOWNLOAD The American’s 2026 Canada Relocation ChecklistIncludes the healthcare setup sequence: gap insurance, provincial registration, supplemental plan enrollment, and Medicare coordination. Free download: 49thparallelwealthmanagement.com/american-canada-relocation-checklist |

AMERICANS IN CANADA — COMPANION SERIES Part 1: How Long Can an American Stay in Canada? Part 2: What Does Canada Actually Cost an American? Part 3: The Tax Reality No One Tells Americans Moving to Canada Part 4: What Nobody Tells Americans Before Their First Full Year in Canada Part 5: So You Want to Make It Official Deep-Dive: Healthcare Coverage for Americans in Canada — this post |

Canada’s universal healthcare system is one of the most frequently cited reasons Americans consider moving north. The idea of leaving behind the complexity of US private insurance — the premiums, the deductibles, the network restrictions, the billing disputes — is genuinely appealing. And Canada’s system is good. But it is not what most Americans imagine it to be, and the gaps are significant enough to require active planning.

This post covers the full healthcare picture for Americans moving to Canada: what provincial health covers, what it does not, what happens to your US Medicare, how to bridge the OHIP wait period, and how to structure ongoing supplemental coverage for both Canadian and US healthcare costs.

|

What Provincial Health Actually Covers — and What It Doesn’t

Canadian provincial health insurance — OHIP in Ontario, MSP in British Columbia, AHCIP in Alberta, and equivalent plans in other provinces — covers medically necessary hospital and physician services. Emergency care, surgery, diagnostic imaging, hospital stays, and specialist visits when referred by a family doctor are all covered without direct cost to the patient.

What provincial health does not cover is a longer list. Approximately 60 percent of Canadians carry supplemental private insurance to fill these gaps:

| Covered by Provincial Health | NOT Covered — Supplemental Required |

| Emergency room visits | Prescription drugs (most provinces) |

| Hospital stays (shared room) | Dental care — any dental procedure |

| Surgery and anesthesia | Vision care — glasses, contacts, eye exams |

| Family doctor and specialist visits | Physiotherapy and chiropractic |

| Diagnostic imaging (MRI, CT, X-ray) | Massage therapy, acupuncture, podiatry |

| Mental health via referred psychiatrist | Psychologist and counsellor visits |

| Ambulance (partial in some provinces) | Private or semi-private hospital room |

| Maternity care and delivery | Out-of-country emergency care (very limited) |

The prescription drug gap is particularly significant for Americans accustomed to employer-sponsored plans that covered medications. In Canada, provincial drug coverage programs exist but vary widely by province and typically apply only to seniors, low-income residents, or specific disease categories. Most working-age adults pay out of pocket or through a private supplemental plan.

PROVINCIAL VARIATION NOTE Every province’s health plan is different. British Columbia recently introduced a provincial pharmacare program covering many common medications. Quebec requires all residents to have either employer-group or private drug coverage. Ontario has a limited pharmacare program for residents under 25 and over 65. Alberta covers seniors’ drugs through AHCIP. Confirm your target province’s specific coverage before assuming what your provincial plan will or will not include. |

The Provincial Wait Period: Your First Healthcare Gap

Before provincial health coverage begins, you have no government health insurance in Canada. This is the OHIP gap — and it applies in most provinces, not just Ontario.

| Province | Wait Period | Notes |

| Ontario (OHIP) | 3 months | Coverage begins on the first day of the fourth month after arrival |

| Alberta (AHCIP) | 3 months | Must apply within 3 months of establishing residency |

| British Columbia (MSP) | None | Wait period eliminated as of 2020 |

| Quebec (RAMQ) | None | Coverage begins when provincial residency is established |

| Manitoba (Manitoba Health) | 3 months | Coverage begins on the first day of the fourth month |

| Nova Scotia (MSI) | 3 months | Must register within 30 days of arrival |

| New Brunswick (Medicare NB) | 3 months | Immediate in some circumstances — confirm on arrival |

During the wait period, any healthcare you receive in Canada is billed at uninsured rates. A walk-in clinic visit typically costs $150 to $250 CAD. An emergency room visit without coverage can run $500 to $2,000 CAD or more, depending on treatment. A hospitalization is substantially higher.

Gap Insurance Options

- Extended travel health insurance — the simplest and most common solution. Extend your existing US travel or health insurance policy to cover you in Canada during the wait period. Many US insurers will not cover this, so confirm before assuming your plan applies.

- Newcomer or visitor health insurance — plans specifically designed for people who have recently arrived in Canada and are waiting for provincial coverage. Companies such as Guard.me, Manulife, and Sun Life offer newcomer plans. Typically covers emergency hospital and physician care.

- International health insurance — a longer-term option that provides comprehensive coverage in multiple countries. For Americans who may continue to spend time in the US, an international plan can cover both the wait period and ongoing US travel in a single policy.

ARRANGE BEFORE YOU ARRIVE Do not arrive in Canada without gap coverage in place. Some insurers will not issue a newcomer or travel health plan to someone who is already in Canada without coverage. Apply before your move date, not after you arrive and realize you need it. |

Supplemental Health Insurance in Canada: What You Need After the Wait

Once your provincial health coverage begins, you have a solid foundation — but as the table above shows, significant gaps remain. This is why approximately 60 percent of Canadians carry private supplemental coverage. For Americans accustomed to comprehensive employer-sponsored plans, the supplemental layer is non-negotiable.

Employer Group Benefits

If you are working for a Canadian employer, your first step is to confirm whether they offer group extended health and dental coverage. Most Canadian employers with full-time employees provide this as a standard benefit. Enrollment is typically required within 30 to 90 days of your employment start date — missing this window often means waiting for the next open enrollment period.

Group plans typically cover a significant portion of prescription drug costs, dental care up to an annual maximum, vision care, and a set of paramedical services including physiotherapy, massage therapy, chiropractic, and psychological counselling. Coverage quality varies significantly by employer and plan design.

Individual Supplemental Plans

If you are self-employed, retired, or your employer does not offer group benefits, individual supplemental plans are available from major Canadian insurers including Sun Life, Manulife, Blue Cross, and Green Shield Canada. These plans mirror group coverage but are purchased directly and are typically more expensive on a per-person basis.

You must be covered by your provincial health plan to enrol in most Canadian supplemental plans. You cannot purchase Canadian supplemental coverage during the provincial wait period.

Approximate monthly costs for individual supplemental coverage covering dental, vision, prescription drugs, and basic paramedicals:

- Single adult under 40: $80 – $150 CAD/month

- Single adult 40–60: $130 – $250 CAD/month

- Single adult 60+: $200 – $350 CAD/month

- Couple (non-smoker, age 55): $350 – $550 CAD/month

Pre-existing conditions are typically excluded from individual supplemental plans or result in rated premiums. The earlier you enroll after gaining provincial coverage, the better your terms are likely to be.

What Happens to Your US Medicare When You Move to Canada

This is one of the most misunderstood aspects of moving to Canada for Americans who are 65 or older or who are approaching Medicare age. The short answer: Medicare does not follow you to Canada and does not pay for healthcare received there.

Medicare Part A — Hospital Insurance

Most Americans receive Part A without a monthly premium because they paid Medicare taxes for at least 10 years during their working career. Part A does not provide coverage outside the United States (with extremely limited exceptions for border emergencies). However, since it carries no premium for most people, there is generally no reason to disenroll from Part A when you move to Canada. It remains in place and your eligibility is preserved.

Medicare Part B — Medical Insurance

Part B covers physician services and outpatient care in the United States. It carries a monthly premium — $185.00 USD in 2025 for most enrollees, with income-based surcharges (IRMAA) for higher earners. Since Part B provides no coverage in Canada, you may choose to voluntarily disenroll when you establish Canadian residency to avoid paying premiums for coverage you cannot use.

MEDICARE PART B DISENROLMENT WARNINGIf you disenroll from Part B and later return to the United States and want to re-enroll, you will face a late enrolment penalty of 10% of the standard premium for each full 12-month period you were not enrolled. This penalty applies for life. If there is any possibility you will return to the US and use Medicare in the future, calculate the cost of maintaining Part B against the cumulative penalty before disenrolling. The General Enrolment Period for re-enrollment is January 1 to March 31 each year, with coverage starting July 1. If you return to the US and need Part B coverage urgently, you may have a significant wait. |

Medicare Part D — Prescription Drug Coverage

Part D provides prescription drug coverage in the United States. Like Part B, it carries a monthly premium and provides no coverage in Canada. The same late enrollment penalty logic applies — disenrolling and re-enrolling later results in a permanent premium surcharge of 1% of the national base premium for each full month you were not enrolled.

Medicare Advantage (Part C)

Medicare Advantage plans are private plans that replace traditional Medicare. They are US-based and do not cover healthcare in Canada. If you have a Medicare Advantage plan, switching to traditional Medicare before your move and making decisions about Part B maintenance is typically the right sequence.

The Medicare Strategy for Americans Moving to Canada

- Keep Part A (no premium for most people, no reason to drop it)

- Evaluate Part B: if you plan to return to the US regularly or permanently, maintain it and factor the premium into your Canadian living costs. If you are certain you will not return, model the lifetime penalty cost versus premium savings before disenrolling

- Drop Part D once you have Canadian prescription coverage in place — but be aware of re-enrollment penalties if you return

- Consult a licensed Medicare specialist before making any changes to your Medicare enrollment status

Covering Your US Visits: The Layer Most Americans Miss

Provincial health plans provide almost no practical coverage outside Canada. OHIP, for example, provides a daily out-of-country benefit of approximately $400 CAD for emergency inpatient hospital care and $50 CAD for emergency outpatient care. In a US emergency room, $400 CAD does not cover a single hour of care.

If you maintain any connection to the United States — visiting family, using a winter property, travelling for any reason — you need a separate layer of coverage for US healthcare costs. Provincial coverage will not protect you.

Travel Health Insurance for US Visits

Short-term travel health insurance covering emergency medical care in the US is available through Canadian insurers, credit card travel benefits, and specialty travel insurers. Coverage typically includes emergency hospital care, physician visits, emergency evacuation, and prescription drugs in an emergency. Costs vary significantly based on age and trip length:

- Adult under 60: approximately $3 – $8 CAD per day for emergency medical coverage in the US

- Adult 60–70: approximately $8 – $20 CAD per day depending on health status

- Adult 70+: $20 – $50+ CAD per day — pre-existing condition clauses become more significant

Pre-existing condition exclusions are standard in travel health insurance. Most plans will not cover treatment related to conditions diagnosed before the policy start date. Some plans offer a stability clause — if your condition has been stable for a defined period (typically 90 to 180 days), it may be covered. Read the fine print carefully.

International Health Insurance — The Comprehensive Option

For Americans who split meaningful time between Canada and the United States — or who travel frequently — an international health insurance plan is often more efficient than managing separate provincial supplemental and travel insurance policies.

International plans provide comprehensive year-round coverage in all countries including both Canada and the United States. They cover the gap period before provincial health begins, ongoing non-insured services, and US healthcare costs in a single policy. Costs are higher than domestic supplemental insurance but replace multiple separate policies.

Plans commonly available to US nationals in Canada include GeoBlue Xplorer (designed specifically for Americans abroad, including full US coverage), Cigna Global, Aetna International, and Allianz Care. Annual premiums for a healthy adult in their 50s typically range from $4,000 to $8,000 USD depending on plan design and deductible.

INTERNATIONAL PLAN ADVANTAGE FOR CROSS-BORDER FAMILIES International health insurance plans can typically cover the entire family under a single policy regardless of where each family member is located. For cross-border families where one spouse may be in the US and one in Canada, or where children are attending US universities, this can be significantly more cost-effective than separate domestic plans in each country. Confirm that any plan you consider explicitly covers the United States — some international plans exclude the US or charge substantially higher premiums for US coverage. |

Long-Term Care: The Coverage Gap That Grows Over Time

Provincial health insurance does not cover long-term care in the traditional sense. Chronic, ongoing residential care — nursing home and assisted living — is not a fully insured service under provincial health plans. Residents of long-term care facilities in Canada pay a regulated daily co-payment that varies by province and income. In Ontario, for example, basic long-term care co-payments run approximately $62 to $110 CAD per day depending on room type — over $22,000 to $40,000 CAD annually.

For Americans who move to Canada in their 40s or 50s, long-term care planning is a decades-long horizon question. The options are:

- Canadian long-term care insurance — available from major Canadian insurers, best purchased before age 65 when premiums are still manageable and underwriting is more accessible. Coverage pays a daily benefit toward care facility costs.

- Hybrid life/LTC products — life insurance or annuity products with a long-term care rider, available in both the US and Canada. May be more efficient for those who want to preserve wealth if long-term care is never needed.

- Self-insurance through asset accumulation — for Americans who move to Canada with substantial assets, self-funding long-term care costs may be more practical than ongoing premiums. This requires explicit modelling of care cost projections.

US long-term care insurance policies generally do not pay benefits for care received in Canada. If you hold a US LTC policy, confirm with your insurer whether Canadian facilities qualify under your policy before assuming your existing coverage applies.

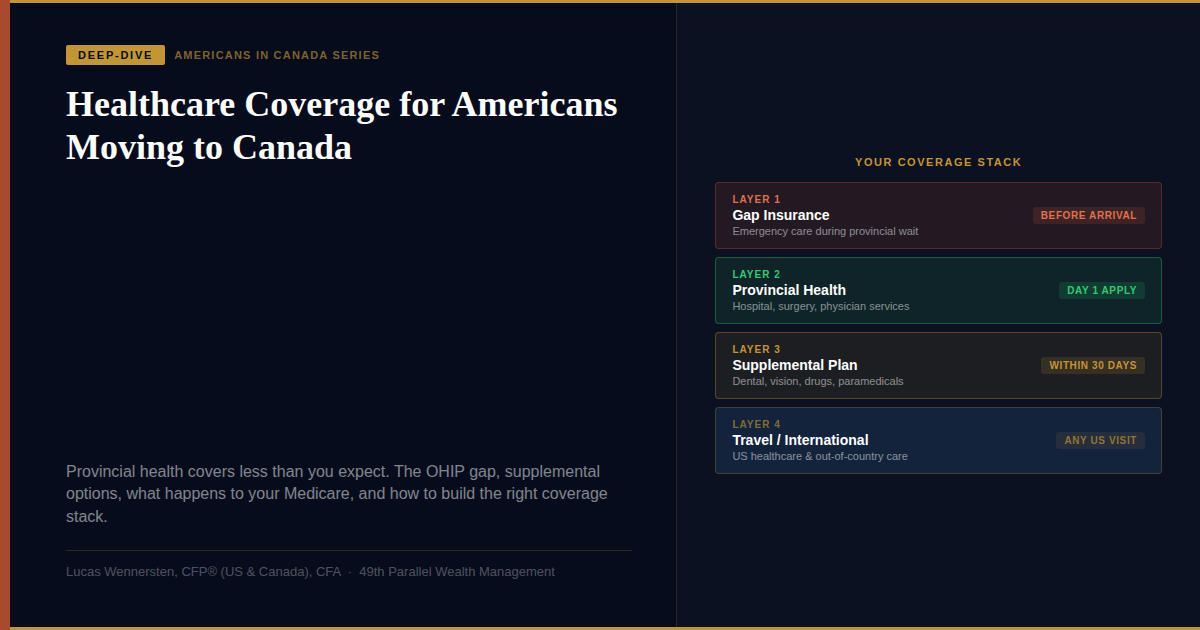

Building Your Coverage Stack: The Right Structure for Americans in Canada

Most Americans in Canada need a three-layer or four-layer coverage structure depending on their US connection. Here is the framework:

| Layer | What It Covers | When You Need It |

| Layer 1 Gap Insurance | Emergency hospital and physician care in Canada during the provincial wait period | Before arrival until provincial coverage begins — typically 3 months |

| Layer 2 Provincial Health | Medically necessary hospital, physician, surgery, diagnostic imaging | Permanent once established — apply immediately on arrival |

| Layer 3 Supplemental Plan | Dental, vision, prescription drugs, paramedical, private room | Enroll within 30 days of provincial coverage starting for best terms |

| Layer 4 Travel / International | US healthcare costs, out-of-country emergencies, full international coverage | Any time you spend in the US or travel outside Canada |

For Americans who do not travel to or spend time in the US, Layer 4 may not be necessary. For Americans who regularly return to the US — for family, for winter, for property, for any reason — Layer 4 is non-negotiable. US healthcare costs without coverage are severe enough to create genuine financial risk regardless of asset level.

The Bottom Line

Canada’s healthcare system is genuinely good at what it covers. The misunderstanding that Americans bring to the move is that it covers everything. It does not — and the gaps are significant enough that unplanned exposure to them can cost tens of thousands of dollars.

The good news is that the coverage structure is straightforward once you understand it. Arrange gap insurance before you arrive. Register for provincial coverage on day one. Enroll in a supplemental plan as soon as provincial coverage begins. Decide on your Part B Medicare strategy before you move, not after. And if you maintain any connection to the United States, make sure you have coverage for US healthcare costs that your provincial plan will not provide.

Healthcare planning is one of the areas where we see Americans make the most avoidable mistakes in their first year in Canada. If you would like to talk through your specific coverage situation as part of a broader cross-border financial plan, book a complimentary consultation with our team.

Frequently Asked Questions |

What does provincial health insurance cover in Canada?

Provincial health insurance covers medically necessary hospital and physician services: emergency care, surgery, hospital stays, diagnostic imaging, and specialist visits when referred by a family doctor. It does not cover prescription drugs, dental care, vision care, physiotherapy, chiropractic, paramedical services, or out-of-country care beyond a very limited daily benefit. Approximately 60 percent of Canadians carry private supplemental insurance to fill these gaps.

How do I cover the OHIP wait period when I move to Ontario?

Ontario requires a three-month wait before OHIP begins. Arrange private gap insurance — a newcomer health plan or extended travel health policy — before your arrival date. Do not arrive without coverage. Some insurers will not issue a newcomer plan to someone already in Canada without coverage.

What happens to my US Medicare if I move to Canada?

Medicare Part A and Part B do not cover healthcare received in Canada. Keep Part A (no premium for most). Evaluate Part B: if you may return to the US, maintain it and factor in the monthly premium. If you disenroll and re-enroll later, you face a permanent 10% premium penalty for each year without Part B. Get specialist Medicare advice before making any enrollment changes.

What supplemental health insurance do I need as an American in Canada?

Most Americans need three or four layers: gap insurance during the provincial wait, provincial health once established, a Canadian supplemental plan for dental/vision/drugs/paramedical, and travel or international health insurance for any time spent in the United States. Provincial health provides almost no practical US coverage.

Does provincial health insurance cover me when I visit the US?

Provincial plans provide a minimal daily out-of-country benefit — typically $50 to $400 CAD per day. This is wholly inadequate for US healthcare costs. Any time you spend in the United States, you need separate travel health or international health insurance that explicitly covers US healthcare.

Can I get employer group health benefits in Canada as an American?

Yes, if your Canadian employer offers group benefits. Enroll within 30 to 90 days of employment start — missing the window typically means waiting until open enrollment. You must be covered by your provincial health plan to enroll in most Canadian group benefit programs.

What is the difference between travel insurance and international health insurance?

Travel insurance covers short trips and emergency care only. International health insurance is an ongoing comprehensive plan covering you year-round in multiple countries including both Canada and the US. For Americans spending significant time in both countries, international health insurance is typically more appropriate than a series of short-term travel policies.

What does supplemental health insurance cost in Canada?

Individual supplemental plans covering dental, vision, prescription drugs, and paramedical cost approximately $80 to $150 CAD/month for a healthy adult under 40, $130 to $250 CAD/month for adults 40 to 60, and $200 to $350 CAD/month for adults over 60. International health plans covering both Canada and the US typically cost $4,000 to $8,000 USD annually for adults in their 50s.

How does healthcare coverage work if I split time between Canada and the US?

You need provincial health in Canada (maintaining required provincial presence days), supplemental coverage for non-insured Canadian services, and separate coverage for US healthcare costs. An international health insurance plan covering both countries is often the most efficient solution for those spending meaningful time in both.

Can I use my US long-term care insurance policy in Canada?

Most US long-term care insurance policies do not pay benefits for care received in Canadian facilities. Confirm with your insurer before assuming your US LTC policy covers Canadian care. If you are moving permanently, consider whether replacing a US LTC policy with a Canadian plan is appropriate given the different coverage geography.