Buying Property in Canada as an American: What the Guides Don’t Tell You

By Lucas Wennersten, CFP® (US & Canada), CFA Founder, 49th Parallel Wealth Management | Published: May 2026 Reading time: ~9 minutes · ~2,200 words |

The Foreign Buyers Ban doesn’t block most Americans with permanent residency. But land transfer taxes, Part XIII rental withholding, FIRPTA on your US home, and capital gains in two countries do. The complete cross-border real estate guide.

IMPORTANT NOTE This article provides general information about real estate ownership in Canada for Americans. Canadian real estate law, tax rules, and the Foreign Buyers Ban are subject to change. Tax rates and rules cited reflect the position as of May 2026. Always obtain independent legal and tax advice specific to your situation before purchasing property in Canada or selling US property after establishing Canadian residency. 49th Parallel Wealth Management is registered as an investment adviser in the United States and does not provide legal or real estate advice. |

FREE DOWNLOAD The American’s 2026 Canada Relocation Checklist Includes the real estate planning steps: Foreign Buyers Ban eligibility, Section 116 clearance certificate timing, FIRPTA planning for your US property, and pre-purchase tax coordination. Free download: 49thparallelwealthmanagement.com/american-canada-relocation-checklist |

AMERICANS IN CANADA — COMPANION SERIES Part 1: How Long Can an American Stay in Canada? Part 2: What Does Canada Actually Cost an American? Part 3: The Tax Reality No One Tells Americans Moving to Canada Part 4: What Nobody Tells Americans Before Their First Full Year in Canada Part 5: So You Want to Make It Official Deep-Dive: Healthcare Coverage for Americans Moving to Canada Deep-Dive: Buying Property in Canada as an American — this post |

When Americans considering a move to Canada search for real estate guidance, most of what they find is wrong for their situation. Articles written for domestic Canadian buyers cover mortgage qualification, bidding process, and closing costs — all useful, but none of it addresses the cross-border dimensions that make buying property in Canada as an American genuinely different.

The Foreign Buyers Ban — which most Americans assume blocks them entirely — does not apply to permanent residents. The land transfer taxes, which most articles mention briefly, are substantially higher for non-residents than the published provincial rates suggest. The rental income rules, the capital gains coordination between two countries, and the FIRPTA exposure on your US property once you establish Canadian residency: none of these appear in a standard Canadian real estate guide.

This post covers the cross-border real estate picture that those guides miss.

The Foreign Buyers Ban: What It Actually Blocks — and What It Doesn’t

The Prohibition on the Purchase of Residential Property by Non-Canadians Act has been in force since January 1, 2023, and has been extended until January 1, 2027. Most Americans assume it blocks them from buying in Canada. For many, it does not.

Who the Ban Applies To

The ban applies to foreign nationals who are not Canadian citizens or permanent residents, and to foreign corporations and entities controlled by foreign nationals. It covers residential properties with three or fewer dwelling units located within Census Metropolitan Areas and Census Agglomerations — broadly, urban areas with populations above 10,000.

Who Is Exempt — Including Most Americans Seriously Considering the Move

• Canadian permanent residents — fully exempt regardless of citizenship. An American who has obtained Canadian PR can buy without any restriction under the ban.

• Canadian citizens — exempt by definition.

• Work permit holders — can purchase residential property if their permit has at least 183 days remaining at the time of purchase and they are not already subject to the ban for other reasons.

• Spouses or common-law partners of Canadian citizens or permanent residents — exempt even if they themselves are foreign nationals.

• Refugee claimants and protected persons — exempt.

What the Ban Does Not Cover

• Recreational property and rural property outside Census Metropolitan Areas and Agglomerations — a cottage in cottage country or rural property is not subject to the ban regardless of buyer status.

• Buildings with four or more dwelling units — apartment buildings and larger multiplexes are excluded.

• Vacant land zoned for mixed-use or other purposes — certain vacant land purchases are permitted.

IF YOU ARE NOT YET A PERMANENT RESIDENT Americans who are in the process of applying for permanent residency but have not yet received it are subject to the ban if they wish to purchase in a covered urban area. Planning your real estate purchase timing around your expected PR grant date is important. Purchasing through a Canadian citizen or permanent resident spouse is an alternative path in some situations — but the ownership and financing structure carries its own legal and tax implications that require specialist advice. |

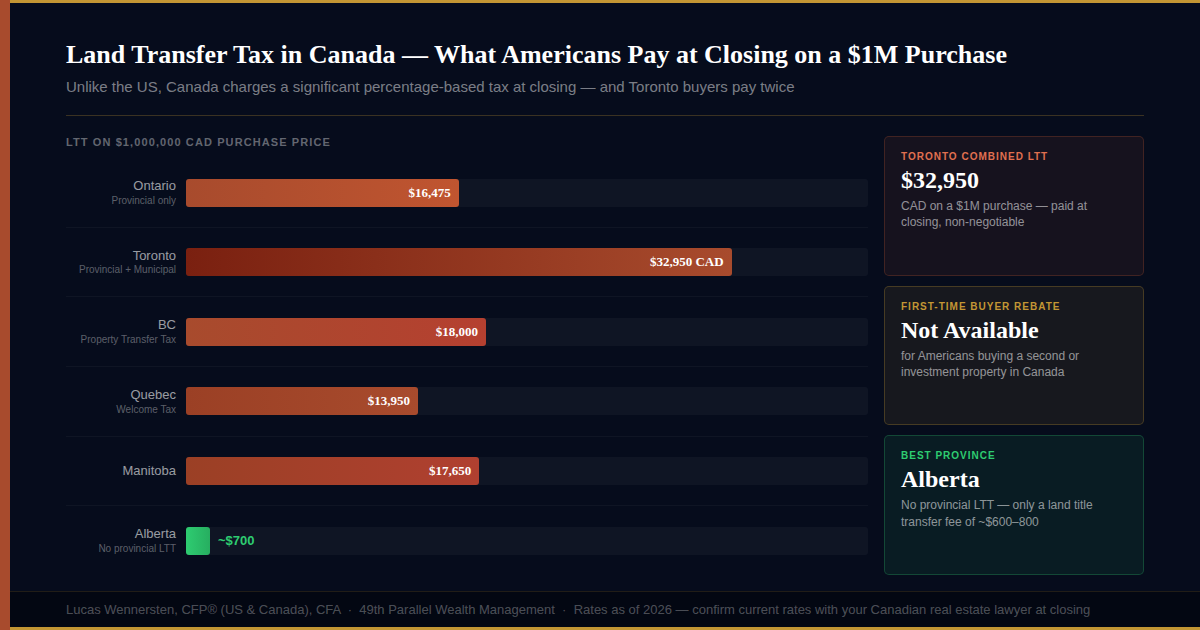

Land Transfer Tax: The Closing Cost Most Americans Underestimate

Unlike most US states which charge a modest recording fee at closing, Canadian provinces levy a Land Transfer Tax (LTT) calculated as a percentage of the purchase price. For permanent residents, this is the standard provincial rate. For non-residents, an additional Non-Resident Speculation Tax applies on top.

Provincial Land Transfer Tax — Standard Rates for Permanent Residents

Province | LTT Rate Structure | Tax on a $1M Purchase |

Ontario | 0.5% to $55K – 2% above $400K – 2.5% above $2M | ~$16,475 |

Toronto (additional) | Same bracket structure as Ontario — stacks on top | ~$16,475 additional = ~$32,950 combined |

British Columbia | 1% to $200K – 2% to $2M – 3% above $2M | ~$18,000 |

Quebec (Welcome Tax) | 0.5% to $53K – 1% to $267K – 1.5% above – higher brackets in Montreal | ~$13,500 outside Montreal |

Alberta | No provincial LTT — land title transfer fee only | ~$500 flat fee |

Nova Scotia | Deed Transfer Tax: 1.5% standard — non-NS residents: 10% (as of April 2025) | ~$15,000 resident / ~$100,000 non-resident |

NON-RESIDENT SPECULATION TAX — A CRITICAL ADDITIONAL COST FOR NON-PR BUYERS Americans who are not Canadian permanent residents face significant additional taxes on top of standard LTT: • Ontario NRST: 25% of the purchase price — province-wide. On a $1M property: $250,000 • Toronto municipal surcharge: additional 10% effective January 2025 — combined non-resident burden in Toronto: approximately 35% of purchase price • BC Additional Property Transfer Tax: 20% in Metro Vancouver and certain surrounding regional districts • Nova Scotia: 10% non-resident deed transfer tax applies to all non-Nova Scotia residents — not just foreign nationals Permanent residents are exempt from NRST in all provinces. This is one of the most significant financial advantages of establishing permanent residency before purchasing Canadian real estate. |

|

Rental Income from Canadian Property: Part XIII and Section 216

If you own Canadian property and rent it out while you are not a Canadian tax resident, Canadian tax law requires withholding on the gross rental payments. This is Part XIII of the Income Tax Act, and it catches many Americans by surprise.

How Part XIII Works

When you are a non-resident of Canada and rent out a Canadian property, your tenant — or the property manager acting on their behalf — is legally required to withhold 25% of each gross rental payment and remit it to the Canada Revenue Agency monthly. This is not optional. If the tenant fails to withhold and remit, they become personally liable for the amounts that should have been withheld.

On a property generating $3,000 CAD per month in rent, this means $750 CAD is withheld every month and remitted to the CRA — $9,000 annually — before you see a dollar of net income.

The Section 216 Election — Reducing the Withholding to Net Income

The withholding can be reduced from 25% of gross to 25% of net rental income (gross rent minus eligible expenses) by filing a Section 216 election with the CRA. This is an annual filing that calculates your actual rental income after mortgage interest, property taxes, insurance, maintenance, and property management fees.

In practice, for many rental properties with significant mortgage interest and expenses, the net income subject to withholding is substantially lower than gross rent. The Section 216 election is almost always worth filing — but it requires an annual Canadian tax return even if you are not a Canadian resident.

CANADIAN TAX RESIDENT VS NON-RESIDENT — THE RULE CHANGES If you are a Canadian tax resident — because you have moved to Canada and established sufficient residential ties — you are taxed on your worldwide income in Canada as an ordinary resident, not under Part XIII. Your Canadian rental income goes on your T1 return as regular income. The Part XIII regime applies only while you are a non-resident of Canada. The distinction between resident and non-resident rental tax treatment is one of the most significant planning considerations if you own Canadian rental property before establishing residency. |

Selling Canadian Property: Capital Gains in Both Countries

When an American in Canada eventually sells their Canadian property, both the CRA and the IRS may have a claim on the gain. How the two systems interact — and how to structure the coordination — is one of the most complex areas of cross-border real estate planning.

Canadian Capital Gains Tax

Canada taxes capital gains based on your Canadian cost base — the price you paid when you acquired the property, or the fair market value on the date you arrived in Canada if you owned it before establishing residency. The current capital gains inclusion rate for individuals is 1/2 on the first $250,000 of gains annually and 2/3 above that threshold. The included portion is taxed at your marginal income tax rate.

US Capital Gains Tax

The IRS taxes capital gains from the sale of Canadian real estate on your US return. The gain is calculated based on your US cost basis and is subject to US capital gains rates — typically 15% or 20% for long-term gains, plus 3.8% net investment income tax for higher earners. The foreign tax credit allows you to offset the US tax owing with Canadian capital gains tax paid on the same gain, generally preventing true double taxation.

Section 116 — The Non-Resident Withholding Requirement

When a non-resident of Canada sells Canadian real estate, the purchaser is required to withhold a portion of the proceeds — typically 25% of the gross purchase price for general real estate or 50% of the estimated gain — and remit it to the CRA. This withholding continues until the seller provides a clearance certificate from the CRA confirming the tax on the gain has been paid or secured.

For a $1M property sale, 25% withholding means $250,000 held by the purchaser until the clearance certificate is issued. The clearance certificate process can take several weeks to months. Non-residents selling Canadian real estate should apply for the clearance certificate well in advance of closing — ideally at least two months before the intended closing date.

CLEARANCE CERTIFICATE — APPLY BEFORE CLOSING Missing the Section 116 clearance certificate is one of the most common and costly mistakes in non-resident real estate transactions. Without it, the purchaser is legally required to hold back funds regardless of any agreement between buyer and seller. Many real estate lawyers and agents who primarily work with domestic transactions do not flag this issue proactively. If you are a non-resident of Canada selling Canadian property, confirm with your real estate lawyer that Section 116 planning is in place well before you list the property. |

FIRPTA: The Reverse Problem You May Not Know You Have

FIRPTA — the Foreign Investment in Real Property Tax Act — is the US-side equivalent of Canada’s non-resident withholding rules. It creates a significant compliance obligation for Americans who have established Canadian tax residency and still own US real estate.

What FIRPTA Requires

When a foreign person sells US real property, the purchaser is required to withhold 15% of the gross sales price at closing and remit it to the IRS. Once you establish Canadian tax residency, you become a foreign person for FIRPTA purposes under US tax law. This means if you later sell your US home, your vacation property, or any other US real estate, the purchaser must withhold 15% of the full purchase price — not the gain, the full price — at closing. The IRS FIRPTA withholding rules apply automatically when the seller is a foreign person.

On a $600,000 US home sale, 15% withholding means $90,000 held from your closing proceeds. The withholding is a prepayment of tax, not a tax itself — you file a US return for the year of the sale and the withholding is credited against your actual tax owing. But it means your closing net is $90,000 lower than expected unless you plan for it.

The Withholding Certificate — How to Reduce or Eliminate the Withholding

You can apply for a withholding certificate from the IRS to reduce the withholding to the amount of tax actually estimated to be owed. The application — IRS Form 8288-B — must be filed before or at the time of closing. If the certificate is issued before closing, the purchaser can reduce their withholding obligation. If the certificate is still pending at closing, the purchaser must still withhold the full 15% but can remit it to the IRS pending the certificate outcome.

PLAN FIRPTA BEFORE YOU LIST The FIRPTA certificate process typically takes 60 to 90 days from application to issuance. If you are an American who has established Canadian residency and plans to sell US real estate, engage a US tax advisor to begin the Form 8288-B process well before your listing date. Waiting until you have an accepted offer significantly limits your options and risks closing delays. |

|

The Principal Residence Designation Conflict

Both Canada and the United States offer capital gains relief on the sale of your principal residence — but the two exemptions cannot always be used simultaneously on different properties.

Canada’s Principal Residence Exemption (PRE) allows you to designate one property per family unit per calendar year as your principal residence, exempting gains from Canadian capital gains tax for those years. The US Section 121 exclusion allows a similar exemption (up to $250,000 single / $500,000 married) on gains from the sale of a US principal residence you have owned and lived in for at least two of the last five years.

The conflict arises when you own property in both countries simultaneously. In any given year, you can only designate one property as your Canadian principal residence. If you also wish to claim the US Section 121 exclusion on your US property, you need to ensure your actual occupancy pattern satisfies both countries’ requirements for the years in question.

Careful year-by-year documentation of which property was occupied as your principal residence, and a deliberate strategy for how many years each property is designated in Canada, can significantly reduce the combined tax on eventual sales of both properties. This planning works best when started before either property is sold — not after.

The Bottom Line

Buying property in Canada as an American is entirely doable — particularly once you have permanent residency. The Foreign Buyers Ban is narrower than most people assume, and permanent residents are fully exempt. The complexity lies not in the buying process itself but in the tax and legal structures that surround ownership: the land transfer taxes that stack up at closing, the Part XIII withholding on rental income, the Section 116 clearance certificate when you sell, and the FIRPTA exposure on your US property once you establish Canadian residency.

None of these are insurmountable — but all of them require planning before you act, not after the fact. The cross-border real estate decisions that create the most problems are the ones made without understanding both sides of the border simultaneously.

If you are considering purchasing Canadian real estate or planning to sell US property after establishing Canadian residency, book a complimentary consultation with our team. We work with Americans at every stage of the Canada real estate conversation — from early planning to coordinating the tax filings on both sides of the border at sale.

Frequently Asked Questions

Can Americans buy property in Canada?

It depends on immigration status. Canadian permanent residents and citizens can buy without restriction. Americans on a valid work permit with at least 183 days remaining can also buy. Americans visiting or without qualifying status are subject to the Foreign Buyers Ban, which prohibits purchase of residential property in Census Metropolitan Areas and Agglomerations until January 1, 2027.

Does the Foreign Buyers Ban apply to Americans with permanent residency?

No. Permanent residents of Canada are fully exempt from the Foreign Buyers Ban regardless of their citizenship. An American with Canadian PR can purchase any residential property without restriction under the ban.

What is land transfer tax in Canada and how much is it?

Land transfer tax is a provincial tax paid by the purchaser at closing. Ontario charges up to 2% on properties above $400,000. Toronto adds a second municipal land transfer tax for a combined rate up to approximately 4.5% on high-value properties in the city. BC charges 1% to $200,000, 2% to $2M, 3% above. Alberta has no provincial LTT. Quebec charges a Welcome Tax of up to 1.5% or more in Montreal. Nova Scotia charges non-Nova Scotia residents 10% as of April 2025.

What is the Non-Resident Speculation Tax?

The NRST is an additional tax on top of land transfer tax for non-permanent residents purchasing residential property. Ontario’s NRST is 25% of the purchase price province-wide. Toronto adds a further 10% municipal surcharge effective January 2025, bringing the combined non-resident rate in Toronto to approximately 35%. BC’s Additional Property Transfer Tax is 20% in Metro Vancouver. Permanent residents are fully exempt from NRST.

What is Part XIII tax and how does it affect Americans with Canadian rental property?

Part XIII requires withholding of 25% of gross rental income paid to non-residents of Canada. Your tenant or property manager must remit this to the CRA monthly. You can reduce this to 25% of net rental income by filing a Section 216 election with the CRA annually. If you are a Canadian tax resident, ordinary Canadian income tax rules apply instead.

What is FIRPTA and how does it affect Americans in Canada?

FIRPTA requires purchasers of US real estate from a foreign person to withhold 15% of the gross sales price at closing. Once you establish Canadian tax residency you become a foreign person for FIRPTA purposes. When you sell US real estate, 15% of the full purchase price must be withheld unless you have obtained an IRS withholding certificate in advance. The certificate application (Form 8288-B) should be started at least 60 to 90 days before your anticipated closing date.

How is capital gains tax handled when an American in Canada sells a Canadian property?

Both Canada and the US may have a claim. Canada taxes gains from your Canadian cost base. The US taxes gains on your US return. The foreign tax credit generally prevents double taxation, but coordination between the two systems requires planning. Non-resident Americans selling Canadian property also face the Section 116 holdback — the purchaser must hold funds until you obtain a CRA clearance certificate. Apply for the clearance certificate at least two months before your intended closing date.

What is the Canadian Principal Residence Exemption and can Americans claim it?

Yes — Americans who are Canadian tax residents can claim the PRE for years the Canadian property was designated as their principal residence. You can only designate one property per family unit per year in Canada. When you also own a US property that could qualify for the US Section 121 exclusion, careful year-by-year planning of designations across both countries can significantly reduce combined capital gains tax on the eventual sale of both properties.

What is a Section 116 clearance certificate and when do I need one?

Section 116 requires non-residents selling Canadian real estate to obtain a CRA clearance certificate, or the purchaser must hold back 25% of the gross purchase price or 50% of the estimated gain. Apply well in advance of closing — the process can take several weeks to months. This is one of the most commonly missed steps in non-resident real estate sales.

Should I buy property in Canada before or after establishing Canadian residency?

For most Americans, the Foreign Buyers Ban makes purchasing before PR status difficult in covered urban areas. Once you have PR, buying as a Canadian tax resident means your full purchase price is your Canadian cost base and Part XIII withholding rules do not apply to rental income. Working with a cross-border tax specialist before any purchase is essential regardless of timing.

49thparallelwealthmanagement.com | crossingthe49thparallel.com |