Cross-Border Charitable Giving: A Guide for Wealthy Canada-US Families

By Lucas Wennersten, CFP® (US & Canada), CFA · 8-minute read

Home › Blog › Cross-Border Charitable Giving

This article is general education, not personalized tax, legal, or financial advice. Cross-border charitable rules are intricate, fact-specific, and change over time. Before making a significant gift, speak with a cross-border advisor about your situation.

For families with serious wealth and ties on both sides of the 49th parallel, cross-border charitable giving is one of the few planning areas where doing it thoughtfully and doing it carelessly produce dramatically different outcomes — sometimes a six-figure difference on a single gift. The instinct is simple: support the causes you care about. The execution is anything but, because the United States and Canada each reward charity through their own rules, and a gift that is beautifully tax-efficient in one country can be worth nothing on the other side of the border. For wealthy households it sits at the intersection of cross-border estate planning and tax strategy, which is exactly why it rewards getting right.

This guide walks through how giving actually works across the border, the single biggest lever most donors miss, and the structures that make sense once your giving reaches the scale where it deserves its own plan.

Cross-Border Charitable Giving

The default rule: each country only rewards its own charities

Start with the trap, because almost everyone walks into it. Under the domestic rules of both countries, you generally get tax relief only when you give to a domestic charity — a registered Canadian charity on your Canadian return, or a US-qualified organization on your US return. Write a cheque to a beloved charity across the border and, by default, you may get no tax benefit at all.

For a household giving modest amounts, that is a footnote. For a family giving hundreds of thousands of dollars a year, it is the whole game.

The single biggest lever: give appreciated securities, not cash

Before the cross-border mechanics, understand the move that matters most — because it is the one that compounds at the wealth levels we are discussing. When you donate publicly traded securities in-kind — directly, rather than selling them and donating the cash — the tax treatment improves sharply in both countries.

In Canada, the accrued capital gain on listed securities gifted in-kind to a registered charity is taxed at a 0% inclusion rate. You eliminate the capital gains tax entirely and still receive a donation tax credit on the full fair market value — the mechanics are set out in CRA Pamphlet P113 – Gifts and Income Tax. It is widely regarded as one of the most powerful individual tax breaks in the Canadian system.

In the US, donating appreciated securities held longer than a year to a public charity lets you deduct the full fair market value while avoiding the capital gains tax you would owe on a sale, as described in IRS Publication 526. Non-cash gifts above the reporting threshold are documented on IRS Form 8283.

Here is what that looks like. An Ontario donor holds $100,000 of stock bought years ago for $60,000. Sell first and donate the cash, and roughly $10,700 of capital gains tax comes off the top before the gift. Donate the shares in-kind instead, and that $10,700 simply disappears, while the donation receipt is identical. Same gift to the charity; materially more kept. At $5M+ portfolios with large embedded gains, this is the difference that funds the next gift.

One caution on both sides: do not pre-arrange a sale that legally obligates the charity to liquidate the moment it receives the shares. In the US especially, a prearranged sale can unwind the benefit. Gift the securities; let the charity decide.

The cross-border giving workaround: Treaty Article XXI

Here is where the dual-resident reality kicks in. The Canada-United States Tax Convention, at Article XXI, creates a limited bridge over the domestic “own-country-only” rule — but it comes with a string attached that surprises people.

For a US person living in Canada: you can give to a Canadian registered charity and claim it on your US return — but generally only against your Canadian-source income, within the usual US percentage-of-income limits, with a five-year carryforward for the excess. For a Canadian resident giving to a US charity, the mirror applies: you can claim it on your Canadian return, but generally only against your US-source income.

The practical consequence: if a US citizen in Canada has little or no Canadian-source income, the treaty deduction for gifts to Canadian charities has little or nothing to apply against. The relief exists, but the income has to line up with it.

There is one notable carve-out worth knowing: gifts to a college or university that you or a family member attended can qualify against your US income generally, not just Canadian-source income. For cross-border families with alma maters on both sides, this is a genuinely useful exception that most donors never hear about.

US donors claiming a treaty-based position typically disclose it on IRS Form 8833. It is a formality, but skipping it is the kind of thing that turns a clean deduction into a messy one.

The 2025 wake-up call: charities are not conduits

A recent Federal Court of Appeal decision — Priority Foundation v. Minister of National Revenue (2025 FCA 180) — is worth flagging for any family that has wondered whether they can route money through a Canadian charity to fund an American one. The court’s answer was unambiguous: no. Article XXI provides relief to donors claiming a gift on their own return; it does not authorize a Canadian registered charity to pass funds through to US charities, and a charity that does so risks losing its registration.

The takeaway for wealthy donors: cross-border giving is structured at the donor level, gift by gift, not by building a private pipeline between charities. If your philanthropy spans both countries, that is a design question to get right up front.

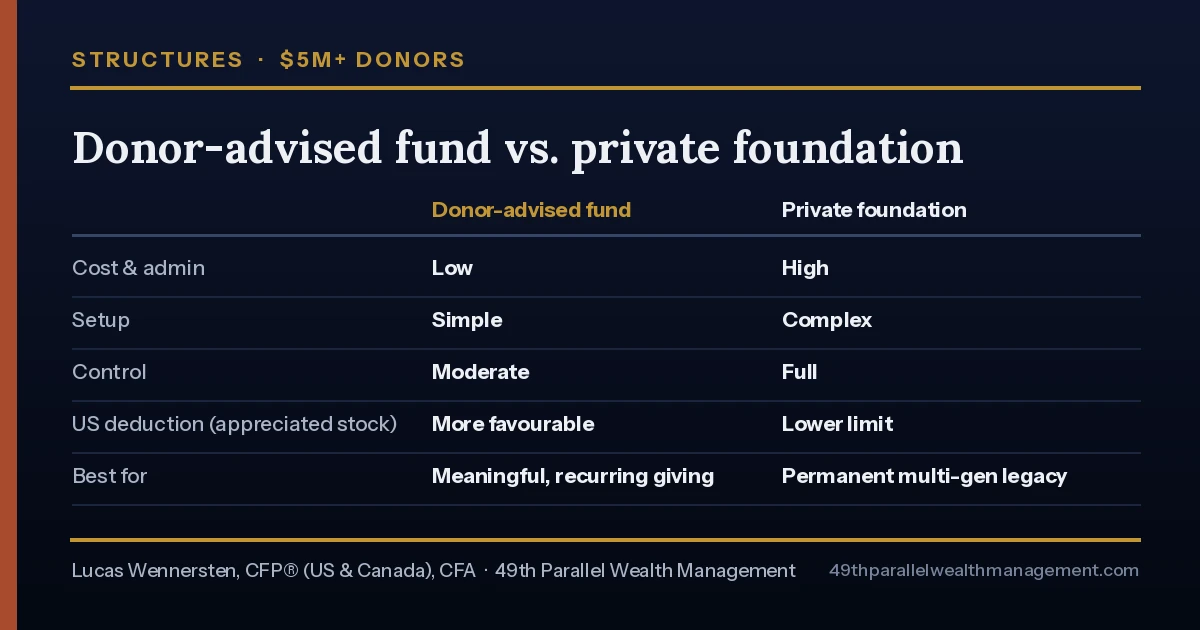

Structures for the $5M+ donor

Once your giving is substantial and recurring, individual gifts give way to structure. Three options dominate the conversation.

Donor-advised funds (DAFs). Available in both countries — through community foundations and the charitable arms of major financial institutions — a DAF lets you contribute appreciated securities now, take the deduction or credit now, and recommend grants to charities over time. It captures the appreciated-securities benefit, removes the assets from your taxable estate, and is far simpler and cheaper to run than a foundation. For most $5M+ families giving meaningfully but not running a philanthropic enterprise, the DAF is the workhorse.

Private foundations. More control, more legacy, more administration — and, on the US side, less favourable deduction limits than public charities and DAFs for gifts of appreciated stock. Foundations earn their keep for families who want a permanent, named institution and multi-generational involvement. This is also where it intersects with broader US estate tax exposure for Canadians, since a foundation can play a role in a larger estate plan.

Holding-company gifts (Canada). If your wealth sits in a Canadian holding company, donating appreciated securities in-kind from the corporation can deliver a deduction at the corporate level, eliminate the capital gain, and generate a capital dividend account credit that lets the company later pay a tax-free dividend to you. For incorporated owners and professionals managing wealth across the border, this is often the most efficient giving vehicle of all — and invisible to anyone planning at the personal level only.

Timing matters too. Percentage-of-income limits cap how much you can claim in a year (in Canada, generally up to 75% of net income; in the US, generally 60% for cash and 30% for appreciated securities to public charities, with five-year carryforwards). Large one-time liquidity events — a business sale, a big stock vest, the year you cross the border — are often the optimal moment to fund several years of giving at once, a move that fits naturally into a broader Canada-US tax strategy.

A cross-border giving checklist

Before you make a significant gift across the border, run through:

- Which return is this gift for? Decide up front whether you are claiming Canadian or US relief — it dictates which charity and which income the gift must align with.

- Cash or securities? If you hold appreciated public securities, default to giving them in-kind. The eliminated capital gain is usually the single largest benefit.

- Does the charity qualify on the relevant side? Canadian registered charity for Canadian relief; US-qualified organization for US relief; the treaty for the cross-border case.

- Is there source income to absorb it? For treaty gifts, confirm you have the Canadian-source (or US-source) income for the deduction to apply against.

- Should this be a DAF or foundation contribution instead of a direct gift? Especially in a high-income or liquidity-event year.

- Are you disclosing the treaty position? Form 8833 on the US side where applicable.

- Have you documented everything? Receipts, valuations, and CRA/IRS registration numbers all matter — cross-border gifts draw more scrutiny.

The bottom line

For wealthy cross-border families, philanthropy is one of the highest-leverage areas of the entire financial plan — but only when the gift, the country, the asset, and the structure are chosen together. Give cash to the wrong-country charity and you have donated generously and saved nothing. Give appreciated securities through the right vehicle, aligned to the right return, and the same generosity can cost you a fraction of the headline figure — leaving more for the causes you care about and your family both.

Frequently asked questions

Can I donate to a US charity and claim it on my Canadian tax return?

Generally only against your US-source income, under Article XXI of the Canada-US treaty. Without US-source income, the Canadian relief has little to apply against. The gift must also be to an organization that qualifies under Canadian standards.

Can I donate to a Canadian charity and claim it on my US tax return?

Yes, generally against your Canadian-source income under the treaty, within US percentage limits and with a five-year carryforward. There is an exception for gifts to a college or university you or a family member attended, which can apply against your US income more broadly.

What is Article XXI of the Canada-US tax treaty?

It is the provision that lets dual taxpayers claim cross-border charitable gifts that domestic rules would otherwise deny. It provides relief to the donor, tied to income sourced in the charity’s country, rather than treating a foreign charity as a domestic one for all purposes.

What is the most tax-efficient asset to donate?

For most wealthy donors, publicly traded securities with large accrued gains, given in-kind. Canada applies a 0% capital gains inclusion rate on such gifts; the US lets you deduct full fair market value while avoiding the gain. Cash is simpler but usually less efficient.

Can a Canadian charity send my donation to an American charity?

No. A 2025 Federal Court of Appeal decision confirmed Canadian registered charities cannot act as conduits to fund US charities. Cross-border giving is structured at the donor level, gift by gift, not through a charity-to-charity pipeline.

Is a donor-advised fund or a private foundation better for me?

Donor-advised funds are simpler, cheaper, and capture the same appreciated-securities benefit, which makes them the usual choice for $5M+ families giving meaningfully. Private foundations suit those who want a permanent, controlled, multi-generational institution and have the giving volume to justify the overhead.

Can I claim the same charitable gift in both countries?

Generally no. A single gift is claimed on one country’s return, with the treaty determining where cross-border relief is available. The system is designed to prevent a double benefit on the same donation.

Do I have to give by year-end to get the deduction?

For in-kind securities, the transfer must complete before year-end, and settlement takes processing time. Start well before December 31 rather than at the end of the month, or the gift may slip into the following tax year.

Does my Canadian holding company change the strategy?

Often, yes. In-kind securities gifts from a Canadian holding company can combine a corporate deduction, elimination of the capital gain, and a capital dividend account credit that supports a later tax-free dividend. For incorporated owners it is frequently the most efficient route.

More from Seven Figures, Two Countries

Concentrated Stock When You Move to Canada: The $5M Diversification Problem — The ITA 128.1 cost-base reset and the US-Canada basis mismatch.

The US Exit Tax When You Renounce: The Real Math at $5M+ — §877A mark-to-market, retirement, and the §2801 transfer tax that follows you forever.

T1135 Foreign Reporting: The Form That Can Cost More Than the Tax — The CRA’s foreign-property inventory that calculates no tax but punishes silence.

Planning a significant cross-border gift, or building philanthropy into a larger plan? Book a complimentary consultation with our team and we will map the most tax-efficient route for your situation.

This article is general education, not personalized tax, legal, or financial advice. Rules differ by province and state and change over time. Speak with a cross-border advisor before acting. — 49th Parallel Wealth Management.

From the Desert to the Tundra™

0 thoughts on “Cross-Border Charitable Giving: A Guide for Wealthy Canada-US Families”

Pingback: Concentrated Stock When You Move to Canada: The $5M Diversification Problem - Crossing the 49th Parallel

Pingback: Seven Figures, Two Countries: A Cross-Border Wealth Series for $5M+ Canada-US Families - Crossing the 49th Parallel